One of the most basic steps to protect public health during a pandemic is for people who are sick, or who have been exposed to the virus, to quarantine themselves, and the CDC recommends staying home for 14 days after possible exposure.[1] But that’s not always possible for essential workers unless they have access to enough paid sick days. New Jersey’s current earned sick day law provides only five days a year and employers can require that workers wait 120 days after the first day of work, and that they earn their time before they can use it. Employers can also ask for a doctor’s note for three or more consecutive days of absence. These burdensome measures make it harder for workers to access their paid sick days so that they can take care of their own health, stay home and protect others from exposure. We need to do more to protect essential and frontline workers and stop the spread of contagion, now or in the future, by strengthening and expanding our earned sick day law.

The need for paid sick days, especially during a pandemic, was so evident that the U.S. Congress took action for the first time ever, passing the Families First Coronavirus Response Act (FFCRA) which provides workers with 10 paid sick days for reasons related to COVID-19.[2] However, the new federal law exempted employers with over 500 employees and virtually all health care workers. And while health care workers are included in the NJ Earned Sick Leave law, per diem health care employees are not. That means an estimated 58 percent of New Jersey workers do not have access to any of the federal protections including emergency paid sick days.[3] Many of these workers are low paid, working at grocery store chains, big box stores and warehouses, and some have reported working in unsafe conditions, potentially exposed to sick coworkers and members of the public. By making changes to improve the state Earned Sick Leave law, we can ensure all essential and frontline workers have access to both basic and emergency paid sick days.

What does bill S2453 do?

Senate Majority Leader, Loretta Weinberg, the champion of the original Earned Sick Leave bill, has sponsored bill S2453 which improves the New Jersey Earned Sick Leave law by:

Providing essential workers with 15 emergency paid sick days available immediately during a declared state of emergency. This would be for future possible pandemics or other emergencies and for the current COVID-19 emergency it is retroactive to March 1, 2020.

Increasing the number of base earned paid sick days from 5 to 7 days.

Removing the burdensome 120 waiting period from a worker’s first day and when the employer must allow them to use the paid sick time that they have earned. As workers accrue their leave they should be able to take it.

Including per diem health care employees (removes their previous carve-out from coverage).

Changing employers’ ability to require a doctor’s note on the third consecutive day of absence to the fifth consecutive day and allows for telehealth documentation.

Adding 2 days bereavement time as an allowable use under the law.

New Jersey is home to the nation’s third largest share of immigrants, both documented and undocumented, who contribute greatly to the social and economic fabric of the state. Under the Trump administration, New Jersey’s immigrant residents face greater threats that put their health, safety, and future prosperity at risk. One such threat is the federal administration’s attempt to change the “public charge” policy, an inadmissibility test designed to identify people who may need public benefits in the future.[1] If the test determines that someone is likely to become a public charge, they would be denied admission to the United States or not be allowed to adjust their immigration status to lawful permanent residence (i.e. obtain a green card).[2] This brief answers frequently asked questions about the proposed public charge rule change.

It is

important to note that immigrant families should not be fearful but educated on

the issue of public charge so that they can make the best decision for

themselves and their families.

What is the current

public charge policy?

The public charge policy is a test that determines whether

an immigrant is likely to use public cash assistance or institutional long-term

care. The test applies to those who are applying for entry to the U.S., or for those seeking lawful permanent residence.

Additionally, immigrants with green cards who are outside of the United States

for more than six months could be subject to the public charge rule when they

return.

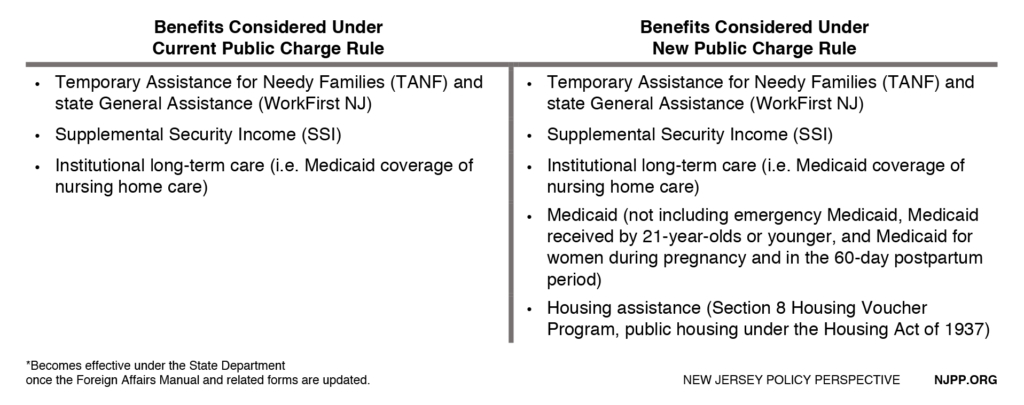

The programs considered in the test are federal and state public cash assistance programs including Temporary Assistance for Needy Families (TANF), Supplemental Security Income (SSI), General Assistance, and institutional long-term .[3]If deemed a public charge, a person can be barred from entering into the U.S. or from obtaining lawful permanent residence status (LPR). (For more on which specific state programs are considered under the rule, see section, “Would the public charge rule change immigrants’ access to New Jersey programs”).

Who is subject to public

charge?

The public charge rule primarily applies to people seeking to immigrate to the U.S. or adjust their immigration status to Legal Permanent Residents (LPRs) or green card holders through family-based petitions. It also will affect certain people seeking to extend or adjust their non-immigrant status (i.e. tourists) while in the U.S. [4]

Who is not subject to

public charge?

Naturalized U.S. citizens are not subject to a

public charge inadmissibility determination, nor are immigrants with lawful

permanent residence status (LPR). Additionally, humanitarian immigrants, such

as survivors of trafficking, domestic violence or other serious crimes, special

immigrant juveniles, and certain other immigrants are not subject to a public

charge test.

Other immigrants who are not subject to a public

charge test include those who apply for:

Deferred Action for

Childhood Arrivals (DACA) renewals

Refugee status

Asylum status

Temporary Protected

Status (TPS)

T and U visas (for

victims of human trafficking and serious crimes or witnesses of certain crimes)

Which agencies enforce

public charge?

The

public charge policy is enforced by both the Department of Homeland Security

(DHS) and the State Department. DHS is responsible for administering requests for adjustment of status and visas inside the United States

and the State Department is responsible for handling similar requests made

outside the U.S.

What would change under the new public

charge rule?

In August 2019, the Trump administration proposed a radical change in the public charge policy that would expand the scope of public benefit programs considered in a public charge determination. The proposed rule change, which was scheduled to take effect on October 15 2019, includes public benefits programs such as the Supplemental Nutrition Assistance Program (SNAP), Medicaid, and certain subsidized housing programs.[5] The rule would apply a similar test to people seeking to extend or change their temporary visas, such as students or temporary workers.

Federal courts have temporarily blocked implementation of the rule for immigrants within the U.S., which is administered by the Department of Homeland Security. One court found that the rule raised serious questions about whether it violates the Equal Protection clause as well as the Rehabilitation Act, which prohibits discrimination against individuals with disabilities. The courts also found that the rule would cause immediate irreparable harm to states, counties, and organizations serving immigrants and their families.[6] In response, the Trump administration appealed these decisions.

However, the court’s actions do not apply to

public charge determinations made outside of the U.S. by the State Department. The new public charge rule will

be enforced by the State Department once new forms

are finalized.

What is the public charge policy for immigrants who have applications processed outside the United States?

Outside the U.S., immigration officials within the State Department oversee visa applications and adjustment of status applications. In January 2018, the department revised its Foreign Affairs Manual (FAM) to change how immigration officials should weigh the affidavit of support that many U.S. sponsors must provide to demonstrate that an applicant will not become a public charge. In the past, an affidavit of support was generally considered enough to outweigh any public charge barrier.[7]

The FAM instructions also introduced other factors and thresholds that can be considered in a public charge test, such as new income thresholds, age, health, and health insurance considerations. Although it did not change the public charge definition, it allows officers to consider the use of any benefits by the applicant, family members or sponsors, thereby giving State Department officials more discretion to decide who is denied or approved.[8]

In fiscal year 2019, the State Department denied 5,343 immigrant visa applications for Mexican nationals based on their likelihood of becoming a public charge. This is a substantial increase from just seven denials under the last full year of the Obama administration.[9]

What other factors are used to determine public charge outside the United States?

The

public charge test is based on a “totality of circumstances” assessment. This

includes the applicant’s age, health, family status, income and resources,

education and skills, and the validity of an affidavit of support. Positive factors can be weighed

against negative factors, and no one factor will determine the outcome.

The following characteristics are considered under the

Foreign Affairs Manual (FAM):

Income, specifically whether the applicant earns less than 125 percent of the federal poverty level

Age, specifically whether the applicant is 18 or younger or 62 and older

Health, including complications that could interfere with the ability to work or care for oneself, increase future medical expenses, or require institutionalization

Education, specifically whether the applicant has less than a high school degree

Family size

Prior history of using public benefits

Would the public charge rule change immigrants’ access to New Jersey programs?

Immigrants,

regardless of status, who participate in state-funded programs — with the

exception of WorkFirst NJ, which includes TANF and General Assistance — would not have their benefits considered under the public charge rule because

the programs are state funded.

In New Jersey, immigrants who are undocumented and meet

certain criteria are eligible for the following programs: in-state tuition,

state financial aid, and NJ FamilyCare. These

benefits would not be considered in the DHS or

State Department public charge test.

Additionally,

if New Jersey joins other states in expanding access for undocumented

immigrants to obtain state health care, driver’s licenses, or other state-funded

programs, these benefits would not be counted under the public charge rule.

How would the public charge rule change harm immigrant families?

The public charge rule is purposely complicated to instill fear in immigrant families, even if the new rule does not apply to them. As a result, many immigrants and their U.S. citizen family members have unenrolled or foregone public services that they are entitled to.[10] This is also known as the “chilling effect” of the public charge rule change. In New Jersey, it is estimated that 690,000 people — including 250,000 children — may be harmed by the chilling effect. This represents 34.5 percent of the state’s immigration population.[11]

To

reduce the negative impact that the chilling effect has on immigrant families

and their U.S. citizen family members, it is important for community

organizations and state agencies to conduct outreach,

clarifying what the public charge rule is and what it means.

Would the public charge rule change harm New Jersey’s economy?

The new public charge rule, by harming immigrants and their families, also damages the broader state economy. As fewer immigrants sign up for health and nutrition programs, New Jersey can expect to lose $367 million in federal benefits.[14] The loss of these benefits could, in turn, harm local communities. Businesses such as grocery stores and supermarkets will likely lose income due to a decrease in SNAP enrollment.[15] Similarly, hospitals and health care providers will likely lose revenue with reduced enrollment in Medicaid and the Children’s Health Insurance Program (CHIP).

Overall, if the public charge rule change takes effect, New Jersey’s GDP is estimated to decline by as much as $709 million, with a related loss of 4,826 jobs and $38 million in lost state tax revenue, according to an analysis by the Fiscal Policy Institute.[16]

Acknowledgements

NJPP would like to thank Tanya Broder from the National Immigration Law Center (NILC) for reviewing this FAQ.

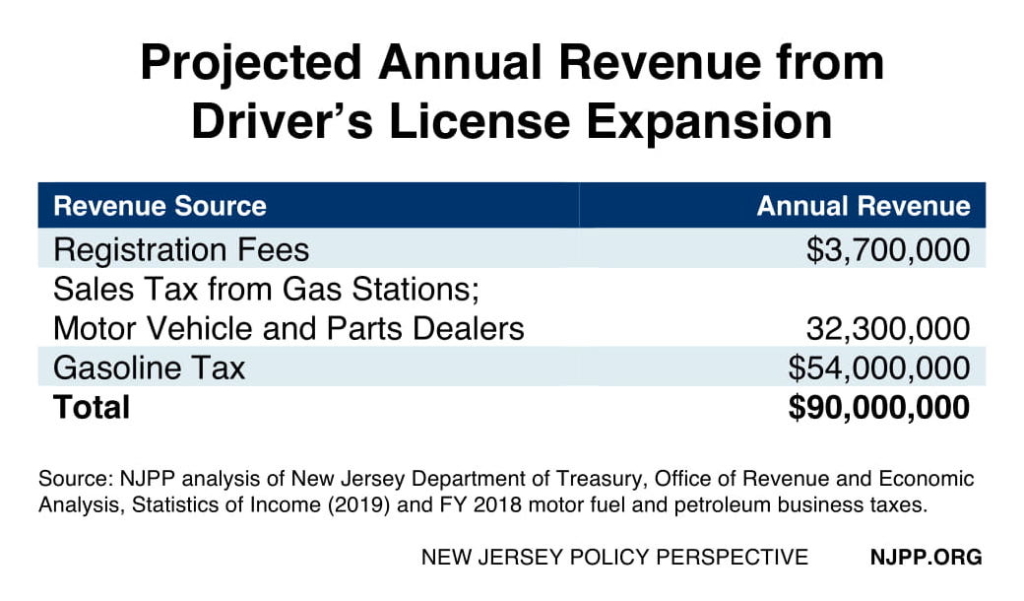

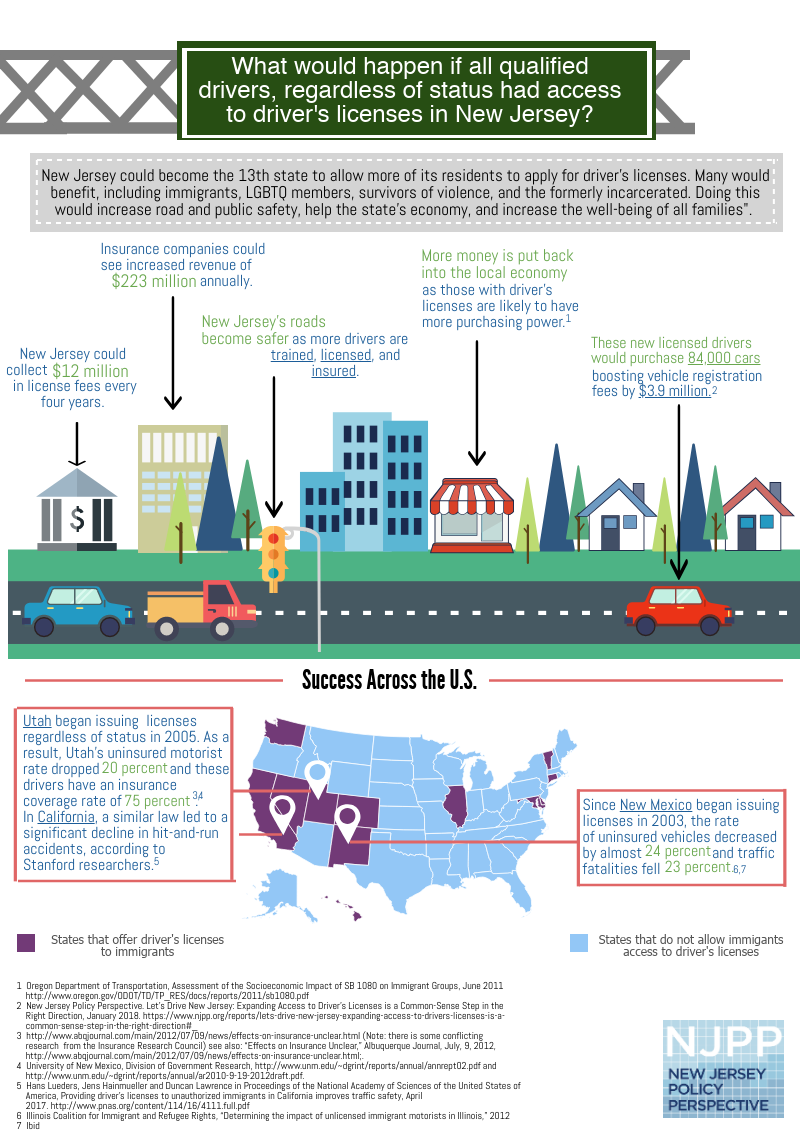

Expanding access to driver’s licenses to all New Jersey residents, regardless of immigration status, would make the state’s roads safer and its economy stronger. The proposal would also pay for itself by bringing in tens of millions of dollars in recurring revenue for the state’s general fund, according to an NJPP analysis of new data from the New Jersey Office of Revenue and Economic Analysis. This is a win-win for drivers, working families, and the state’s finances.

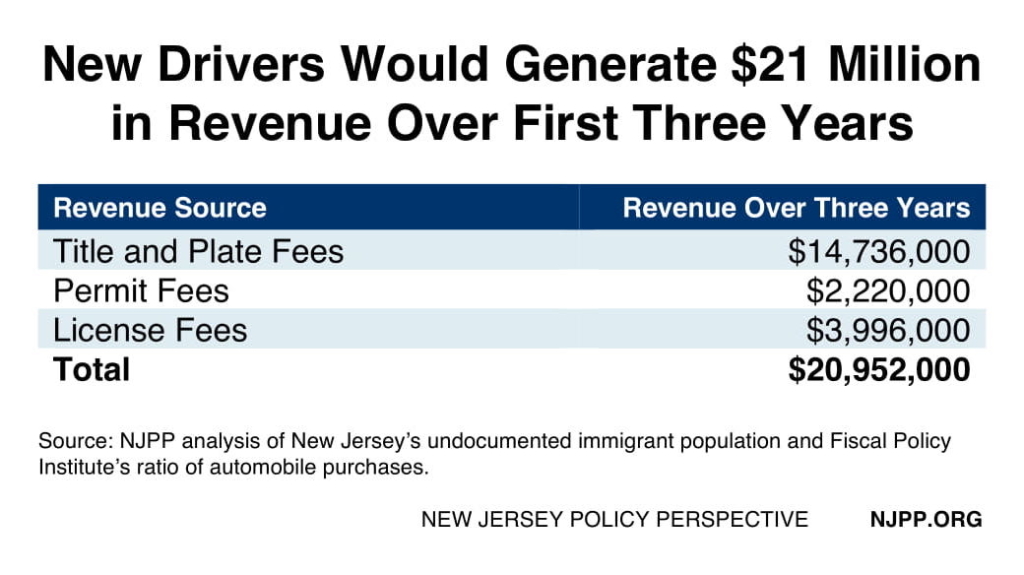

Over the first three years of implementation, driver’s license expansion is projected to generate $21 million in revenue from permit, title, and driver’s license fees. Once fully implemented, new drivers will generate $90 million annually from registration fees, the gas tax, and the sales tax on purchases made at gas stations and motor vehicle and auto parts retailers.[1]

New Jersey is one of the most diverse states in the nation and is home to approximately 484,000 undocumented residents, representing 5.4 percent of the state’s total population. Of the nearly half million undocumented residents, 91.5 percent are of driving age (16 and older). Based on the experiences of the twelve states that have already expanded access to driver’s licenses, NJPP estimates that 222,000 residents would obtain a drivers license during the first three years of implementation. This equates to a 3.5 percent increase in the total number of people in New Jersey with a driver’s license.[2]These new drivers would pay a collective $6 million in permit and license fees over the first three years of implementation.

These drivers are also estimated to purchase 80,000 cars over the same three year period, representing a three percent increase in the number of vehicles registered.[3] Title and plate fees associated with these new vehicles will generate almost $15 million in revenue.

According to NJPP’s analysis of new data from the New Jersey Treasury Department’s Office of Revenue and Economic Analysis, driver’s license expansion would also generate the state tens of millions of dollars in recurring revenue as new drivers register their vehicles and purchase gasoline as well as auto parts and associated retail goods at gas stations and auto part dealers. Using the Treasury’s data on sales taxes collected from gasoline stations and auto parts stores, combined with revenue figures from the petroleum gross receipts and motor fuels tax, NJPP projects that driver’s license expansion would generate $90 million annually in sales and gas tax revenue. Revenue from the gas tax would go directly to the Transportation Trust Fund, which currently collects 41.5 cents per gallon of gas sold. This will make the state’s gas tax collections less volatile and could lower the odds of a future gas tax increase.

In addition to making New Jersey’s roads safer and its economy stronger, expanding access to driver’s licenses would more than pay for itself, generating $90 million in tax revenue every year.

Methodology

Number of Undocumented Immigrants of Driving Age and the Number Who would obtain a driver’s license during the first three years of implementation

There are three estimates used to quantify the number of undocumented immigrants: 452,000 (Center for Migration Studies), 475,000 (Pew Hispanic Center), and 526,000 (Migration Policy Institute). The average of the three estimates is 484,000. There are two estimates for the percent of New Jersey’s undocumented immigrants who are 16 years or older: 90 percent (Center for Migration Studies) and 93 percent (Migration Policy Institute). NJPP took the average of the two numbers (91.5) and multiplied that by average number of undocumented immigrants to get the estimated number of undocumented residents who are of driving age: 444,000. We assume that New Jersey would have a high-end participation rate after three years, similar to Illinois’ rate of 47 percent. We project New Jersey’s rate will be slightly higher at 50 percent given driving is necessary to getting around the state’s sprawling suburbs. The Fiscal Policy Institute (FPI) similarly uses this take up rate in their projections for New York. Thus, we multiply the number of undocumented residents of driving age by the take up rate of 50 percent to project that approximately 222,000 undocumented immigrants who would obtain a driver’s license during the first three years of implementation.

Number of new cars on the road

To analyze new cars on the road after driver’s license expansion, NJPP projects similar automobile purchases and new licenses as FPI projected for New York. Multiplying FPI’s take-up ratio by the number of New Jersey residents that would get a driver’s license during the first three years of implementation projects 80,000 new cars. Note that new cars means new car purchases, not brand new automobiles. For more information, see: Expanding Access to Driver’s Licenses: Getting a License Without Regard to Immigration Status and Expanding Access to Driver’s Licenses: How Many Additional Cars Might Be Purchased? (http://fiscalpolicy.org/wp-content/uploads/2017/01/FPI-Additional-cars-report-2017.pdf)

Numbers for Annual Revenue

The annual revenue includes: registration fees, gas station and auto part sales tax revenue, and gas tax revenue. The projected 80,000 new cars after three years represents a 2.86 percent increase in registered cars in New Jersey. We multiplied the 2.86 percent increase to the latest figures on gas station and auto part retailer sales tax revenue and to annual gasoline purchases subject to the state gas tax (including petroleum gross receipts and motor fuels).

Revenue from the first three years of implementation

Regardless of a person’s age, first time drivers must pay a $10 dollar permit fee. NJPP multiplied this fee by 222,000, the number of estimated new drivers during the first three years of implementation. We also include revenue associated with title and license plates fees. We multiplied the one time fee of $46.50 times the number of estimated new cars, 80,000. Finally, we multiplied the number of people who would get a driver’s license during the first three years of implementation, 222,000 by $18 the price of a basic driver’s license according to Assembly bill A4743.

End Notes

[1] Does not include the revenue from sales tax of new car purchased.

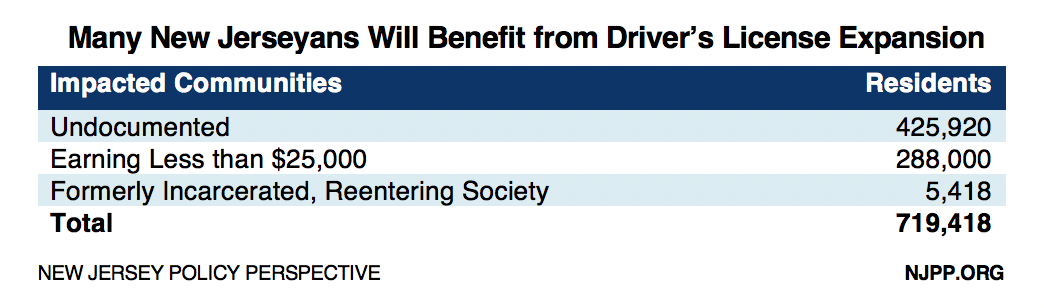

As New Jersey welcomes 2019 with the passage of a $15 minimum wage and paid family leave expansion, it’s time to shift focus to another policy issue that’s critical to the economic security of working families: making New Jersey the 13th state in the nation to allow all its residents to apply for driver’s licenses, regardless of their immigration status. There is a proposal in the Legislature — A4743 — that would lower the barriers to getting a driver’s license, impacting 719,000 New Jersey residents and benefitting not only undocumented immigrants, but those who earn less than $25,000 a year as well as those reentering society from the criminal justice system. This policy will increase public safety, empower workers and families in every corner of the state, boost the state’s economy, and contribute over $9 million in revenue to the state in the form of registration and licensing fees.

In New Jersey, having a car is essential to fully participating in the economy. No matter where you live in the Garden State — with very few exceptions — driving is necessary to get to work, pick kids up from school and take them to the doctor, shop for groceries and complete all the other errands that fill up the day. The ability to drive legally and safely is central to a vibrant New Jersey economy where everyone can work, get around and provide for themselves and their families.

Based on the experiences of other states that have implemented driver’s license expansion, NJPP estimates that 338,000 New Jersey residents will apply for a license during the first three years of implementation.

Restricting who is allowed to legally drive also has a chilling effect on the families and children of those who do not have the documents necessary to receive a driver’s license. In New Jersey, 168,000 children have undocumented parents who cannot drive them to and from school, their doctors appointments, sports games and practices, and other activities and errands parents make with their children. Instead, they are left relying on underfunded transit systems and spending money on taxis or Uber/Lyft drivers when that money could be going toward their children and spent in their local communities.

The proposed legislation, A4743, would create two categories of driver’s licenses and identification cards:

REAL-ID: a REAL ID Act-compliant driver’s license and identification card that residents can use to travel domestically on an airplane and enter federal buildings.

Standard License: a non-REAL ID basic license and identification card that would not be valid to board an airplane or to be used for certain official federal purposes. However, the non-REAL ID license would be valid for driving purposes and a form of identification.

What is REAL ID?

In 2005, the Congress passed and then-President George W. Bush signed the REAL-ID Act, legislation requiring driver’s licenses and identification cards to meet certain requirements set by the federal government to control who could board an airplane and hence make the country “more secure.” Specifically, the Real-ID Act calls for proof of legal presence in the United States and identity, a social security number, and state residency. The law also requires that applicants’ personal data and documents be entered into a state government database that is accessible to the federal government. These requirements are similar to the six-point system New Jersey currently has with the exception of the requirement to retain or scan documents into a DMV database. Despite there being no data that suggests the provisions in this law actually make driver’s licenses and identification cards more secure, the federal government is set to fully implement and enforce the REAL ID Act over the next two years.

States are not required to have their driver’s licenses and identification cards comply with the REAL ID Act, as there is no legal or financial punishment, but non-compliance will create a burden for residents of those states as they will need additional documentation, such as a passport, to fly domestically or enter federal buildings. The federal government will start enforcing the provisions of the REAL ID Act in New Jersey on October 10, 2020.

Is New Jersey REAL ID Compliant?

No, New Jersey’s licenses and identification cards are not compliant with the REAL ID Act, but state officials have signaled that they hope to change that in 2019. As of February 2019, 38 states are compliant, as well as Washington DC, Puerto Rico, and Guam. New Jersey is one of twelve states that is not compliant, and all twelve have received enforcement extensions into 2019 and 2020.

Who will benefit from A4743?

If New Jersey becomes REAL ID compliant without creating a standard license as an alternative option, many residents will be impacted by this change. The federal REAL ID Act’s requirements will make driver’s licenses out of reach for many, including undocumented immigrants, individuals earning less than $25,000 a year, and people reentering society from prison.

To ensure these residents, who may not have the funds and necessary documentation for a REAL ID, are able to legally drive and fully participate in society, New Jersey must create an alternative license. This is the only way to ensure that all New Jersey residents can continue to have access to a driver’s license and be able to protect their privacy.

Sponsored by Assemblywoman Annette Quijuano, A4737 would ensure New Jersey is compliant with the REAL ID Act while also creating an alternative standard license. Creating an alternative standard license would benefit the following people:

Citizens who do not want their information stored in a federal data system

Those who do not need a license to travel domestically

Certain senior citizens

Survivors of domestic violence who are unable to retrieve all their documents

Formerly incarcerated individuals

Low-income individuals and families

Transgender people whose documents may not accurately match their gender identity

Immigrants, including undocumented immigrants

Both citizens and noncitizens who have lost essential documents and have not yet obtained replacements because of cost or administrative delay

New Jersey has an opportunity to be REAL ID compliant and allow other qualified New Jersey residents the opportunity to be trained, licensed, and insured. It is a common sense policy that would make the Garden State’s road safer, allow children to arrive safely to school, help local economies to prosper, and establish a modeled system for the nation to follow.

Methodology

Estimating how many people who are undocumented would be impacted

To estimate the number of people who would get licenses if New jersey allows undocumented immigrants to apply, we start with the number of unauthorized immigrants who are 18 years and older. We use the experience of other states to predict the “take-up rate” for New Jersey—the share of unauthorized immigrants who would get licenses if the policy was changed. The number of unauthorized immigrants is drawn from the Center for Migration Studies (CMS), PEW Hispanic Center, and Migration Policy Institute Estimates of the Unauthorized Population; we take the average of the three estimates which is 484,000 and multiply that by the percentage of undocumented population that is 18 years and older,88 percent to give us the estimated number of folks who would benefit, 425,920. The share of age-eligible unauthorized immigrants who get a license within three years of implementation of the policy ranges from about a quarter (25 percent in Nevada) to about a half (47 percent in Illinois), according to the Fiscal Institute Policy. In New Jersey, we assume that the policy would be implemented well, and that the take-up rate would be at the top of this range. Our estimate is that (47 percent) of age-eligible unauthorized immigrants would get a license.

Calculating how many people earn less than $25,000

According to the IPUMS American Community Survey 2017, 1-year sample, an estimated 2.4 million U.S. citizens adults including naturalized citizens in New Jersey reported earning less than $24,999 and based on a study at least 12 percent of voting-age American citizens earning less than $25,000 per year do not have a readily available U.S. passport, naturalization document, or birth certificate. Hence, we multiple 2.4 million times 12 percent.

Calculating how many people reenter from the criminal justice system

According to the latest outcome report, “State of New Jersey Department of Corrections State Parole Board Juvenile Justice Commission (2016), 10,835 inmates were released in 2011. Based on the Motor Vehicles Affordability and Fairness and Task Force Final Report (https://www.state.nj.us/mvc/pdf/about/AFTF_final_02.pdf) studies show that at least 50 percent of those released out prison do not have access to identification. Thus, we multiplied 10,835 times 50 percent.

Calculating license revenue:

Under A4743, the cost of obtaining a “standard basic license” is $18 and an initial permit is $10 for a license, totaling $28. Under the first outcome, the three potential groups total is multiple by the 47 percent “take-up rate” (see number 1 for more). The second outcome only includes the undocumented population times the 47 percent “take-up rate” times the price of license plus permit. The recurring revenue calculates only the revenue for renewing the license.

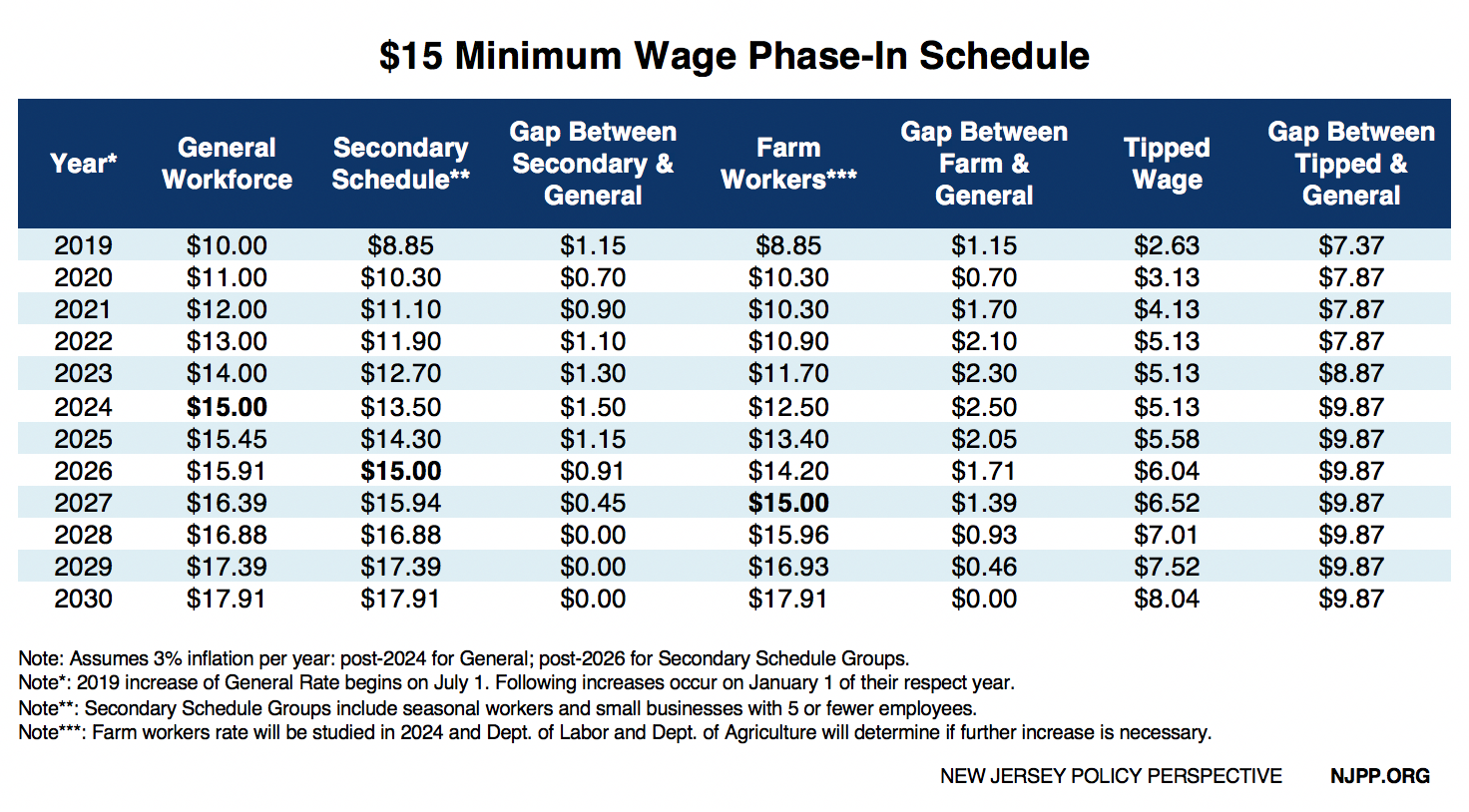

Earlier this month Governor Murphy and legislative leaders reached a deal to raise the state’s minimum wage to $15 by 2024, for most workers. Seasonal and small business employees will reach $15 by 2026, while farm workers will reach $15 by 2027, but only if the labor commissioner and secretary of agriculture sign off on it. The proposal is far from perfect — and unnecessarily complex as all work should be valued equally — but nonetheless it will have a tremendous positive impact for the Garden State’s low-paid workers and broader economy. Further, the minimum wage will remain indexed to inflation, and despite a slower phase-in for some, the legislation provides a pathway for all workers to reach the full minimum wage by 2030.

The Basics

NJPP has long-advocated for a $15 minimum wage for all workers to combat poverty and ensure all New Jerseyans can better support themselves and their families. The current minimum wage of $8.85 fails to reflect the state’s high cost of living and helps explain why four in ten New Jerseyans qualify as working poor, according to the United Way ALICE report. Raising the minimum wage to $15 an hour will boost the take home pay of nearly one million workers and inject billions of dollars into the state economy as families have more disposable income to spend in their local communities.

Assembly bill A15 is the current proposal to raise the minimum wage to $15 and is the culmination of a year-long deliberation between Governor Murphy, Senate President Sweeney, and Assembly Speaker Coughlin. The bill passed the Assembly Labor Committee on Thursday, January 24, and is being fast-tracked through the Legislature — the bill could pass both chambers and be signed by Governor Murphy by the end of the month.

The proposal makes new distinctions in New Jersey’s wage and hour law, so workers in certain sectors — in particular farmworkers, seasonal workers and employees at small businesses with five employees or less — will have to wait longer to reach a $15 minimum wage. Again, it is important to note that for these workers, the bill provides a pathway to parity, so all workers will have the same minimum wage from 2030 onward. This is critical because it prevents workers on the slower phase-in schedule from earning a sub-minimum wage in perpetuity. Instead, they will just be on a slower phase-in schedule but will eventually catch up to the full minimum wage and its yearly cost of living increases.

Unfortunately, this does not apply to tipped workers, as is detailed below, and further advocacy is necessary on behalf of both tipped and farm workers to ensure that the dignity of their work is fully valued and properly honored.

Phase-In Schedule (For Most Workers)

As specified in the bill, the current minimum wage of $8.85 will rise to $10.00 an hour on July 1, 2019, and to $11.00 an hour on January 1, 2020. From then on, the minimum wage will increase by $1.00 per hour every January 1st until it reaches $15.00 on January 1, 2024. Every year thereafter, the minimum wage will receive an inflationary bump, tied to the Consumer Price Index (CPI).

Secondary Schedule (Seasonal and Small Business Workers)

For seasonal workers, defined as “those who are employed by an employer that is a seasonal employer or non-profit or government entity, and not outside of the period of that year commencing on May 1 and ending September 30,” and employees at businesses of five workers or fewer, the minimum wage will rise at a slower rate and reach $15.00 an hour on January 1, 2026. The next two years will act as a catch up period, so that by January 1, 2028 these workers will earn the same minimum wage as everyone else, including cost of living increases. From 2028 onward, these workers will earn the full minimum wage and will be eligible for the same CPI increases as the general minimum wage.

Farm Workers

With regard to farm workers, the minimum wage for will increase to $12.50 an hour by January 1, 2024. At that juncture, a joint decision will be made by the state labor commissioner and secretary of agriculture on whether to recommend that the minimum wage for farm workers should continue to increase. If the two agree that the minimum wage should continue to increase, it will rise to $15.00 per hour by 2027, and will reach parity with all other workers by 2030 If the two parties cannot come to an agreement, a third member — as proposed by the governor and approved by the legislator — would break the tie and affirm the decision. If the state labor commissioner and secretary of agriculture make a recommendation to prevent further increases, the legislature would have to affirm that decision by passing a concurrent resolution.

While the different schedule for farm workers is less than ideal, it is important to note that absent both a recommendation not to continue on the specified path by the state labor commissioner and secretary of agriculture, and a concurrent resolution adopted by both houses of the legislature implementing the recommendation, the increases to $15 by 2027 remain in effect, as will further increases to catch up to the general minimum wage.

Tipped Workers

With regard to tipped workers, their minimum wage will increase to $5.13 per hour by 2022, where it will remain until 2024. Then, beginning in 2025, the wage will increase in concert with the general minimum wage, remaining $9.87 lower than the general minimum wage in perpetuity. NJPP has advocated for a full phase-out of the tipped wage as it improves the work experience for employees, guarantees a level of income that enables them to reliably budget for their lives, and very clearly makes a tip a tip again rather than being a critical portion of earnings that is necessary to afford the most basic of needs. We will continue to advocate for a full phase-out of the tipped wage, as is the law in seven other states, so that the labor of tipped workers is properly recognized and valued.

New Jersey is poised to become the 13th state in the nation to allow all residents, regardless of immigration status, to apply for a driver’s license. Doing so would increase public safety, bolster the state’s economy, and increase the well-being of all families, particularly the hundreds of thousands of New Jersey residents who would gain the right to legally drive.

How many New Jersey residents would benefit from expanded access to driver’s licenses?

There are approximately 466,000 undocumented immigrants in New Jersey who are of driving age and would be eligible for a license. Based on the experience of other states, NJPP estimates that half these eligible New Jerseyans – 233,000 – would receive a license within the first three years of implementation, a 3.8 percent increase in the total number of licensed drivers in the state. A higher number would likely apply for a license, but not everyone who applies passes the written and road tests.

Would allowing undocumented immigrants access to obtaining a driver’s license and insurance under their name increase premiums?

No. There is no evidence that undocumented immigrants obtaining a driver’s license raises premiums for the average driver. In fact, having more insured drivers who have been tested, trained, and licensed on the road would make everyone safer. Since auto insurance is compulsory in New Jersey, universal driver’s licenses would allow for thousands of drivers to obtain auto insurance coverage, thereby reducing the number of uninsured drivers, a cost that is currently borne by all insured motorists.In Utah, which has allowed undocumented immigrants to drive legally since 1999, the uninsured motorist rate dropped by 20 percent.

Do undocumented immigrants qualify for the Special Automobile Insurance Policy (SAIP), also known as the dollar-a-day auto insurance policy?

No. Undocumented immigrants do not qualify for the dollar-a-day (SAIP) auto insurance policy because they are not eligible for federal Medicaid benefits. Undocumented immigrants are barred from all social safety net programs (i.e. NJ Family Care, TANF, SNAP).

Do you need a social security number (SSN) to obtain auto insurance?

No. Insurance companies are not required by law to ask for a driver’s social security number (SSN). Insurers may ask for an SSN in their auto insurance application, but disclosing an SSN is not mandatory to obtain auto insurance.

Does auto insurance coverage or cost vary depending on the type of license you have? For example, some states have Real ID license; does it matter if you have a Real ID compliant license?

No. Having a certain kind of license does not bar individuals from certain types of insurance coverages. Also, under the current proposed expanded driver’s license legislation, insurance companies are barred from assigning anyone with the proposed provisional license to a rating plan.

Will drivers who obtain a license be vulnerable to violations of privacy if they get into an automobile accident?

Potentially. Ideally, restrictions to automobile accident reports would protect drivers from unsolicited legal notices that can mislead or scare people into thinking they need a lawyer simply because they were in an auto accident. People with provisional driver’s licenses should be confident that an auto accident does not jeopardize their privacy or subject them to unnecessary medical treatment and fraudulent activity.

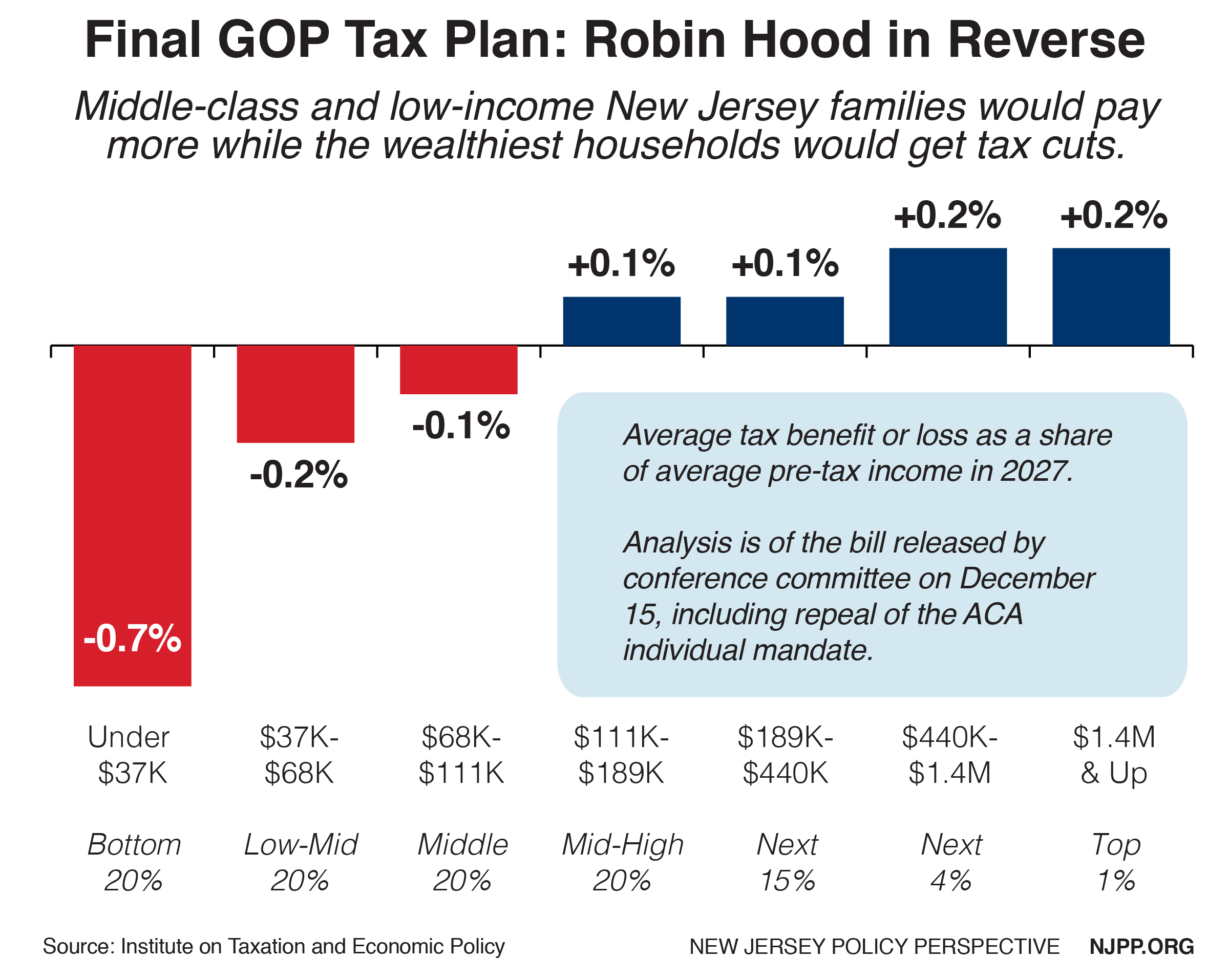

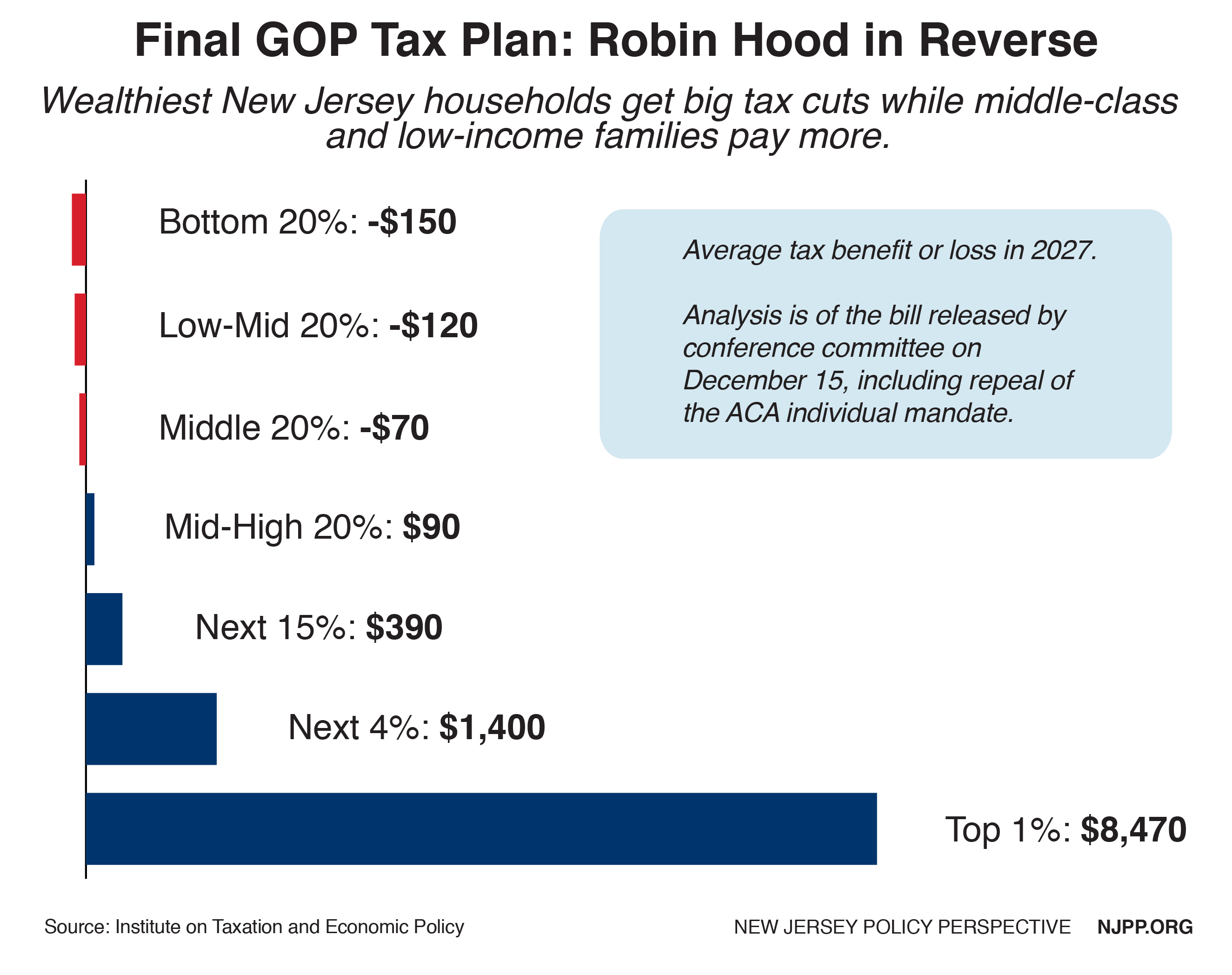

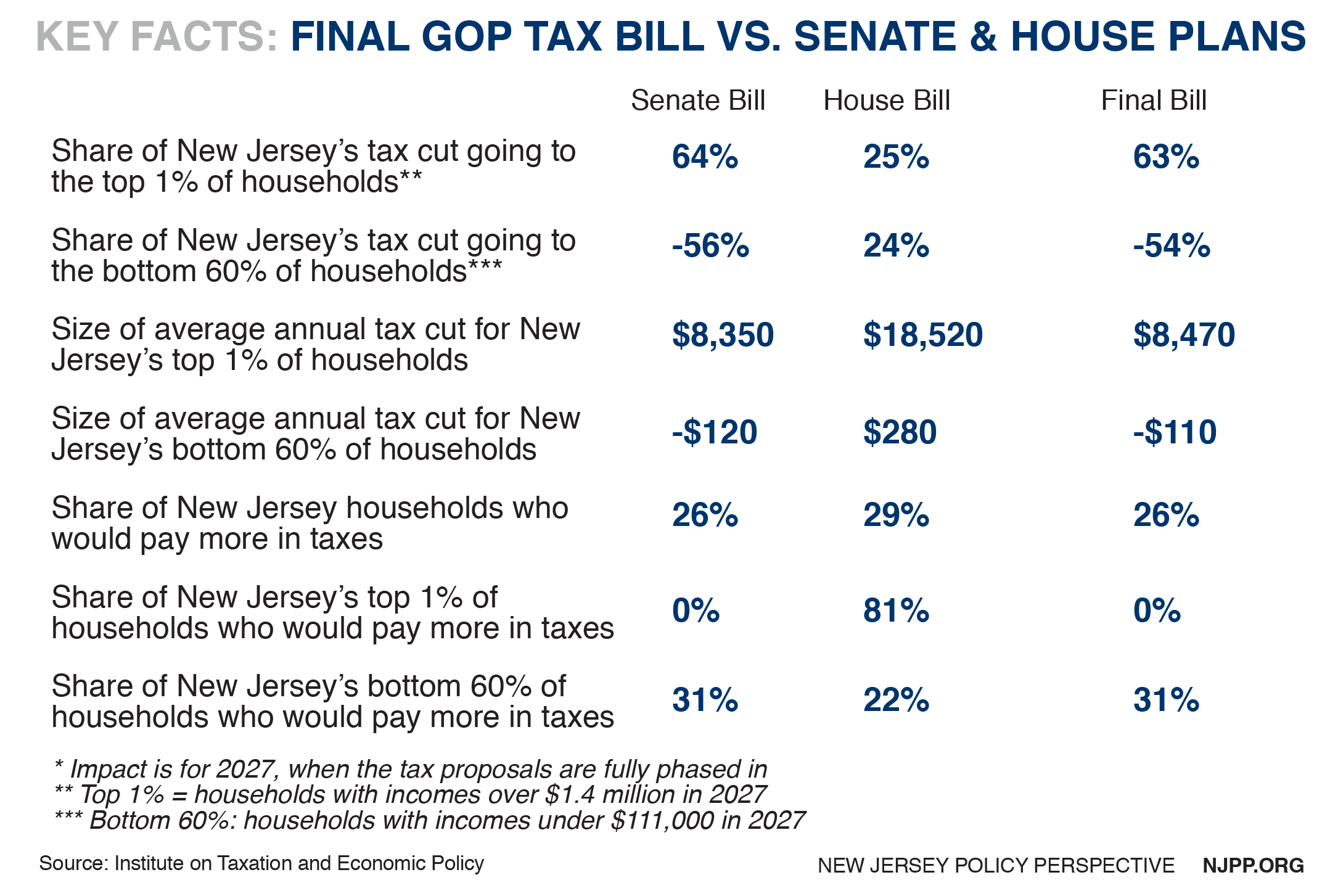

Once it is fully phased in, the federal tax proposal released by conference committee on December 15 would raise taxes for the average middle-class and low-income New Jersey family while cutting taxes for wealthier families and for large corporations. At the same time, it would increase the number of New Jerseyans without health insurance by 340,000 by 2027 thanks to the repeal of the Affordable Care Act’s individual mandate,[1] and would tee up deep and devastating budget cuts that would harm working families across New Jersey.

While all income groups in New Jersey on average would see a tax reduction in 2019 under the final GOP plan, it’s important to look at the impact in the year 2027, since the bill includes both permanent provisions (the tax cuts for corporations and a tax hike on working families through a change to how inflation is measured) and temporary provisions that expire after 2025 (the rest of the bill that directly affect families and individuals). Unless otherwise noted, this fact sheet looks at the impact on New Jersey families in 2027.

New Jersey households with incomes over $1.4 million (the top 1 percent) would receive an average $8,470 tax cut while the bulk of Garden State families (the bottom 60 percent, or those with incomes under $111,000) would see a tax hike averaging $110.[2] Taken all together, those families in the top 1 percent would receive 63 percent of the state’s share of the tax cut – $384.1 million in total – while the bottom 60 percent would, together, receive less than 0 percent of the tax cut, since they’d pay a total of $331 million more in taxes under the plan.

In all, about 1 in 4 New Jersey taxpayers (26 percent) would see a tax hike under the GOP bill,[3] a slightly lower share than the nation as a whole (27 percent) and the 22nd highest of the 50 states.

The plan is a clear example of Robin Hood in reverse, as it gives the largest average tax hikes to New Jersey’s poorest families while showering the state’s very wealthiest families with the biggest tax cuts. While just 1.6 percent of the state’s wealthiest 5 percent of families would see a tax hike, 31 percent of families in the bottom 60 percent would. That share of tax hikes for middle- and lower-income families is the 15th highest of the 50 states.

The final GOP bill is more similar to the Senate-passed bill than the House-passed bill, as you can see by looking at the impact of all three plans on New Jersey.

Corporate Tax Cuts Drive GOP Tax Plan’s Impact – and its Inequities

Big tax cuts for corporations – specifically a cut in the corporate income tax from 35 percent to 21 percent – are the centerpiece of the GOP tax plan. After all, they comprise most of the parts of the final plan that are permanent, while nearly all of the smaller tax cuts and changes for individuals and families are temporary. As a result, these breaks for corporations end up driving the overall impact of the GOP tax plan once fully phased in, as well as the plan’s inequity.

That’s because slashing the top corporate tax rate by nearly half will primarily benefit owners of corporate stocks, according to Congress’ own Joint Committee on Taxation.[4] In fact, despite President Trump’s insistence that average working families will get a “$4,000 pay raise” from this tax plan, just 25 percent of the long-term benefit of a corporate tax cut will go to workers.[5]

And of that already small share, an even smaller piece will go to middle-class or low-income workers, since fewer than half of all Americans own any stock, and overall shareholder wealth is – like most of the rest of the country’s wealth – extremely concentrated at the top (the top 10 percent of Americans own about 80 percent of the value of the total stock market, according to leading economist Ed Wolff).[6]

The bulk of the benefit from the corporate rate cut – three-quarters of it, in fact, – will go to shareholders, and a good chunk of that will flow to foreign investors, who own about 35 percent of stocks in American corporations.[7]

Tax Bill is Step One of a Damaging Two-Step Tax & Budget Agenda

Unfortunately, the pain for New Jersey’s working families does not end with the direct impact of this tax bill. In fact, the tax bill is step one of Congressional Republicans’ two-step tax and budget agenda that would rip the American social contract to shreds, undo decades of progress for working Americans and send the country hurtling even faster toward a new gilded age.[8]

Here’s how this two-step agenda works. First, enact costly tax cuts now that are heavily skewed toward wealthy households and profitable corporations. Next, use the cost of those tax cuts and their negative impact on the federal deficit as a rationale to cut public services, programs and investments on which all Americans – particularly low- and moderate-income residents – rely.[9]

We don’t need to wildly guess what will be on the chopping block when GOP lawmakers get to this second step. After all, they have already outlined deep and severe budget cuts in their long-range budget plans.

For New Jersey, these budget plans have included devastating cuts to programs that expand economic opportunity for all residents, including job training, education, and economic development programs in cities and rural communities. But the proposals’ cuts would fall hardest on Garden State residents struggling in today’s economy, with reductions to programs that provide income assistance to help families get back on their feet and help nearly 900,000 New Jerseyans afford groceries through SNAP, and additional cuts to Medicaid, which provides health care to about 1.8 million New Jerseyans – including 852,000 kids.[10]

Endnotes

[1] NJPP analysis based on Congressional Budget Office estimates using weighted average for employer-based, marketplace, and Medicaid expansion coverage.

[2] Institute on Taxation and Economic Policy (ITEP) Microsimulation Tax Model, December 2017. Model includes all major components of the tax bill, including personal income tax changes, changes to deductions, corporate tax changes and estate tax changes. Full dataset and methodology available at https://itep.org/finalgop-trumpbill/

[3] This report’s key findings on the distribution of the tax plan focus on average and total tax hikes or cuts by income group. This explains why, for example, the bottom 60 percent would, on average, and, in total, pay more in taxes, even while there are individual taxpayers inside that income group who would pay less – the tax cuts they receive are just overwhelmed by the tax hikes that others in the same income group would see.

[5] ITEP and JCT both assume that in the short run, a corporate tax cut will benefit the owners of corporate stocks alone, but in the long run (usually assumed to be ten years after enactment) a quarter of the benefits will flow to workers.

When President Trump ended the Deferred Action for Childhood Arrivals program earlier this year, he left almost 800,000 DACA recipients – including 17,400 New Jerseyans – to face an unknown future.[1] Now Congress must act to protect these and other young, striving immigrants by passing the Dream Act of 2017.[2] Doing so could brighten the futures of tens of thousands of young New Jerseyans while boosting the state’s economy. However, a Congressional fix for young immigrants should not be used as a vehicle for increased spending to increase border enforcement, expand immigrant detention, further militarize border communities or build a wall on the southern border.

Tens of Thousands of New Jerseyans Would Have Brighter Futures

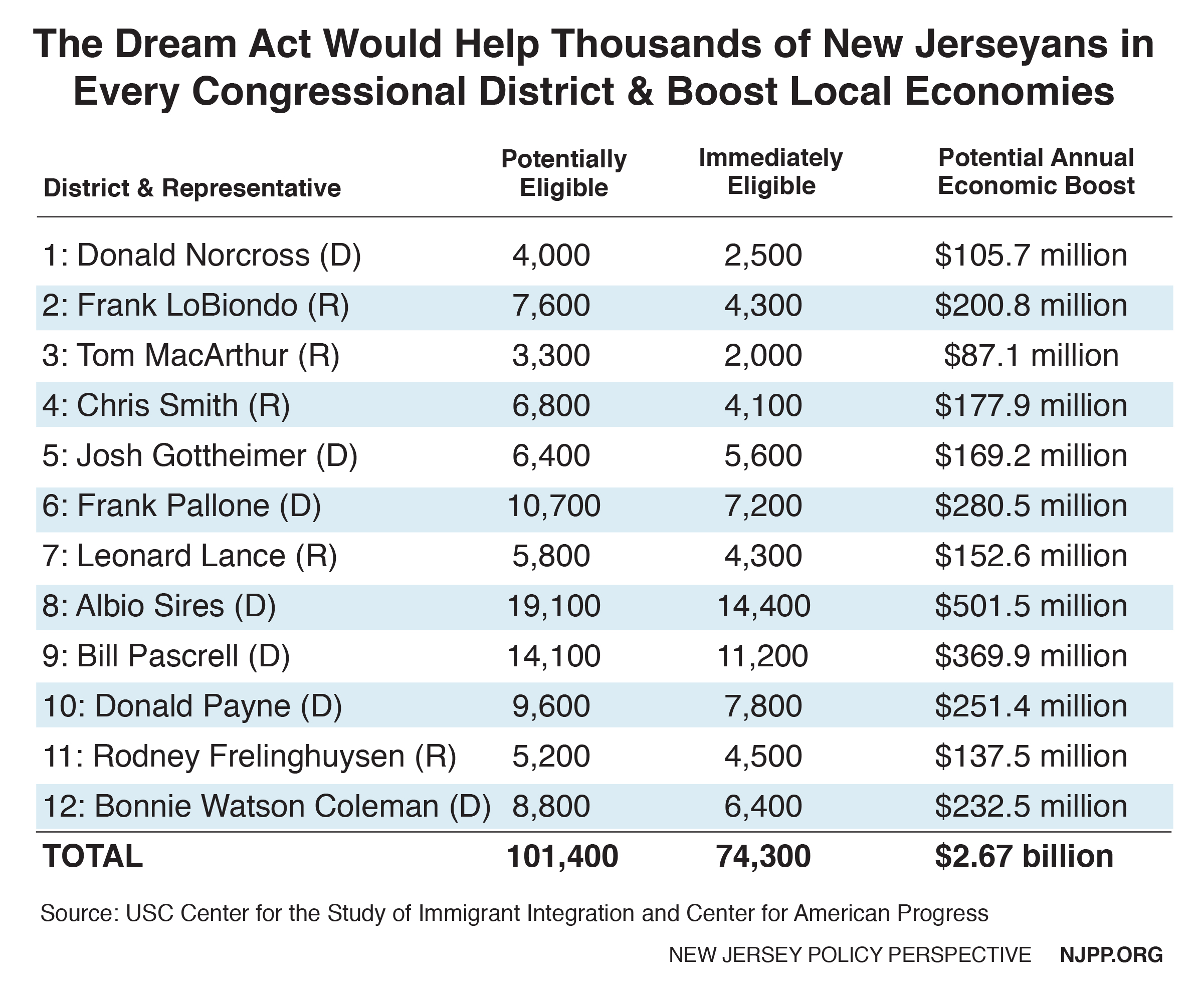

An estimated 101,000 New Jerseyans could benefit from the Dream Act of 2017. These are people who entered the U.S. before they turned 18 and have been in the country for four continuous years.

Of these New Jerseyans, 74,000 would immediately qualify for Conditional Permanent Residence (CPR) status under the law.[3] This is the first step in the bill’s process for becoming a legal permanent resident (LPR).

Of the New Jerseyans who could benefit from the Dream Act, 61,000 are in the workforce; this is the seventh highest of all the states.[4]

These New Jerseyans live all over the state, with thousands of eligible young immigrants residing in every Congressional District.

New Jersey’s Economy Would Benefit

Passing the Dream Act and putting these New Jerseyans on a path to legal status could boost the state’s economy by at least $800 million each year – the sixth largest increase of all the states.[5]

The longer-term payoff for New Jersey’s economy is even greater. For example, if just half of the working New Jerseyans who are eligible for the Dream Act complete the transition from CPR status to LPR status by pursuing additional education, New Jersey’s economy would see an economic boost of up to $2.7 billion each year[6] – this impact is spread throughout all Congressional Districts, with every District but one seeing an economic benefit of $100 million or more.

Eventually, the economic boats lifted by the rising tide of the Dream Act would modestly boost the average incomes of all Americans by $82-$273 a year.[7]

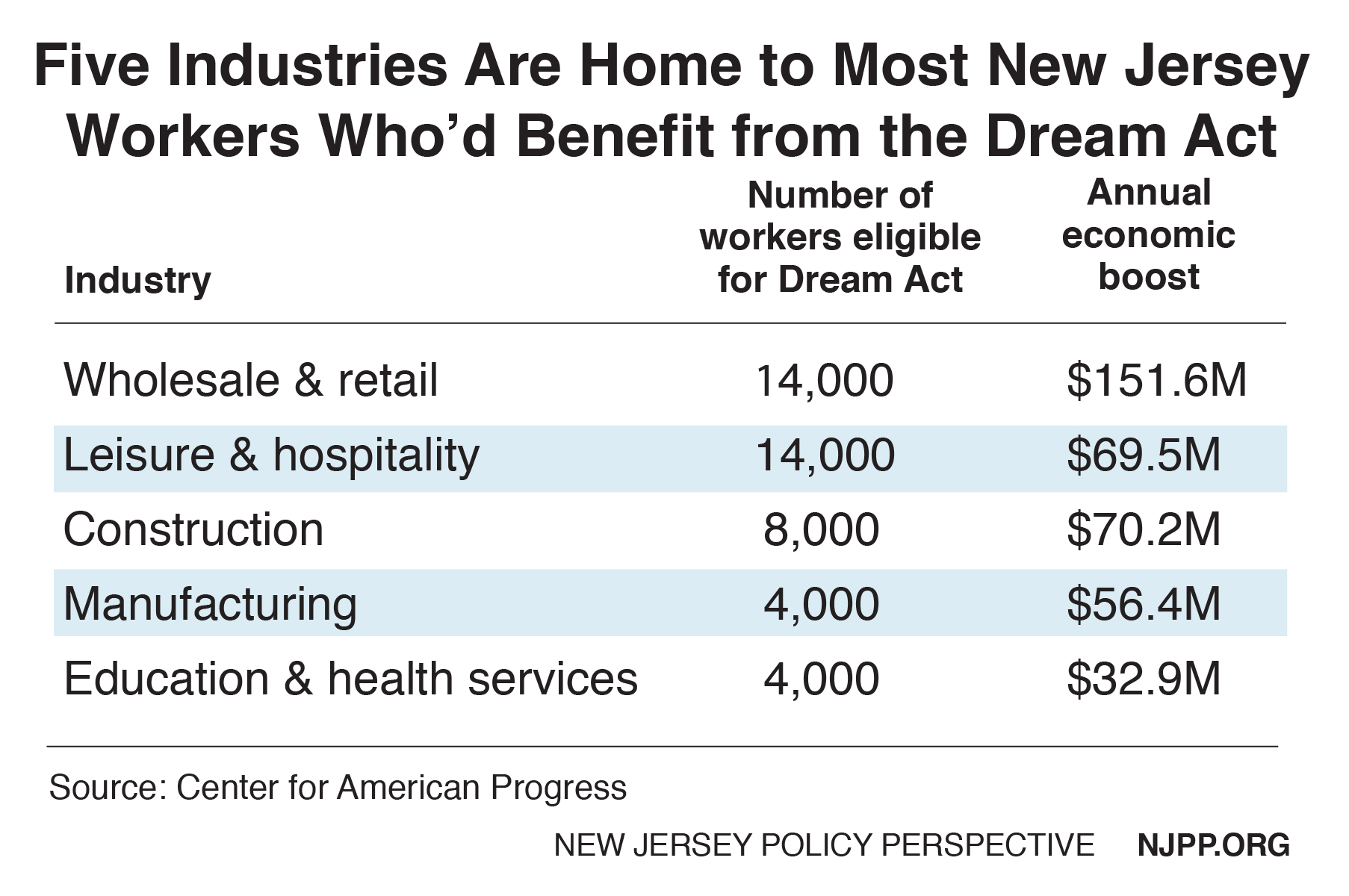

Nearly 3 in 4 New Jerseyans (72 percent) who could benefit from the Dream Act and are in the workforce work in five industries: wholesale and retail, leisure and hospitality, construction, manufacturing, and education and health services. These five industries would see a large chunk of the economic gains from the Dream Act as well.

Without the Dream Act, New Jersey Would Suffer

The consequences to New Jersey of the Dream Act not becoming law are dire:

Without a DACA fix, tens of thousands of young New Jerseyans would lose work permits and protection from deportation over the next two and a half years.

The loss of DACA alone would cause New Jersey’s economy to lose an estimated $1.6 billion each year – the fifth largest dollar loss of all states.[8]

It would also make more immigrants vulnerable to wage theft, workplace exploitation and discrimination based on their legal status; lead to economic distress in many households that invested in buying homes, businesses and other investments; and create a higher risk of family separation and deportation.

Endnotes

[1] New Jersey Policy Perspective, Fast Facts: DACA Directive Dims the Future of Thousands of Young New Jersey Immigrants, September 2017. https://www.njpp.org/reports/fast-facts-daca-directive-dims-the-future-of-thousands-of-young-new-jersey-immigrants

[2] Dream Act of 2017, S. 1615, 115 Congress, https://www.congress.gov/bill/115th-congress/senate-bill/1615/text, 2017.

[3] USC Center for the Study of Immigrant Integration analysis of pooled 2010-2014 American Community Survey microdata from IPUMS-USA. http://dornsife.usc.edu/csii/interactive-map-dream-act-2017/

[5] Center for American Progress. The State-by-State Economic Benefits of Passing the Dream Act, October 2017. https://www.americanprogress.org/issues/immigration/news/2017/10/26/441298/the-state-by-state-economic-benefits-of-passing-the-dream-act/

[7] Center for American Progress. The Economic Benefits of Passing the Dream Act, September 2017. https://www.americanprogress.org/issues/immigration/reports/2017/09/18/439134/economic-benefits-passing-dream-act/

[8] Center for American Progress, A New Threat to DACA Could Cost States Billions of Dollars, July 2017. https://www.americanprogress.org/issues/immigration/news/2017/07/21/436419/new-threat-daca-cost-states-billions-dollars/

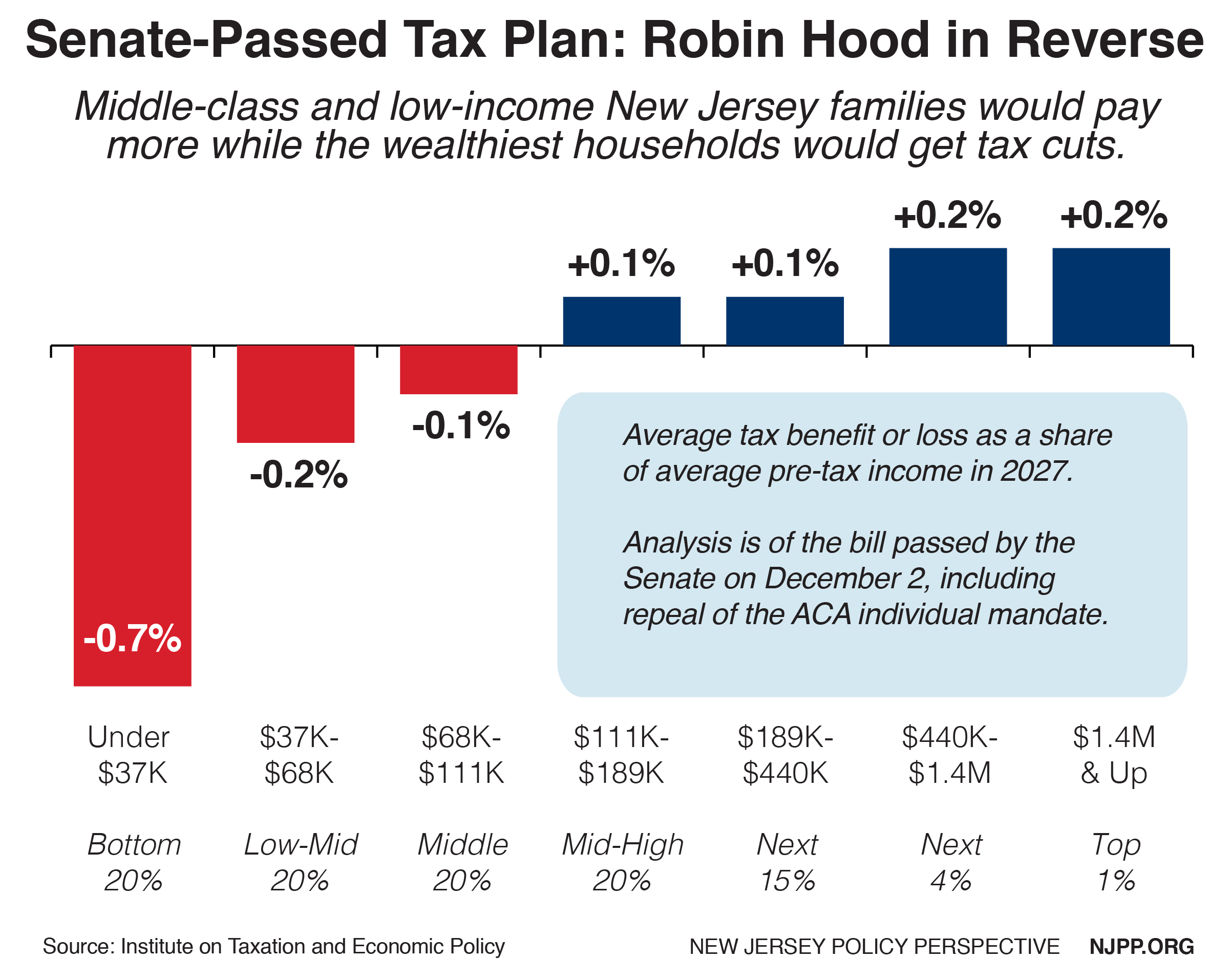

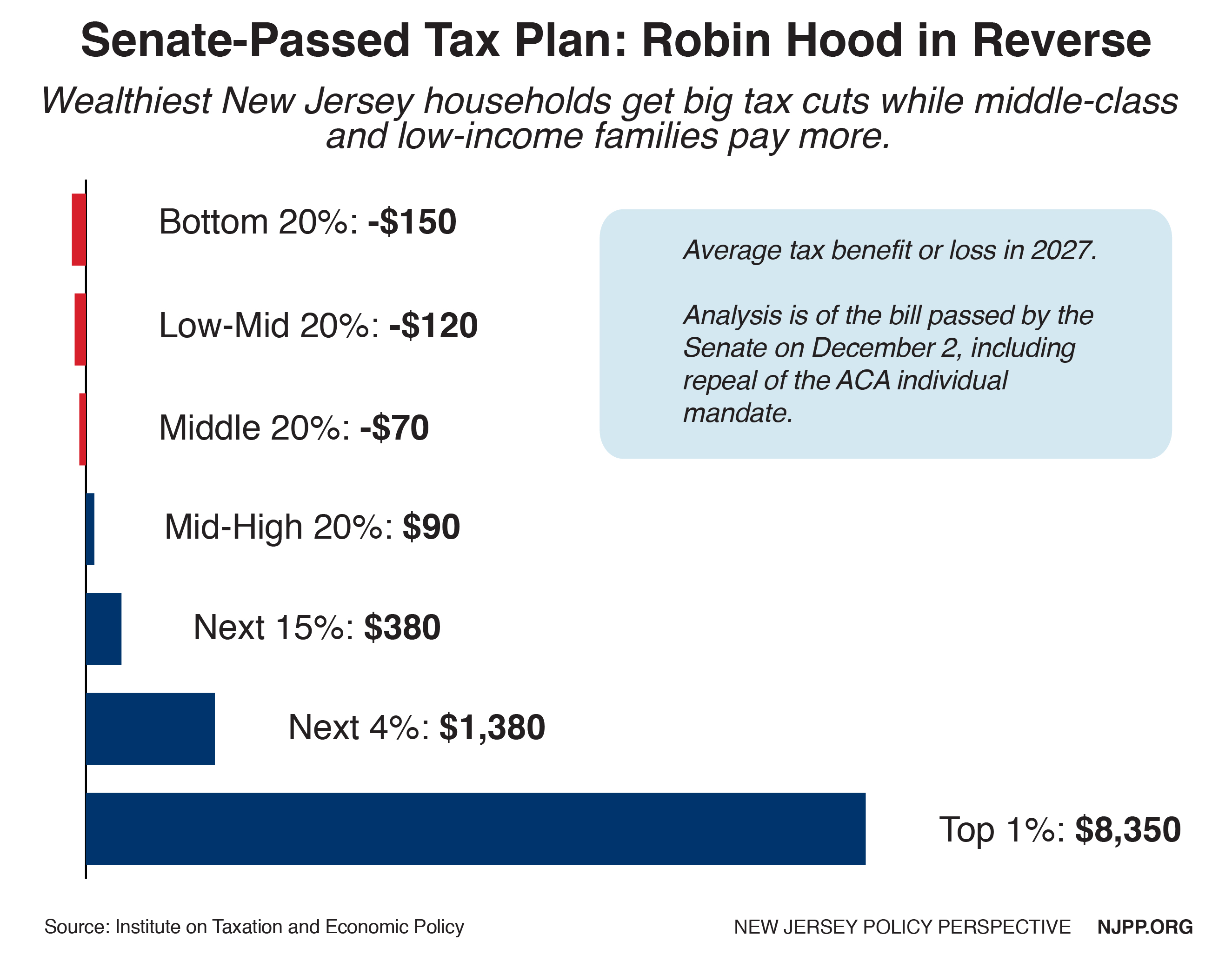

The federal tax proposal passed by the U.S. Senate on December 2 would raise taxes for the average middle-class and low-income New Jersey family while cutting taxes for wealthier families and for large corporations. At the same time, it would increase the number of New Jerseyans without health insurance by 340,000 by 2027 thanks to the repeal of the Affordable Care Act’s individual mandate.[1](Unless otherwise noted, all data in this Fast Facts is on the impact in the year 2027, once the plan is fully phased in.)

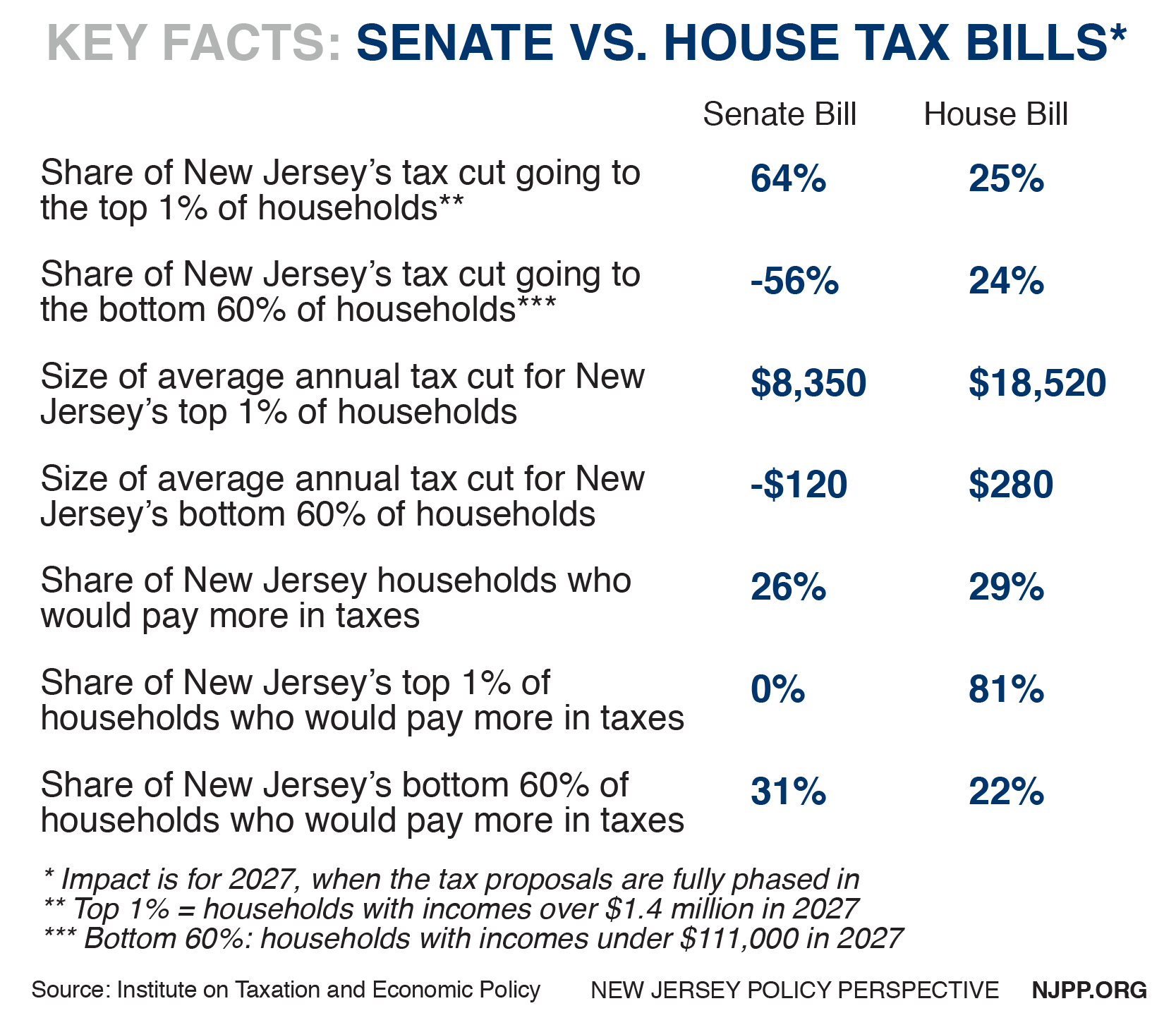

New Jersey households with incomes over $1.4 million (the top 1 percent) would receive an average $8,350 tax cut while the bulk of Garden State families (the bottom 60 percent, or those with incomes under $111,000) would see a tax hike averaging $120.[2] Taken all together, those families in the top 1 percent would receive 64 percent of the state’s share of the tax cut – $378.8 million in total – while the bottom 60 percent would, together, receive less than 0 percent of the tax cut, since they’d pay a total of $333.7 million more in taxes under the plan. In all, about 1 in 4 New Jersey taxpayers (26 percent) would see a tax hike under the Senate-passed bill.[3]

The plan is a clear example of Robin Hood in Reverse, as it gives the largest average tax hikes to New Jersey’s poorest families while showering the state’s very wealthiest families with the biggest tax cuts. While just 1.6 percent of the state’s wealthiest 5 percent of families would see a tax hike, 3 in 5 families in the bottom 60 percent would.

By just about every measure, the Senate-passed bill is worse for New Jersey’s working-class and middle-class families than the House bill, which was quite damaging for these families already.

The pain for New Jersey’s working families does not end with the direct impact of this tax bill, unfortunately. In fact, the tax bill is step one of Congressional Republicans’ two-step tax and budget agenda[4]: enact costly tax cuts now that are heavily skewed toward wealthy households and profitable corporations, then use the cost of those tax cuts and their negative impact on the federal deficit as a rationale to cut public services, programs and investments on which all Americans – particularly low- and moderate-income residents – rely.[5]

State and Local Tax Deductions Remain On the Chopping Block

The Senate-passed bill – like the House-passed bill – eliminates taxpayers’ ability to deduct state/local income or sales taxes paid while capping the amount of property taxes one could deduct at $10,000. A total of 41 percent of Garden State households currently file using these deductions – the third highest share of all states, after Maryland and Connecticut. Slightly more New Jerseyans claim the income or sales tax deduction (1.8 million) than claim the property tax deduction (1.6 million). Garden State households deduct a total of $32.2 billion in state and local taxes each year, the third highest dollar amount after California and New York.[6]

While the property tax provision has been pitched as a “compromise” to win over reluctant lawmakers from New Jersey and other similar states, an estimated 54 percent of Garden State taxpayers who currently claim the property tax deduction would no longer do so under the Senate-passed bill. And those most likely to lose the deduction are middle-class families – in fact, 60 percent of current middle-income claimants of the property tax deduction would lose it, while just 1 percent of current high-income claimants would.[7]

That’s because even though they’d still technically be able to take the property tax deduction, many would choose not to because the combination of itemized deductions (which would no longer include state income and sales taxes) would be smaller than the standard deduction. This would be a bad deal for many taxpayers because even as the Senate-passed bill increases the standard deduction, it eliminates personal exemptions would be eliminated. Even if the standard deduction were tripled (and it’s not even doubled under the Senate-passed bill), a significant portion of families that now itemize their deductions would still end up with tax increases.[8]

In all, New Jerseyans would likely deduct nearly $27 billion less in state and local taxes under the Senate-passed bill than they do now.[9]

Endnotes

[1] NJPP analysis based on Congressional Budget Office estimates using weighted average for employer-based, marketplace, and Medicaid expansion coverage.

[2] Institute on Taxation and Economic Policy Microsimulation Tax Model, December 2017. Model includes all major components of the tax bill, including personal income tax changes, changes to deductions, corporate tax changes and estate tax changes. Full dataset and methodology available at https://itep.org/housesenatetaxplans-dec17/

[3] This report’s key findings on the distribution of the tax plan focus on average and total tax hikes or cuts by income group. This explains why, for example, the bottom 60 percent would, on average, and, in total, pay more in taxes, even while there are individual taxpayers inside that income group who would pay less – the tax cuts they receive are just overwhelmed by the tax hikes that others in the same income group would see.

[4] Center on Budget and Policy Priorities, Budget Briefs: The Republican Two-Step Fiscal Agenda, November 2017. https://www.cbpp.org/budget-briefs-the-republican-two-step-fiscal-agenda

[5] The Washington Post, GOP eyes post-tax-cut changes to welfare, Medicare and Social Security, December 2017. https://www.washingtonpost.com/news/wonk/wp/2017/12/01/gop-eyes-post-tax-cut-changes-to-welfare-medicare-and-social-security/?utm_term=.7f251e2e56bf

[6] New Jersey Policy Perspective, Fast Facts: Millions of New Jerseyans Deduct Billions in State & Local Taxes Each Year, November 2017. https://www.njpp.org/budget/fast-facts-millions-of-new-jerseyans-deduct-billions-in-state-local-taxes-each-year

[8] Government Finance Officers Association, Impact of Eliminating the State and Local Tax Deduction (Updated with 2015 IRS Data), 2017. http://www.gfoa.org/sites/default/files/RCC%20Report%20on%20SALT%20Deduction-092017_Final.pdf

[9] NJPP analysis using data and estimates from Ibid 2 and actual dollar amounts currently deducted by New Jersey households from Ibid 6