Below are prepared remarks delivered to the Senate Commerce Committee today on S-1877.

Thank you for the opportunity to testify on the need to preserve the individual health insurance market in New Jersey. While New Jersey has made major progress in reducing the uninsured, there are still about 700,000 New Jerseyans without coverage. Congress’ recent repeal of the shared responsibility penalty in the Affordable Care Act will undoubtedly cause that number to rise unless something is done.

This penalty provided an important incentive to ensure that younger, healthier people obtain insurance and spread the risk in the health insurance pool. Without robust participation of these individuals in our health insurance marketplace, premiums will climb and the market will become destabilized.

NJPP supports restoration of this requirement at the state level in New Jersey if steps are taken to also ensure that insurance is affordable. To achieve that goal we urge that S-1877 be amended to require that all revenues generated by the penalty be used only in ways that will make insurance more affordable, such as for state premium subsidies or to help fund reinsurance.

We also recommend that S-1878, which would establish a reinsurance plan and is also being considered by the committee today, be passed at the same time. We believe that the combination of these bills would create a synergy that would substantially reduce premiums for New Jerseyans. It would also be smart to allocate at least $2 million for outreach to make insurance more accessible, attract healthier people, and maximize federal funds.[1]

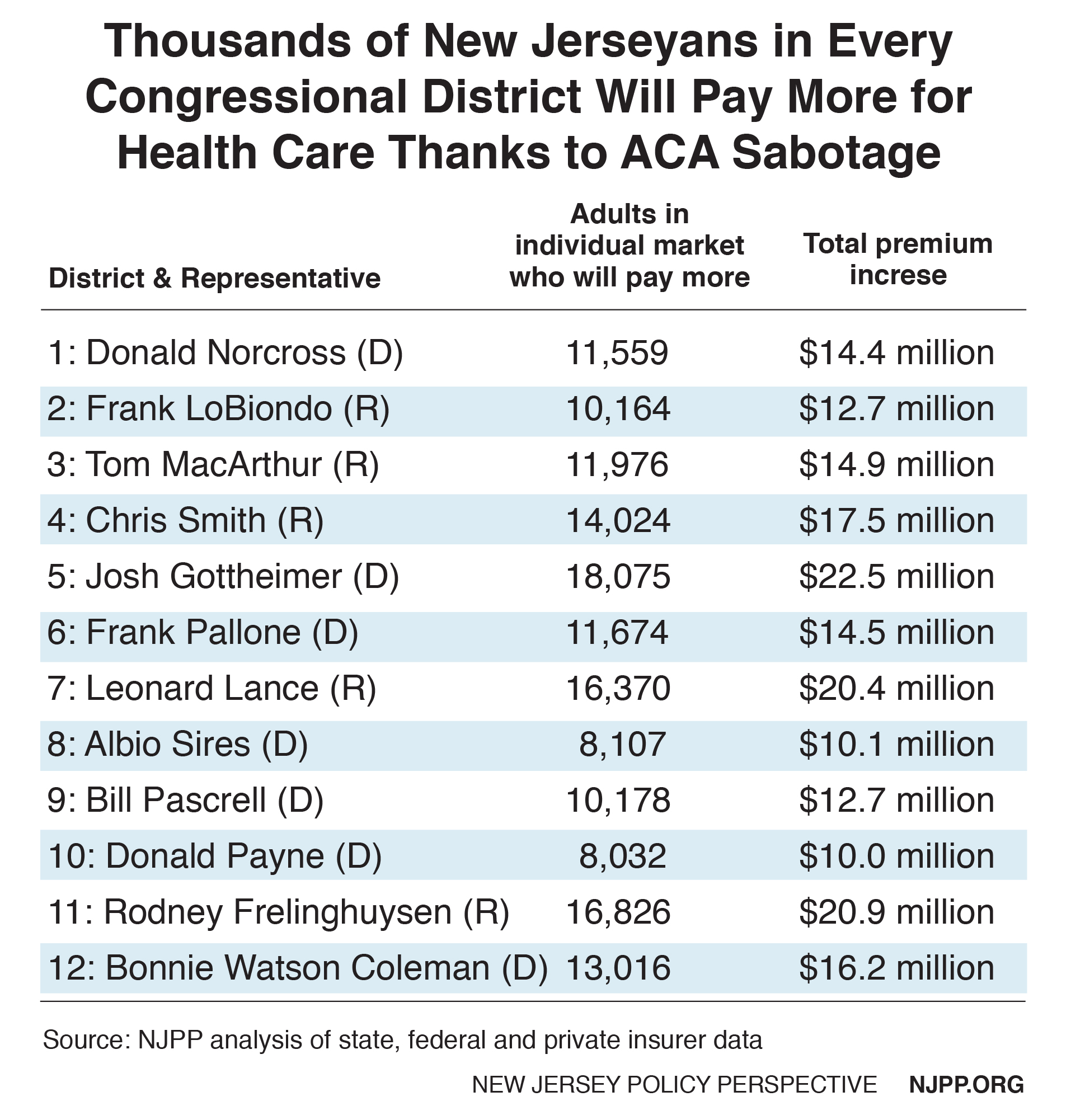

Because insurers need time to adjust their rates for next year, this has become an urgent matter. Unless legislation is enacted within the next four months to address this problem, next year about 150,000 middle class New Jerseyans will have to spend much more in premiums, thousands more will become uninsured, state charity care payments will increase and New Jersey will lose federal Medicaid funds.

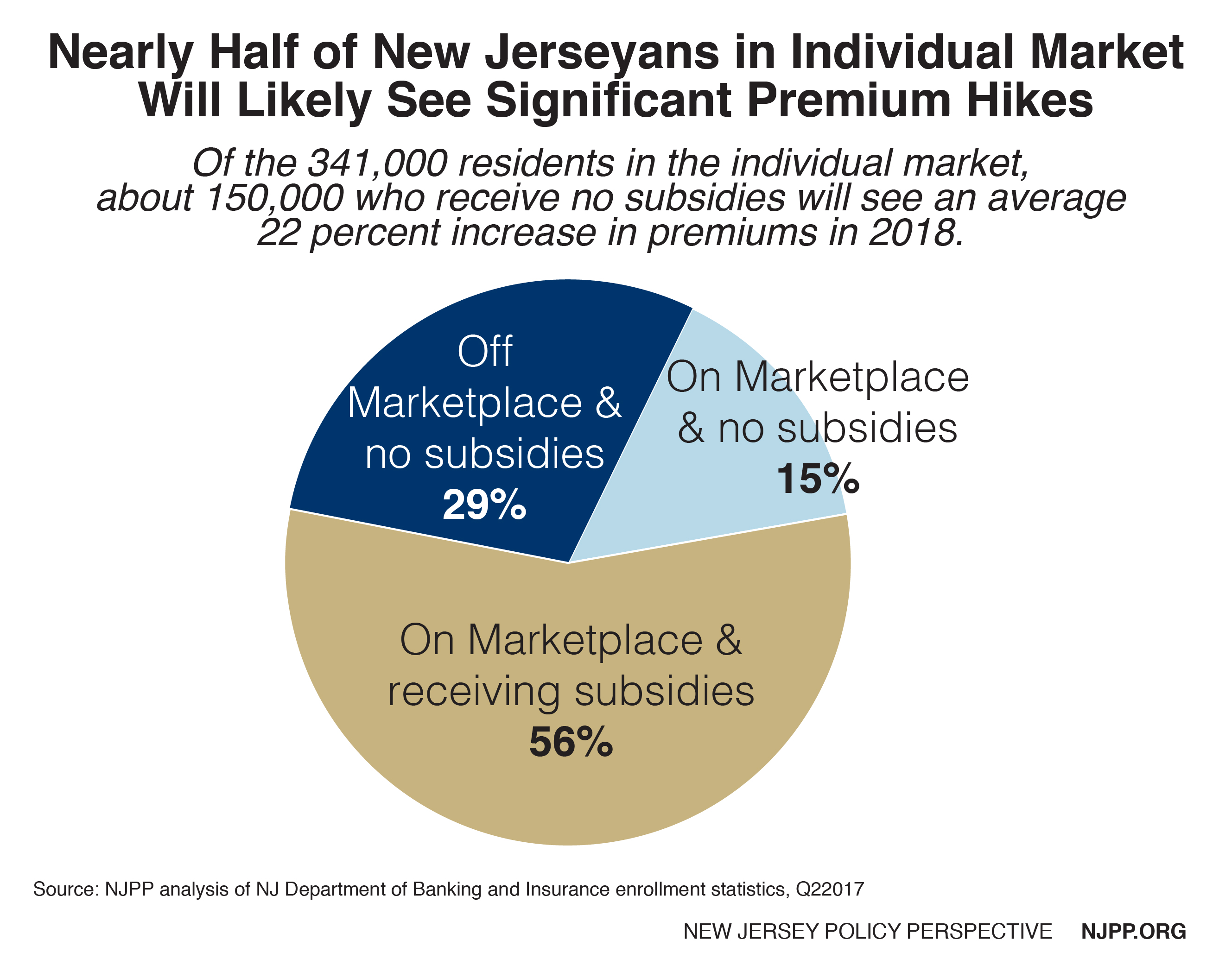

Unfortunately, some of this is already happening. Even before the federal penalty was repealed, premiums for most plans this year in New Jersey went up by 8.5 percent[2] (as part of an overall increase of 22 percent[3]) because the Trump administration threatened to weaken the enforcement of this requirement. This affected nearly half of everyone in the individual market because these consumers exceeded the income guidelines for subsidies.[4] We estimate they will pay up to a stunning $65 million more in premiums this year.

That means the average person in the marketplace paid $400 and a four-person family paid $1600 more this year just due to the weakening of the federal provision. Those costs could double next year without a shared responsibility penalty.

The long-range implications of not replacing this provision are staggering. Based on our analysis of national data from the Congressional Budget Office,[5] premiums in New Jersey will increase 10 percent a year in most of the next 10 years, and about 340,000[6] residents will become uninsured. Because the largest decrease in coverage would be in Medicaid, the state would also lose billions in federal matching funds. At the same time, we can expect a major increase in state charity care payments, which have been reduced by more than half due to the ACA.

Restoring this penalty is one of the most cost-effective ways that the state can reduce premiums since it costs the state nothing other than administrative costs and avoids a major loss in federal funds.[7] Another advantage is that very few New Jerseyans would be affected by the penalty. About 189,000 New Jerseyans paid the penalty in 2015 which meant that about three-fourth of all the uninsured were exempt from the federal penalty. These households represent only about five percent of all tax filers.

Under a state penalty even fewer people might be affected, depending on the state policies that are established. For example, the bill understandably exempts individuals who earn less than the income threshold income for state taxes ($10,000), which is twice as low as the federal threshold ($20,000). That exemption alone could reduce the number of persons who would have to pay the penalty by over 40,000.

The mandate also would encourage many of the uninsured to seek insurance that is affordable which they may not know about. National research shows that about half (54 percent) of everyone uninsured and eligible for a plan in the marketplace would be better off financially if they bought a bronze plan rather than paid the penalty.[8]

Endnotes

[1] State Medicaid outreach funds would receive a federal match of 50 percent.

[2] New Jersey Business, Majority of Horizon Individual Premium Increases Due To Federal Changes, October 17, 2017, based on Horizon charges, https://njbmagazine.com/njb-news-now/majority-horizon-individual-premium-increases-due-federal-changes/

[3] Raymond Castro, Sabotage of the Affordable Care Act Puts Middle-Class New Jerseyans in the Crosshairs, November 21, 2017, https://www.njpp.org/healthcare/sabotage-of-the-affordable-care-act-puts-middle-class-new-jerseyans-in-the-crosshairs

[4] 400 percent of the federal poverty level which is $82,000 for a family of three, well below the state’s median family income of $95,000 in 2016.

[5] CBO, Repealing the Individual Health Insurance Mandate: An Updated Estimate, November 8, 2017, https://www.cbo.gov/publication/53300

[6] Raymond Castro, Ibid.

[7] The current payments are $695 per adult and $347 per child or 2.5 percent of family income, whichever is greater.

[8] Matthew Rae, et al, How Many of the Uninsured Can Purchase a Marketplace Plan for Less Than Their Shared Responsibility Penalty? November 2017.