By Gordon MacInnes and Sheila Reynertson, President and Senior Policy Analyst. Research assistance: Yixin Liu, Neha Mehta, Paul Siracusa, Annelisa Steeber, Jared Sussman

To read a PDF version of this report, click here.

This November, New Jersey voters will consider a constitutional amendment to permit the expansion of casino gambling to North Jersey. The proponents of this expansion claim that:

- Two North Jersey casinos will save Atlantic City from failing as a tourist destination

- The construction and operation of the two casinos will spark a boom in jobs and economic activity

- Struggling seniors and disabled New Jerseyans will be assisted with more generously funded benefits

- The shrinking equine industry will receive a subsidy to preserve jobs and economic activity

These are hefty promises, and as such they are worth exploring. But is casino expansion all it’s cracked up to be? The short answer is “absolutely not.”

Gambling on Casinos to Revive Atlantic City: Short-Term Win, Long-Term Failure

When New Jersey voters approved a 1976 amendment allowing casinos to open in Atlantic City, it created a monopoly on casino gambling in the middle of one of the world’s largest and richest markets with Las Vegas as its only competitor. Just 40 years later, Atlantic City’s casino industry has rebalanced itself following the shuttering of five casinos, but unemployment is at record levels and its municipal government is close to declaring New Jersey’s first bankruptcy since the Great Depression. There is now a heated war of words over the best way to “save” Atlantic City between those who advocate creating competing casinos in North Jersey and those who point to the cannibalization of the gambling market in neighboring states that triggered the crisis.

Proponents of the 1976 casino legalization, operating as the “Committee to Rebuild Atlantic City,” saw casinos as the savior that Atlantic City needed. Their campaign centered on casinos as the means to turn Atlantic City into a magnet for convention and family tourism.

The 1977 Casino Control Act stated that the two goals of casino gambling were to revive Atlantic City’s tourism industry and to spur urban redevelopment.[1] Codified in the legislation was the optimistic promise that casino gambling would “fix” Atlantic City. The language of the law clearly implies that casinos were never intended to be the sole attraction of the City’s tourist economy.[2] Unfortunately, almost all the new economic activity and job creation was concentrated in those blocks occupied by the 12 licensed casinos. Neither the State nor Atlantic City focused their attention on the creation of non-gambling attractions beyond the construction of the Convention Center and a modernized rail station.

As Casinos Flourished, the Rest of the City Faded

The first casino to open was Resorts International in 1978,[3] as it was the only then-existing hotel in Atlantic City that possessed at least the 500 rooms required by the Casino Control Act that its owners helped write.[4] Resorts enjoyed a 13-month monopoly before Caesars Boardwalk Regency opened. By 1987, Atlantic City boasted 12 casinos and established itself as a premier gambling destination.

While the number of visitors during that first decade skyrocketed nearly five-fold,[5] casinos alone reaped most of the benefits of the boom. New visitors came to Atlantic City with no reason to leave the casinos, since they housed restaurants, shops, spas, gyms and performance theatres. In fact, many of Atlantic City’s most iconic businesses closed their doors shortly after casino gambling took off.[6]

This is not a historical accident, but a result of policy. The 500-room minimum in the Casino Control Act limited applications for casino licenses to resort-style hotels that catered to tourists’ every need.[7] This made it extremely difficult for non-gambling tourist businesses to develop.

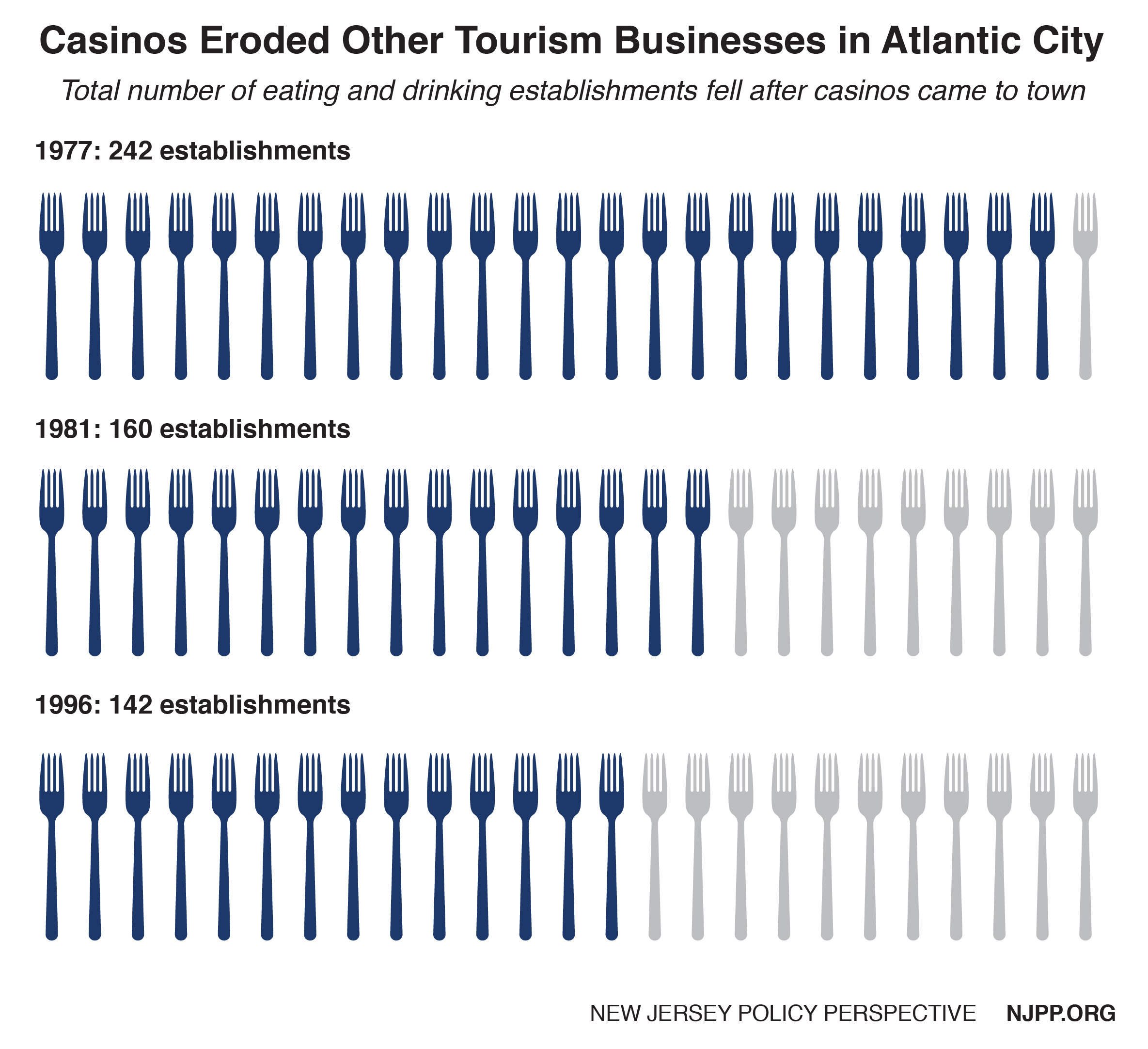

For example, before casinos arrived in Atlantic City there were 242 eating and drinking establishments. By 1996, just 142 were left – including the many bars, cafes and upscale restaurants inside the casinos.[8]

For example, before casinos arrived in Atlantic City there were 242 eating and drinking establishments. By 1996, just 142 were left – including the many bars, cafes and upscale restaurants inside the casinos.[8]

Casinos became the centerpiece of Atlantic City’s tourism offerings. But the promise that casinos’ good fortunes would spill over to the city’s broader tourist economy was never fulfilled as casinos monopolized tourism in Atlantic City and local and state governments did little to stimulate non-gambling attractions.

A Lack of Urban Redevelopment

The other promise of casino gambling in Atlantic City – urban redevelopment and revitalization – has been largely ignored as any drive around the city will confirm. Particularly as the number of casinos shrinks, it’s clear that the economic fortunes of Atlantic City remain unsustainably tied to a single industry.

Initially, the Casino Control Act required casinos to pay a portion of their revenues directly to the redevelopment of the city to ensure that the rest of Atlantic City reaped the benefits from casino gambling.[9] But there was a loophole. Casinos could either designate two percent of their revenue to Atlantic City revitalization or retain the revenue for five years and pay it as a tax to New Jersey.[10] Every casino chose the second option.[11] This meant that the funding for redevelopment in Atlantic City was delayed and promises of revitalization unfulfilled.

So in 1984, New Jersey created the Casino Reinvestment Development Authority (CRDA) to oversee the revitalization of Atlantic City.[12] The state flipped the incentive for the casinos by offering two options: spend 1.25 percent of gross revenue on CRDA-issued bonds for urban and economic development, or pay a 2.5 percent tax to the state. This time all the casinos chose the first option.

But over time, the redevelopment mission was diluted by the legislature, allowing CRDA to spend money on tourism-related activities that directly benefited the casinos – investment that was initially banned.[13] The casino industry – not Atlantic City – became a major beneficiary of CRDA’s investments that focused on new conference centers and restaurant facilities on casino premises.

As New Jersey’s East Coast Monopoly Ended So Did the Growth in Revenues

Despite having an East Coast monopoly on casino gambling for more than 26 years, New Jersey levied a tax of just 8 percent on gambling winnings of Atlantic City’s casinos[14] – just a touch higher than the state’s pre-1980 corporate income tax of 7.5 percent.

Overall, revenues from casino gambling grew steadily until 2006 when they topped off at $502 million. Then, revenues began to decline rapidly.[15] Tax revenues from casinos are now hovering in the $200 million range – levels last seen in the mid-1980s.

The economic decline of Atlantic City and the steady reduction in state revenues was accelerated primarily by the expansion of gambling in neighboring states.[16]

Pennsylvania legalized slot machines in 2004, saw the opening of its first casino in 2006 and offered table games in 2010.[17] By 2012, four Pennsylvania casinos were located in the metropolitan Philadelphia area. Another Philadelphia casino is slated to open this year.[18] Within a decade, Atlantic City lost about a third of its customer base.

Pennsylvania casinos pay a 34 percent tax on slot machines and other electronic games, and a 14 percent tax on table game revenue.[19] In 2011, the last year that casino winnings in Pennsylvania were less than New Jersey’s ($3.0 billion vs. $3.3 billion), tax collections were more than five times higher in the Keystone State ($1.5 billion) than the Garden State ($278 million).[20]

Gambling in Pennsylvania isn’t the only competition hurting Atlantic City. Delaware, Maryland, New York and Connecticut have all introduced or expanded gambling, carving up the market’s customer base and eating away at tax revenue potential for the entire northeastern region.

Lesson number one: New Jersey and Atlantic City failed to exploit their monopoly on casino gambling by tending to the casinos and little else.

Without Knowing Tax Rates How Can We Talk About Revenue?

Its proponents say casino expansion will help rescue Atlantic City, dramatically increase support for struggling seniors and the disabled, help the fading horse racing industry and help host municipalities and counties. The number commonly cited is $500 million in new revenue each year, with at least $200 million going to seniors and the disabled and $200 million to assist rebuilding Atlantic City. But essential questions about the taxes to be imposed and who decides about their distribution remain unanswered.

The two presiding officers of the Assembly and Senate have refused to indicate what level of taxation would be imposed on the two casinos. This lack of transparency on their part makes the promises of the proponents close to worthless.

Assemblyman Caputo, a former casino executive and a prime sponsor of the referendum, finally introduced in mid-September a non-binding resolution to frame the tax rates and the uses of the revenue. Caputo voiced concern that there was insufficient transparency to guide voters’ judgments. His resolution expands the uses for the expected revenues to also include “infrastructure and public places” at the county level and “transportation improvements and airport enhancements.” Expanded uses threaten, of course, to further reduce the funds that would be available for Atlantic City.

An earlier supporter of tax rates in the 40 to 60 percent range, Caputo’s resolution would assess a tax rate that is characterized as “considerably higher” than the rate imposed on Atlantic City, but would be “tiered” to reflect the scale of investment.[21] This first inkling of the tax rate range must have been music to the ears of the two most likely developers, particularly Jeff Gural of the Meadowlands who earlier had suggested that a 55 percent tax rate was fair but now says nothing more than 35 percent is acceptable. Paul Fireman, the Jersey City waterfront developer, threatened that any tax even as high as 35 percent would lead to a cutback in the scale of his casino.

A concurrent resolution filed 50 days before the public must vote on the casino referendum may be better than no information at all. However, Caputo’s effort is too late.

Given the stubborn failure of the legislative leadership to even post legislation that sets the prospective tax rate on North Jersey casinos, there is no way to correctly forecast the revenues that will be available for seniors, the disabled or Atlantic City. Given the false promises of the past, healthy skepticism is advised.

Lesson number two: Claims promising that North Jersey casinos will produce revenues adequate to rescue Atlantic City and expand assistance to seniors and the disabled should be treated as speculation and hypothesis.

Transportation Infrastructure: How to Deal with Congestion, and Who Will Pay?

To be successful, North Jersey casinos will require improved roads and public transit, a burden that cannot simply be handed off to the municipalities and counties selected for the two casinos.[22]

Proponents of a Meadowlands casino boast that their location is just 15 minutes away from Manhattan. While the extreme west side of Manhattan might be that close on a quiet August weeknight, the idea of a 15-minute jaunt from anywhere else in Manhattan is close to fantasy. And the two major routes through the Meadowlands are already two of the state’s most congested highways, yet no plans are in place to change either transit or highway access to the Meadowlands.

The proposed Jersey City site is convenient to the Turnpike Extension’s exit 14B (just before the frequently backed-up Holland Tunnel), but a fair distance from the Bergen-Hudson Light Rail station and not walkable from the nearest PATH station. Given its waterfront site, the proposed casino is plainly aimed at the New York City market and its 50 million annual tourist visitors.

Yes, the Hudson River can be crossed by ferries, and a ferry port is a part of the plans advanced by developer Paul Fireman. That’s great for some visitors. But a big part of his pitch is the creation of 6,000 unionized jobs to operate the casino.[23] In the absence of any convenient and affordable public transit near the site, how will all those workers get to work on a 24-hour daily schedule? This is a particularly important question for the Jersey City residents and other nearby municipalities who presumably would fill many of the lower-paid positions in the casino, restaurants and hotel.

Lesson number three: New Jersey has no plans in place to improve transportation to proposed casino sites in Jersey City and the Meadowlands.

Casino Expansion Will Decimate, Not ‘Save,’ Atlantic City

Despite a sharp decline in Atlantic City casino revenues following the Pennsylvania market competition, a saturated regional market and New Jersey’s history of disappointingly oversold gambling endeavors, casino expansion supporters tout hundreds of millions of dollars in tax revenue, thousands upon thousands of jobs and – crucially – a helping hand for Atlantic City.[24]

The three leaders who are central to approving policy changes in New Jersey – the Governor, Assembly Speaker and Senate President – all support the casino expansion referendum and suggest it will boost Atlantic City.

And prospective casino developer Jeff Gural asserts that only the passage of the referendum will save Atlantic City from being “finished” and that it can use the “$200 million a year for 15 years” to develop non-gambling attractions. He estimates that two North Jersey casinos will pay $500 million in taxes, ‘two and a half times what 7 or 8 casinos in Atlantic City” pay.” He also states that he would invest in Atlantic City “in a heartbeat” if North Jersey casinos are approved.[25]

These big promises sound all too familiar. But will New Jersey repeat its mistakes by accepting these exaggerated promises? Remember the lesson from the opening of Pennsylvania’s casinos: over a ten-year period beginning in 2004, Atlantic City lost about one-third of its “convenience’ gamblers and in 2014 one-third of its casinos shut down. Given that at least one-third of its remaining customer base resides in North Jersey, why would the results not be the same?

Mr. Gural’s optimism and his guarantee that Atlantic City can realize $200 million annually for 15 years raises the stakes on the tax rate required to generate such certain funding. His math also collides with the mandate of the referendum legislation.

First, the amendment limits Atlantic City’s share of the casino tax collections to not more than one-third of the revenues collected in any fiscal year. Second, Atlantic City’s share of revenues declines by 10 percent with every $150 million collected up to $450 million (at which point Atlantic City would receive $180 million). Given these facts, for Atlantic City to realize its $200 million in the first full year of both North Jersey casinos operating would require tax collections of $610 million – a target that no advocate has advanced.

In June, Fitch ratings issued its analysis of the impact of North Jersey casinos on Atlantic City, finding that at least three Atlantic City casinos would be shut down by the advent of new casinos. While the most vulnerable of those identified – Trump Taj Mahal – has already closed, both the Golden Nugget and Resorts are the other two identified as not being able to sustain what is expected to be a 20 percent reduction in gambling winnings.[26] Even the “breathing space” of four years or so it would take to authorize, license and construct two large casinos might not be adequate for weaker casinos to invest in attractions to hold their North Jersey customers. “Day-trippers” would have little reason to travel to Atlantic City with more convenient magnets minutes to an hour away.

Lesson number four: The heavily-advertised assertions that North Jersey casinos would “rescue” Atlantic City are based on implausible hypotheses and inaccurate citation of the facts. Neutral Wall Street analysts target at least three casinos for closure.

What Will New York Do?

Once New York State authorized casino gambling, it focused primarily on employing casinos to stimulate economic development and job creation in struggling upstate areas. Its 2015 authorizing legislation placed a seven-year moratorium on permitting casinos in New York City beyond the “racino” already operating at Aqueduct Racetrack. With six years remaining on the moratorium, New Jersey developers are hoping to gain approval in 2016 and have their full-service casinos operating in time to beat potential New York City competitors, which would take eight to 10 years to open assuming the current moratorium holds.

The New York metropolitan area is the nation’s most tempting market. The success of racinos (which offer only electronic games) in Queens and Yonkers also suggest the potential magnitude of the gambling market. In just the first five months of 2016, the two racinos contributed $277 million to education, far more than eight Atlantic City casinos generated all last year. Of course, the 50 percent tax on New York slots versus New Jersey’s 8 percent tax helps explain this imbalance.

Approval of November’s North Jersey casino question would be certain to produce a quick reaction from New York State. Here’s how the chair of the New York Assembly gambling committee put it: “I’m not interested in creating a border war with New Jersey, but New York has a vested interest in gambling and we’re not going to allow one of our neighbors to take away from that.”[27] This statement is no guarantee that New York would take rapid action to end the New York City moratorium, but it is enough of a warning to dilute the claims of North Jersey casino developers that casinos in Manhattan or the inner boroughs “will never happen.”[28]

In June, both chambers of the New York Legislature passed resolutions recognizing the threat of the New Jersey casino referendum to New York’s budding gambling industry and agreed to take quick action should New Jersey voters approve it.[29]

Lesson number five: The chances are excellent that New York would move quickly to authorize full casinos in New York City should the November 8 referendum be approved.

Endnotes

[1] New Jersey Casino Control Act–Introduction and General Provisions, vol. N.J.S.A. 5:12–1 through 5:12-49, n.d.

[2] New Jersey Casino Control Act–Introduction and General Provisions, vol. N.J.S.A. 5:12–1 through 5:12-49, n.d.

[3] New York Times, It’s ‘Place Your Bets’ as East’s First Casino Opens, May 1978. http://query.nytimes.com/gst/abstract.html?res=9503E7DE1030E632A25754C2A9639C946990D6CF

[4] A provision in the Casino Control Act that placed a minimum number of room criterion on casinos, making Resorts the only hotel that was eligible for a casino license at the time.

[5] UNLV Center for Gaming Research, Atlantic City Casino Statistics. http://gaming.unlv.edu/abstract/ac_main.html

[6] Casino Connection AC, 30 Years of Gaming, May 2008. http://www.casinoconnectionac.com/articles/30_Years_of_Gaming

[7] CCA, 5:12-83.

[8] Government Accountability Office, Impact of Gambling: Economic Effects More Measurable than Social Effects, 2000, p. 21. http://www.gao.gov/assets/230/229051.pdf

[9] CCA 5:12-144 b through e.

[10] Cathy H. Hsu, ed., Legalized Casino Gaming in the United States: The Economic and Social Impact (New York and London and Oxford: The Haworth Hospitality Press, 1999); Harriet Newburger, Anita Sands, and John Wackes, ATLANTIC CITY: PAST AS PROLOGUE A Special Report by the Community Affairs Department.

[11] New Jersey Casino Reinvestment Development Authority, History of CRDA. http://www.njcrda.com/about-us/history/

[12] Legislation pertaining to the CRDA is found in Article 12 of the CCA.

[13] Casino Control Act–Casino Reinvestment http://www.state.nj.us/casinos/actreg/act/

[14] New Jersey Division of Gaming Enforcement, Atlantic City Gaming Industry Casino Revenue Fund Taxes and Fees Source Report, November 2015. http://www.nj.gov/lps/ge/docs/Financials/CRFTF/CRFTFSourceReport.pdf

[15] UNLV Center for Gaming Research, Atlantic City Casino Statistics: Casino Revenue. http://gaming.unlv.edu/abstract/ac_main.html

[16] Repetti and SoYeon Jung, “Cross-Border Competition and the Recession Effect on Atlantic City’s Gaming Volumes,” UNLV Gaming Research & Review Journal 18, no. 2 (July 2014): 23–38“Interactive Map: Where Is the Casino Reinvestment Development Authority Spending Its Money? | The Asbury Park Press NJ | App.com,” accessed April 25, 2015, http://archive.app.com/interactive/article/20130611/SPECIAL17/306110001/Interactive-Map-Where-Casino-Reinvestment-Development-Authority-spending-its-money-

[17] UNLV Center for Gaming Research, Pennsylvania Gaming Summary. http://gaming.unlv.edu/abstract/pa_main.html

[18] Wikipedia, Pennsylvania Gaming Control Board. https://en.wikipedia.org/wiki/Pennsylvania_Gaming_Control_Board

[19] American Gaming Association, 2014 State of the States. http://www.gettoknowgaming.org/by-the-book

[20] American Gaming Association, 2012 State of the States.https://www.americangaming.org/sites/default/files/research_files/aga_sos_2012_web.pdf

[21] See ACR 206 filed September 19, 2016.

[22] Alan Mallach, Economic and Social Impact of Introducing Casino Gambling: A Review and Assessment of the Literature (Federal Reserve Bank of Philadelphia, March 2010), 18.

[23] The Jersey Journal, Developer touts casino plan as ‘windfall’ for Jersey City, September 2016. http://www.nj.com/hudson/index.ssf/2016/09/paul_fireman_touts_jersey_city_casino_plan.html

[24] NJBIZ, Lesniak: Gaming in North Jersey Will Save Atlantic City, December 2014. http://www.njbiz.com/article/20141215/INDINSIGHTS/141219869/Lesniak:-Gaming-in-North-Jersey-will-save-Atlantic-City.

[25] Jeff Gural, interview on and letter to ACprimetime, September 13, 2016. http://acprimetime.com/gurals-bullish-atlantic-city-north-jersey-casinos-get-voter-ok/

[26] Online Poker Report, Resorts And Online Partner PokerStars Disagree With Fitch Ratings’ Assessment Of North Jersey Casino Risk, June 2016. http://www.onlinepokerreport.com/21003/resorts-pokerstars-refute-fitch-ratings-new-jersey-casino-claims/

[27]Casino.org, New Jersey Casino Expansion? Not So Fast, Say New York Lawmakers, June 2016. https://www.casino.org/news/new-jersey-casino-expansion-not-so-fast-say-new-york-lawmakers

[28] op cit. ACprimetime interview

[29] See New York Senate resolution K1604 https://www.nysenate.gov/legislation/resolutions/2015/k1604 and New York Assembly resolution K01604 http://nyassembly.gov/leg/?default_fld=&leg_video=&bn=K01604&term=2015&Summary=Y&Text=Y, June 2016.