Earlier today, the Task Force on EDA Tax Incentives released its final report on New Jersey’s scandal-plagued corporate tax subsidy programs. The report found that New Jersey awarded over $500 million in tax breaks to companies that did not deserve them. In response to the report, New Jersey Policy Perspective (NJPP) releases the following statement.

Sheila Reynertson, Senior Policy Analyst, NJPP:

“This report provides further evidence that New Jersey’s experiment with corporate tax breaks was a costly failure that provided little return on investment for taxpayers. Fortunately, the state’s bloated, scandal-ridden corporate tax subsidy programs expired over a year ago without a replacement, and the state is better off as a result.

“There is no good reason for New Jersey to offer limitless tax incentives to large and already successful corporations. It’s a glass half empty view of New Jersey’s economic potential that ironically robs the state of resources needed to promote a robust and healthy business climate. To remain a viable option for companies to relocate to and expand in, New Jersey should instead focus on the building blocks of a strong economy, like strong public schools that maintain an educated workforce and reliable transit infrastructure so workers can get to their jobs on time.

“With a state budget ravaged by the fallout of a global pandemic, lawmakers must stop awarding billions of dollars in corporate tax subsidies; it is not a wise use of public resources. Mounting research finds that tax subsidies for corporations are a subpar investment when compared to other state policies and investments that are proven to help grow an economy.

“Putting people first by investing in the development of lifelong skills through things like subsidized child care and community college grants has a better return on investment and more positive impact on the state economy than do shovel-ready photo ops that allow politicians to falsely claim they helped create jobs by luring businesses to the state.

Earlier today, the New Jersey Legislature approved a three-month supplemental spending bill, which relies solely on budget cuts to close New Jersey’s revenue shortfall. In response to the spending bill, For the Many NJ releases the following statement.

Brandon McKoy, President of New Jersey Policy Perspective (NJPP) and Co-Convener of For The Many NJ:

“This budget proposal, and the process through which it was developed, is an insult to the taxpayers of New Jersey. We are in the midst of the biggest economic crisis of a generation, yet this budget does not deliver the relief New Jersey families need, nor does it meaningfully address the racial disparities that COVID-19 has laid bare. Instead, this budget relies solely on damaging cuts that will worsen the economy’s fall and further harm those struggling to make ends meet.

“Since the pandemic began, the Legislature has recognized the importance of expanding the social safety net with a flurry of new bills meant to support families who have been devastated by the pandemic. This budget does the complete opposite of that. Recent history shows that austerity does not work. New Jersey took a cuts-only approach to the Great Recession, gutting public services and programs to the bone, which dragged the state’s recovery to a crawl. Repeating this strategy means we have not learned from the mistakes of our past and will bring massive harm to workers, families, and businesses who are already in tremendous pain. The scope and impact of this crisis is tremendous, and this three-month budget fails to match it.

“Governor Murphy and legislative leaders could have avoided such drastic cuts if they had pursued new sources of revenue, starting with the reversal of Christie-era tax breaks given to ultra-wealthy families and big corporations. There is no good policy rationale to delay these reforms to the state’s tax code, and insisting on waiting for federal relief is no excuse to not do as much as we can on our own.

“The economic fallout from COVID-19 has fallen disproportionately on low-paid workers and New Jerseyans of color the most and spared the state’s wealthiest households who are disproportionately white and overwhelmingly benefit from federal tax changes signed into law by the Trump administration. To once again balance the budget on the backs of New Jersey’s working families, those living in deep poverty, and Black and Latino communities will only further exacerbate existing inequities that are rife in our society. In this historic moment of recognizing the urgency of rectifying racial equity, we can and must do better.”

For The Many is a statewide coalition of more than 30 organizations working collectively to expand funding for essential services and improve budget practices to adequately meet current and future needs, especially for communities that have been historically marginalized.

Steering committee members include: New Jersey Policy Perspective, New Jersey Working Families Alliance, New Jersey Citizen Action, New Jersey Work Environment Council, Environment New Jersey, Make the Road New Jersey, Anti-Poverty Network of New Jersey, New Jersey Education Association, Communications Workers of America – NJ, Amalgamated Transit Union – NJ, Clean Water Action – NJ.

Earlier today, the New Jersey Legislature released its three-month supplemental spending bill proposal, which relies solely on budget cuts to close New Jersey’s revenue shortfall. The last-minute proposal, released this morning and voted out of the Assembly Budget Committee this afternoon, leaves little room for public input or scrutiny. In response to the spending bill, New Jersey Policy Perspective (NJPP) releases the following statement.

Brandon McKoy, President, NJPP:

“This budget was written in secrecy with zero public hearings, zero opportunities for public comment, and little time for reporters, advocates, or even lawmakers to actually read and fully understand the bill before it was voted on. The budget document itself is unclear and begs more questions than it answers, as it fails to communicate the scale of cuts that are being made. This is a mockery of the democratic and legislative process — one we have all become far too comfortable with — and completely shut out the families harmed most by the pandemic who will now bear the brunt of budget cuts that could have been avoided. Until this deeply flawed process changes, it’s impossible to expect equitable outcomes. The people of New Jersey need and deserve better.”

New Jersey Policy Perspective (NJPP) is a nonpartisan think tank that drives policy change to advance economic, social, and racial justice through evidence-based, independent research, analysis, and advocacy.

The current pandemic has created unprecedented challenges to New Jersey’s finances, as hundreds of millions of dollars are being poured into stopping the spread of the coronavirus, saving lives, and protecting workers and communities across the state.[1] Once the immediate public health risk subsides, New Jersey will face a stark reality: the enormous costs associated with the response and the drain on incoming revenue needed to keep public services available and support struggling families and businesses. Even with federal aid and borrowing to help shore up expected revenue shortfalls, New Jersey will need to do more to address budget shortfalls in the short and stabilize the state’s finances in the long-term.

At the start of the Great Recession, New Jersey implemented a temporary income tax surcharge on earnings over $400,000 to plug budget holes and reinvest in the economy. But as the recession dragged on, the state let this policy expire and, instead, pivoted to a cuts-only approach to balancing the budget. This shift in policy slowed New Jersey’s recovery, illustrating the findings of research by economists at the Center on Budget and Policy Priorities, which found that during a recession, spending cuts are actually more harmful to a state’s economy than tax increases.[2] Facing today’s crisis, which has exposed deep-seated inequities in New Jersey’s economy, state lawmakers must avoid the mistakes of the past by avoiding damaging cuts by reforming the state’s outdated, inadequate, and unfair tax code.

A more balanced response must be taken now — one that includes increasing tax contributions from the richest five percent of earners who have repeatedly benefited from a lopsided tax system. Taken as a whole, New Jersey’s tax code has allowed the very wealthy to avoid paying their fair share towards public assets and resources.[3] These same households have also received billions of tax breaks through temporary and permanent provisions in the federal Tax Cuts and Jobs Act (TCJA) of 2017, including a reduction in the federal estate tax that only very wealthy families pay, a cut in the personal income tax rate, and a permanent cut to the corporate tax rate.

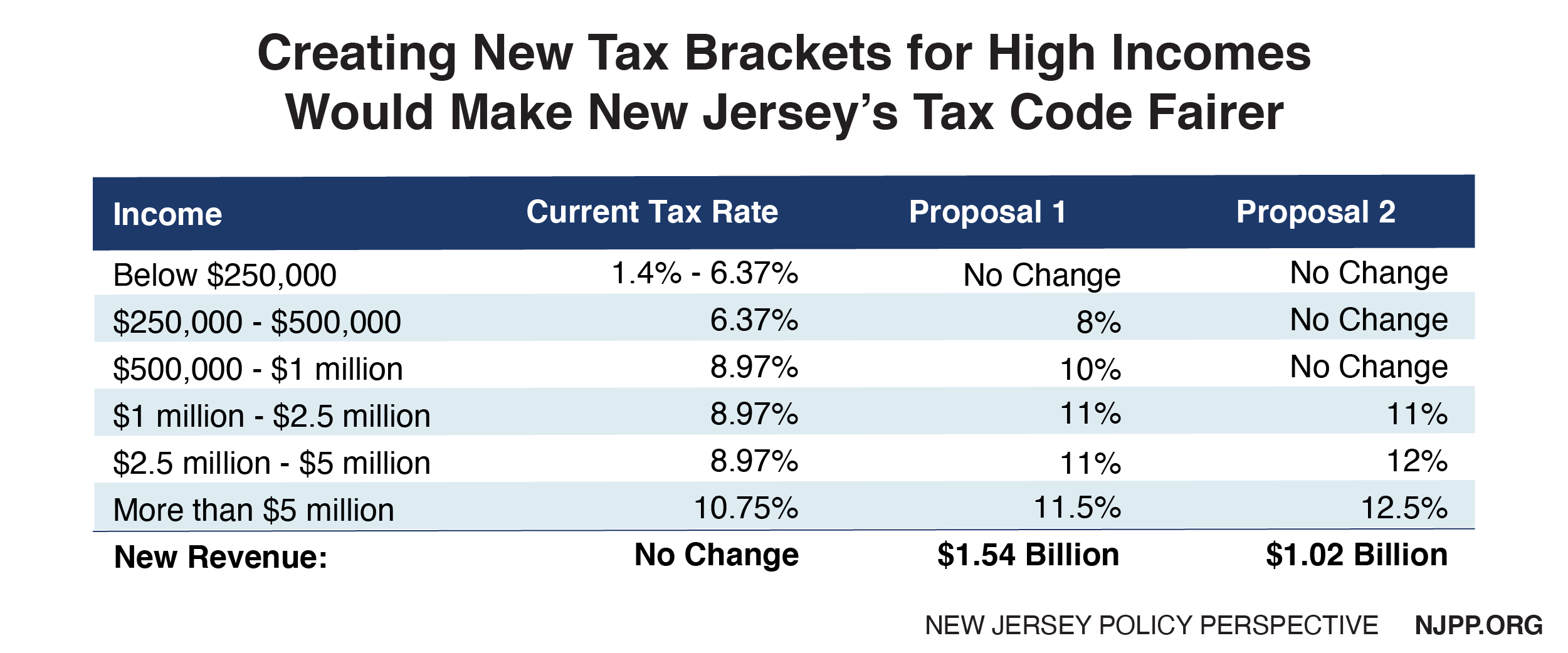

A sensible way to address revenue shortfalls and an unfair tax code is to raise income taxes on the state’s wealthiest households. By reforming New Jersey’s income tax, our recovery can be strengthened by reducing the tax burden that low-paid and middle class families pay, while generating more revenue for public programs and services that benefit all residents. Overall, increasing and adding additional tax rates on the wealthiest households would raise approximately $1.5 billion in new revenue each year while making the overall tax code fairer.[4]

A more progressive tax code can be accomplished through targeted changes on the very top tax brackets.[5] Below are two options for improvement: Proposal 1 would create new brackets at $250,000 and $1 million, and would increase the tax rate slightly at the existing $500,000 and $5 million brackets. This would ensure that the tax increase would be paid mostly by New Jersey’s ultra-wealthy, with the top 1 percent of households — with average annual incomes of $2.46 million — paying 70 percent of the total tax increase.[6]

Alternatively, the tax changes could focus solely on those who earn more than $1 million per year who live and work in New Jersey. Proposal 2 creates two new brackets at $1 million and $2.5 million, paired with a slight increase on the existing tax rate at $5 million. However, this would raise approximately $520 million less revenue than Proposal 1.

Given these findings, Proposal 1 is unequivocally the more equitable and progressive option, and should receive support from lawmakers and advocates who seek to move New Jersey’s tax code towards a more reliable and sustainable design. While Proposal 2 requires those who earn $1 million and above to contribute their fair share, choosing to exclusively focus on millionaires is a narrow and reductive view of income inequality in the Garden State. Adjusting the income tax code to modestly raise rates on those earning $250,000 and more is both a common-sense step and one which more fully addresses the disproportionate share of wealth that is held by these households. Critically, Proposal 1 also raises approximately $520 million more than Proposal 2, which would provide greater flexibility to invest in critical assets and services that can further address racial inequities rife throughout the state.

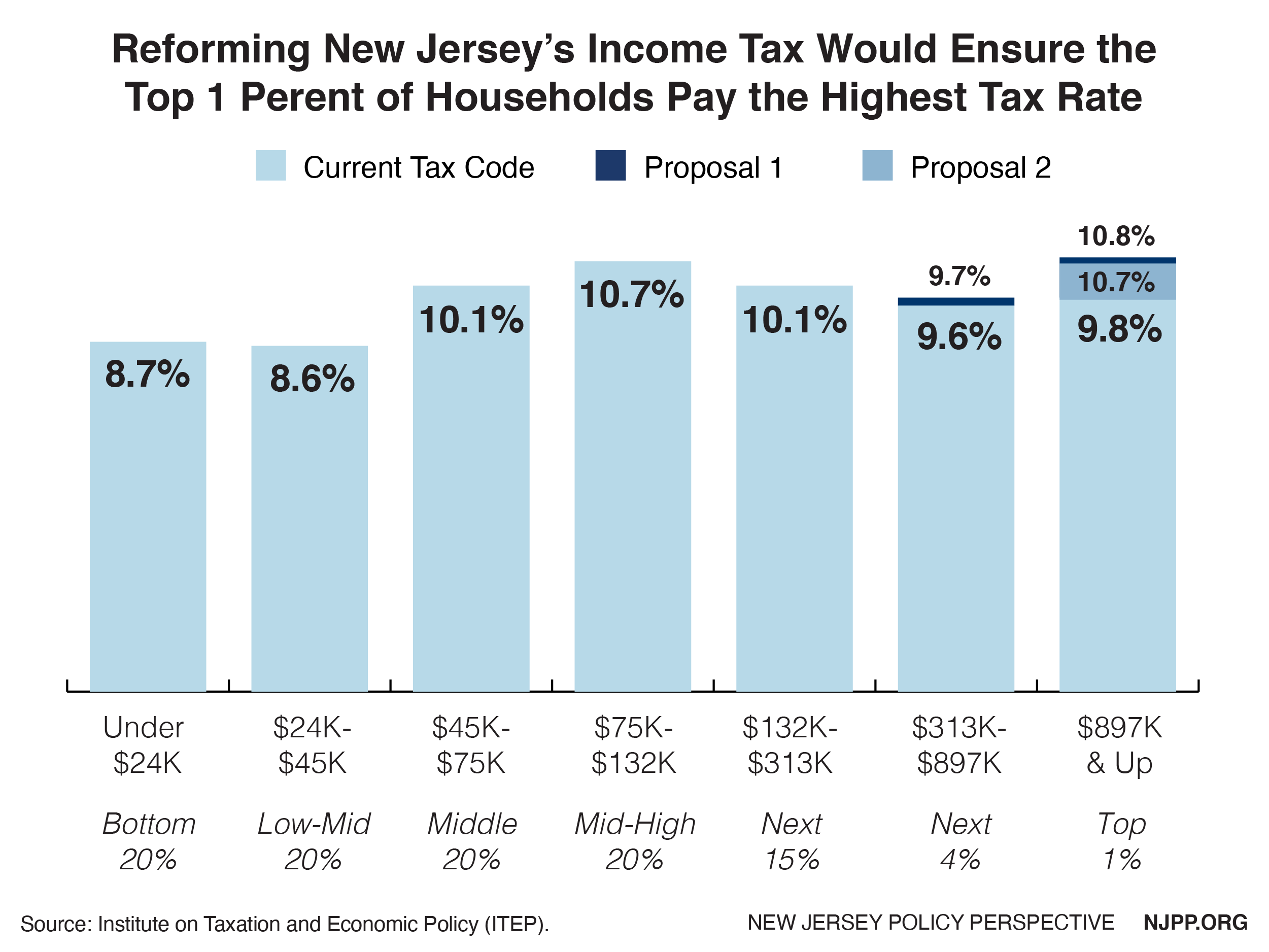

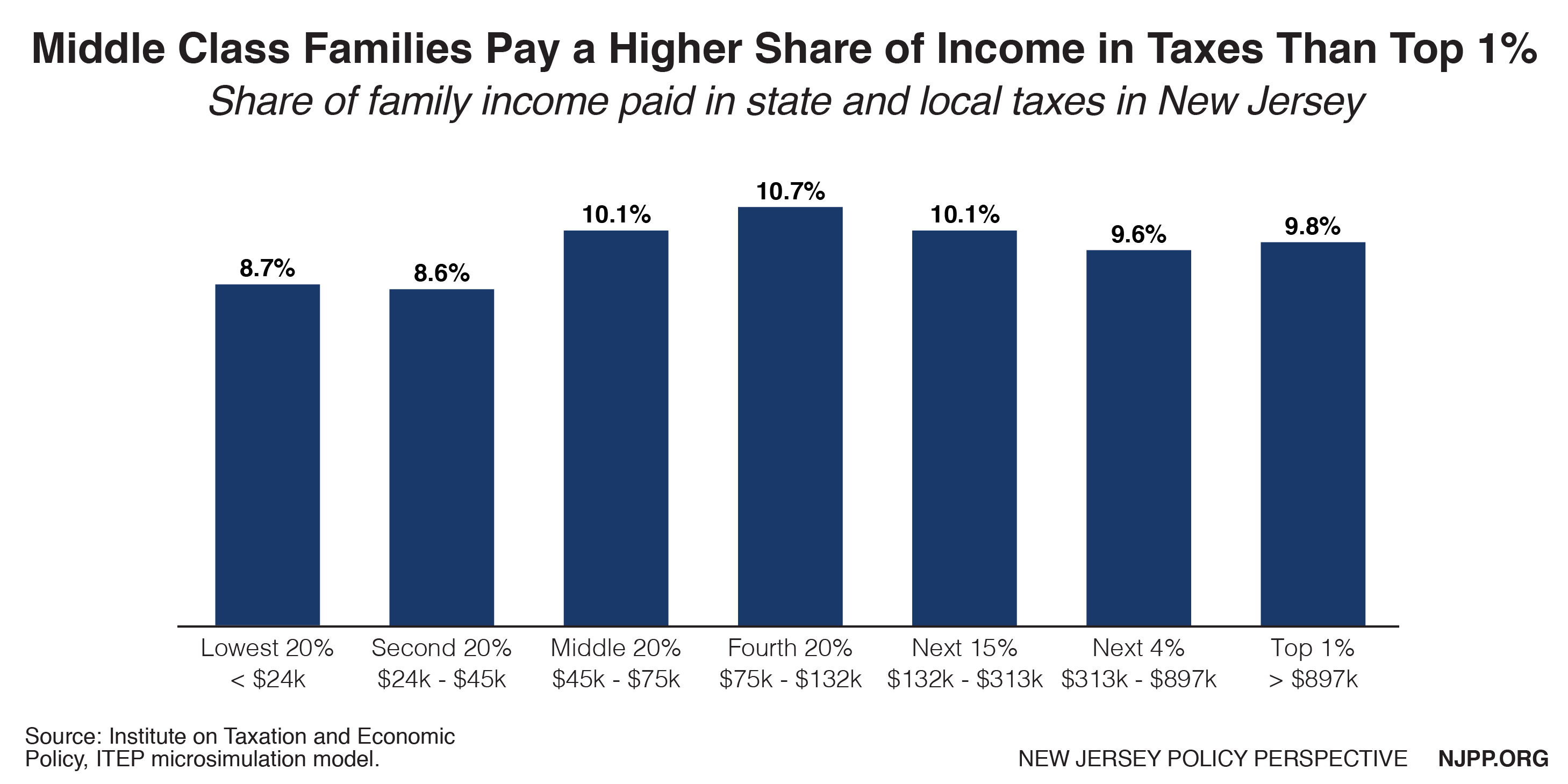

Today, middle-class New Jerseyans pay a greater share of their incomes to state and local taxes than the state’s highest earners.[7] With these proposed changes, the state income tax code would become fairer, ensuring budgets are no longer balanced on the backs of middle-class families. If Proposal 1 were adopted, the share paid by the top 1 percent would rise from 9.8 percent to 10.8 percent, a slightly higher contribution than what is paid by middle-class New Jersey families who make between $74,800 and $132,000. Proposal 2 also makes the income tax code less regressive, with the state’s top earners paying 10.7 percent of their annual income on state and local taxes, the same rate that is paid by those in the middle.

Overview and History of New Jersey’s Income Tax

New Jersey’s income tax was established in 1976 to provide better resources for schools, cities and towns, and direct property tax relief for homeowners.[8] It currently raises aproximately $16 billion in annual revenue, representing 42 percent of total state tax collections.[9] All revenue from the income tax is constitutionally dedicated to fund property tax relief, which includes school aid, teacher pensions, municipal and county aid, and direct relief for qualified veterans, people with disabilities, and senior homeowners. Despite this guaranteed revenue stream, these programs have been plagued by chronic underfunding, cuts, and delayed payments for decades. At the same time, the wealthy were given billion-dollar tax cuts and benefited from tax loopholes, lowering their overall tax responsibilities. These changes combined have created a tax code that is skewed toward the wealthy, which translates to painful cuts to public programs and services that New Jersey families, schools, and communities rely on.

Today, for single tax filers, New Jersey’s income tax ranges from 1.4 percent on incomes up to $20,000 to 10.75 percent on incomes over $5,000,000. For couples filing jointly, the tax is slightly more graduated, with lower rates in the mid-range brackets.[10]

New Jersey employs marginal tax rates, which apply different tax rates to different levels of income. As income rises, it is taxed at incrementally higher rates as opposed to a flat rate, which taxes at the same rate across all income levels. In other words, a New Jerseyan with $5,005,000 in earnings pays the top rate of 10.75 percent on only $5,000 of her earnings, not on the entire $5,005,000.

Currently, there are more tax brackets — four — under $75,000 than there are over it: three. The way New Jersey’s income tax code is designed means that $80,000 in annual earnings has the same income tax rate as $450,000. Similarly, $600,000 in earnings has the same rate as $4.9 million. New Jersey’s income tax code would benefit from a more stratified approach to higher levels of income by adding more brackets between $250,000 and $5 million.

New Jersey’s Income Tax Code: Outdated, Inadequate, and Unfair

New Jersey’s current income tax structure doesn’t accurately reflect the staggering level of income inequality that has taken root over the past 40 years. The share of all income held by the top 1 percent has steadily climbed since the Reagan administration and now approaches historical highs.[11] According to the latest data from the U.S. Census Bureau, New Jersey is the ninth most unequal state when it comes to income inequality, up from twelfth place in 2016.[12] The wealthiest households earn, on average, 37.9 times more than the middle 20 percent, according to 2019 data.[13]

While New Jersey has taken steps toward making the income tax code fairer in the past, it has failed to accurately reflect growing disparities in income:

In 2004, a new top rate of 8.97 percent on income over $500,000 was added.

In 2009, a temporary surcharge lowered the threshold for the 8.97 percent rate on income above $400,000 and added new tax rates of 10.25 percent above $500,000 and 10.75 percent above $1 million. This surcharge and new tax bracket expired in 2010.

In 2019, a new top rate of 10.75 percent on income over $5,000,000 was added.

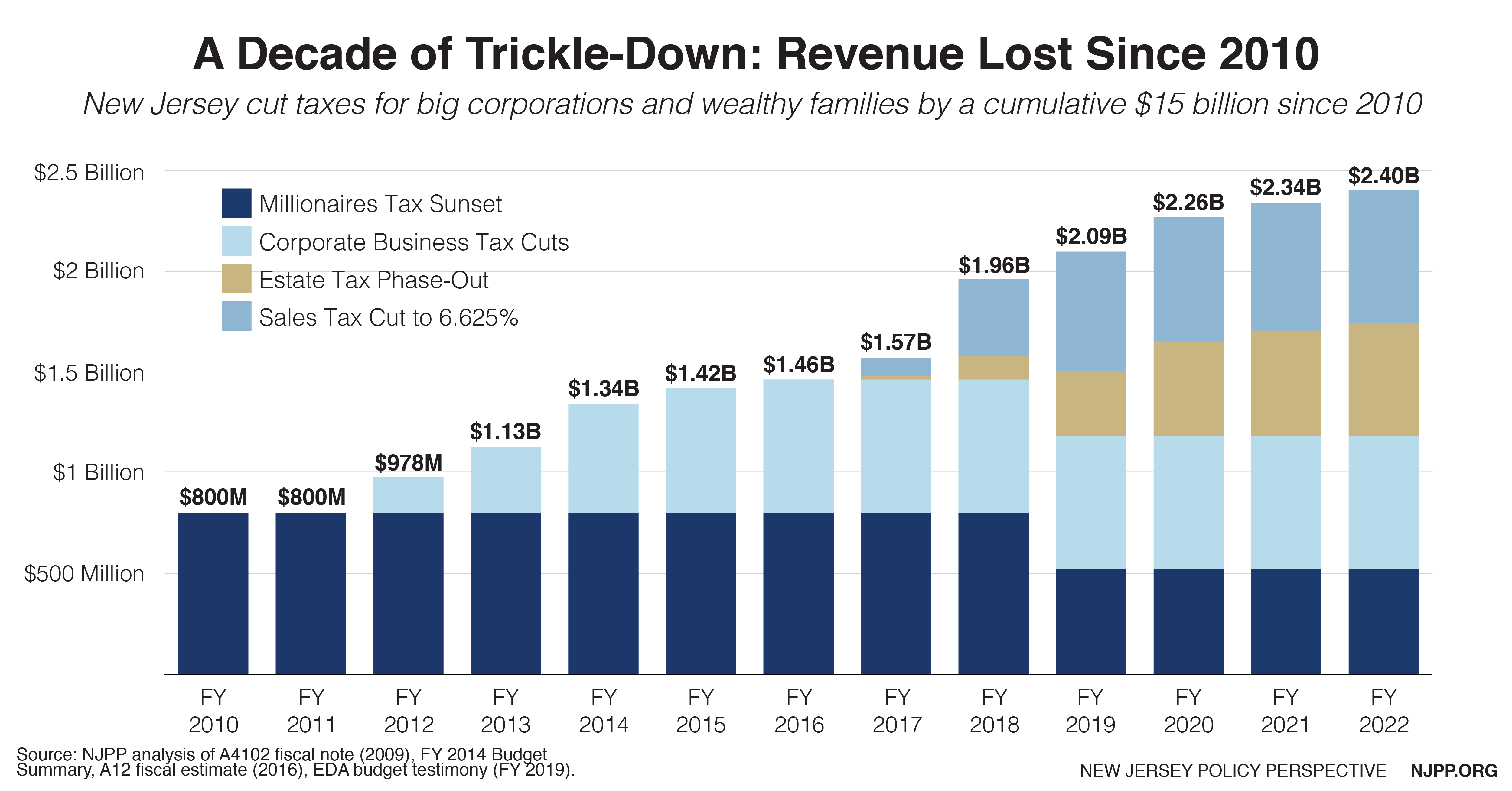

The temporary changes to income tax brackets over the $400,000 threshold raised approximately $560 million at a time when New Jersey was experiencing an enormous budget shortfall due to the Great Recession. However, the legislature allowed them to sunset a year later in 2010.[14] Subsequent efforts to reinstate these new brackets, or to otherwise make the tax code more progressive, were repeatedly vetoed by then-Governor Christie. This inaction has allowed high-earning New Jersey families to enjoy over $7 billion in cumulative tax breaks between fiscal years 2010 and 2018.[15] A permanent “mega-millionaire” tax bracket on earnings over $5 million at 10.75 percent was finally added in 2019, raising an average of $363 million a year, but this left about $400 million a year in the pockets of 18,200 New Jersey resident taxpayers and 12,800 non-residents who work in the Garden State who earn between $1 million and $5 million in annual income.[16]

Advancing Racial Equity Through Income Tax Reform

Improving New Jersey’s tax code would also address worsening racial disparities laid bare by the COVID-19 pandemic. A long history of discrimination in housing, education, employment, and the criminal justice system are all rooted in the legacy of slavery. These policies were created, and continue, to perpetuate economic advantages for white families in the Garden State. The result is a landscape of undisturbed structural racism, occupational segregation, exclusionary residential laws and practices, and massive income and wealth disparities between white households and Black and Latinx households. The typical white family in the United States has 10 times the wealth of the typical Black family and seven times the wealth of the typical Latinx family.[17] In New Jersey, the typical white family has over 52 times the wealth of the typical Black family and over 44 times the wealth of the typical Latinx family.[18] This stark and long-lasting gap means some families can respond to unexpected emergencies like a pandemic without significant hardship while others are left vulnerable and at greater risk of housing insecurity and job loss.

One of the most powerful tools driving income and wealth inequality is the tax code. Just as tax policy choices are both a symptom of, and contributor to, broader injustices, they can also be utilized to repair the damage done and advance racial equity.

For example, the 2017 federal tax law, the Tax Cuts and Jobs Act (TCJA), actually worsened racial inequities by showering the wealthy with tax benefits at the expense of the economic security among middle-class and low-income families, which in New Jersey are over-represented by Black and Latinx households. Three-quarters of Black households (75 percent) and of Latinx households (77 percent) earn less than $81,000 a year in the Garden State.[19]

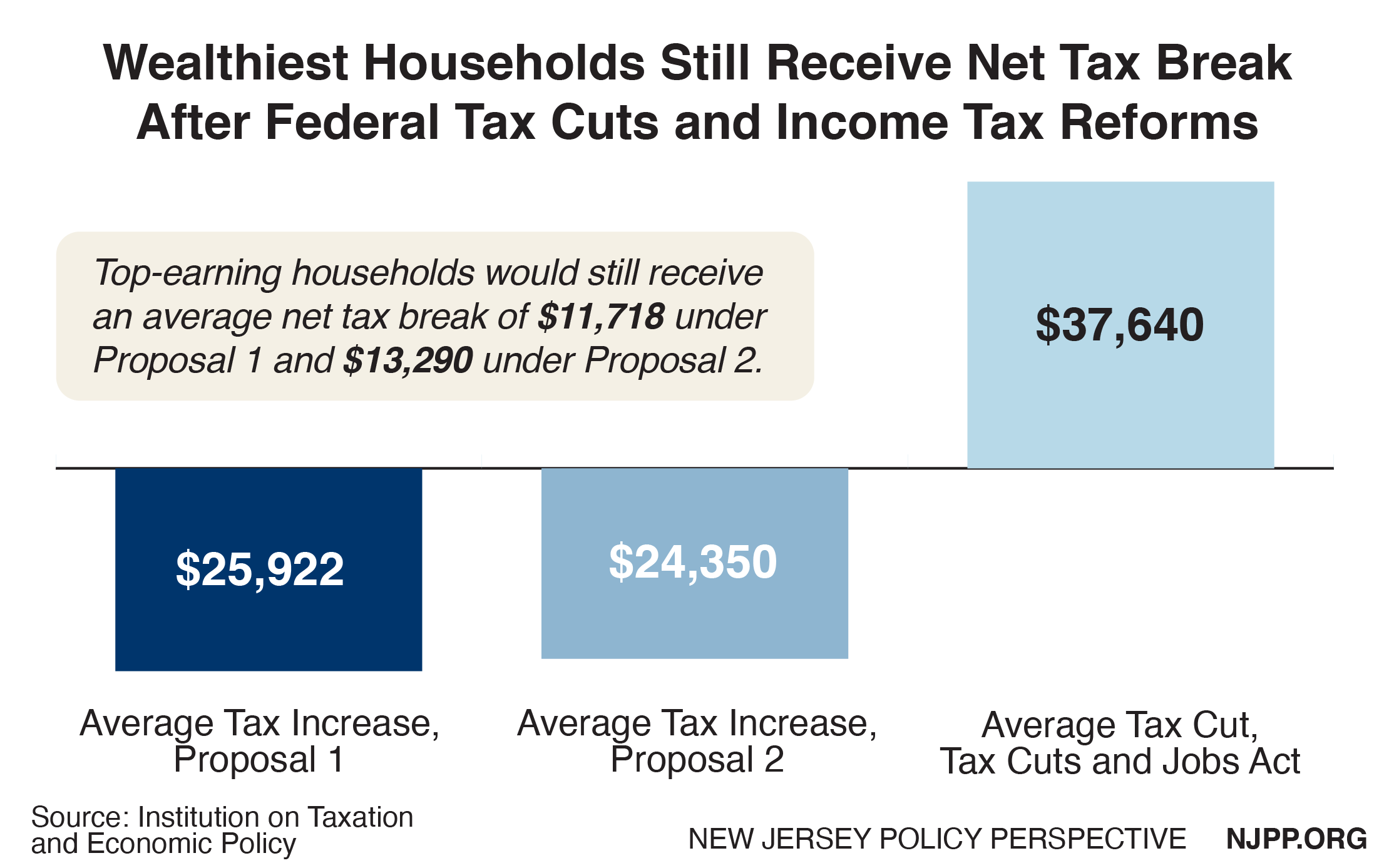

In New Jersey, the TCJA is more widely known for one provision: the temporary $10,000 cap on state and local tax (SALT) deductions, which limits how much taxpayers can deduct these taxes from their federal tax bill. But other provisions in the 2017 tax law — corporate tax cuts, pass-through tax cuts, and estate tax cuts — benefited the vast majority of the wealthiest taxpayers. That windfall means that even with the SALT deduction limitation factored in, New Jersey’s top 1 percent of earners, who are overwhelmingly white, will pocket an average of $37,640 this year.[20]

Targeted changes to New Jersey’s income tax code as proposed above could rectify this lopsided benefit, reversing course on the racial implications of the TCJA and providing the state with desperately needed resources — with the top 1 percent of earners still receiving an average net tax cut of about $12,500 when considering both the TCJA and the proposed income tax reforms.

Should the federal government repeal the SALT deduction limitation, as currently proposed by Congress in the HEROES Act, there is no reason for New Jersey to pull back on these targeted changes to the income tax code. That’s because over half (54 percent) of the benefit from a reversal of the SALT cap would go to the wealthiest 1 percent with nearly every one of those families getting a hefty tax break.[21] In fact, such a policy change all but solidifies why New Jersey must take action.

According to State Treasurer Elizabeth Maher Muoio, New Jersey is likely facing “an unprecedented fiscal crisis” with potential shortfalls that rival the Great Recession.[22] Tough decisions lay ahead with options that may or may not be available to the Garden State, including borrowing, flexible federal aid, and revenue reserves. Raising sufficient revenue for the recovery is not just a short-term goal. It is a strategic tool to protect vital investments, overcome racial inequities, and build a state economy whose benefits are widely shared.

The COVID-19 crisis has devastated communities across New Jersey. If we really are all in this together, we must guarantee that sacrifices will be shared among all residents. For decades, low-income and middle-class families — especially families of color and marginalized communities — have borne the brunt of economic recovery while enjoying none of the rewards. These proposed changes to the income tax code are the right policies at the right time and will help ensure that all New Jerseyans are paying more of their fair share to support the investments we all need to thrive.

End Notes

[1] New Jersey Department of Treasury, Report on the Financial Condition of the State Budget for Fiscal Years 2020 and 2021, May 2020. https://www.state.nj.us/treasury/omb/publications/NJ-Financial-Condition.pdf

[2] Center on Budget and Policy Priorities, Budget Cuts or Tax Increases at the State Level: Which is Preferable When the Economy is Weak?, April 2010. https://www.cbpp.org/research/budget-cuts-or-tax-increases-at-the-state-level?fa=view&id=1032

[3] New Jersey Policy Perspective, It’s Time to Face the Music, Jersey: We’ve Been Robbed, March 2019. https://www.njpp.org/budget/its-time-to-face-the-music-jersey-weve-been-robbed

[4] These proposals use the Institute on Taxation and Economic Policy (ITEP) Microsimulation Tax Model, 2019. Revenue estimates will be affected by COVID-19 crisis. However, because these tax changes are targeted on high-income earnings, the estimates will likely be comparable.

[5] A tax bracket refers to a range of incomes subject to a certain income tax rate.

[6] Taxation and Economic Policy (ITEP) Microsimulation Tax Model, 2019.

[7] Institute on Taxation and Economic Policy, Who Pays? A Distributional Analysis of the Tax Systems in All 50 States, 6th Edition, October 2018. https://itep.org/whopays/new-jersey/

[9] State of New Jersey, The Governor’s FY 2021 Detailed Budget, March 2020. https://www.nj.gov/treasury/omb/publications/21budget/pdf/FY21GBM.pdf

[10] New Jersey Department of Treasury, Division of Taxation, NJ Income Tax – Tax Rates, Last updated February 2020. https://www.state.nj.us/treasury/taxation/taxtables.shtml

[11] Center on Budget and Policy Priorities, A Guide to Statistics on Historical Trends in Income Inequality, January 2020. https://www.cbpp.org/research/poverty-and-inequality/a-guide-to-statistics-on-historical-trends-in-income-inequality

[12] The Star Ledger, The gap between the rich and poor in New Jersey keeps increasing, data shows, March 2020. https://www.nj.com/data/2020/03/the-gap-between-the-rich-and-poor-in-new-jersey-keeps-increasing-data-shows.html

[13] Institute on Taxation and Economic Policy (ITEP) Microsimulation Tax Model. Based on all New Jersey residents, using 2019 incomes.

[14] New Jersey Department of Treasury, Division of Taxation, Important Changes for 2010, Last updated March 2020. https://www.state.nj.us/treasury/taxation/new2010.shtml

[15] New Jersey Policy Perspective, It’s Time to Face the Music, Jersey: We’ve Been Robbed, March 2019. https://www.njpp.org/budget/its-time-to-face-the-music-jersey-weve-been-robbed

[16] New Jersey Treasury, Office of Management and Budget, Citizens’ Guide to the State Budget Fiscal Year 2019, December 2018. https://www.nj.gov/treasury/omb/publications/19citizensguide/citguide.pdf

[17] Center for American Progress, The Coronavirus Pandemic and the Racial Wealth Gap, March 2020. https://www.americanprogress.org/issues/race/news/2020/03/19/481962/coronavirus-pandemic-racial-wealth-gap/

[18] New Jersey Institute for Social Justice, Reclaiming the American Dream: Expanding Financial Security and Reducing the Racial Wealth Gap Through Matched Savings Accounts, April 2019. https://www.njisj.org/new_jersey_institute_for_social_justice_releases_reclaiming_the_american_dream_expanding_financial_security_and_reducing_the_racial_wealth_gap_through_matched_savings_accounts

[19] Data shared with NJPP by Institute on Taxation and Economic Policy, May 2019.

[20] Institute on Taxation and Economic Policy, TCJA by the Numbers: 2020, August 2019. https://itep.org/tcja-2020/

[21] New Jersey Policy Perspective, A Grain of ‘SALT’: New Jersey Needs More Than Workarounds to Respond to GOP Tax Plan, January 2018. https://www.njpp.org/budget/a-grain-of-salt-new-jersey-needs-more-than-workarounds-to-respond-to-gop-tax-plan

[22] New Jersey Department of the Treasury, Treasury Issues Preliminary Update on Projected Revenue Shortfall through Fiscal Year 2021, May 2020. https://www.nj.gov/treasury/news/2020/05132020b.shtml

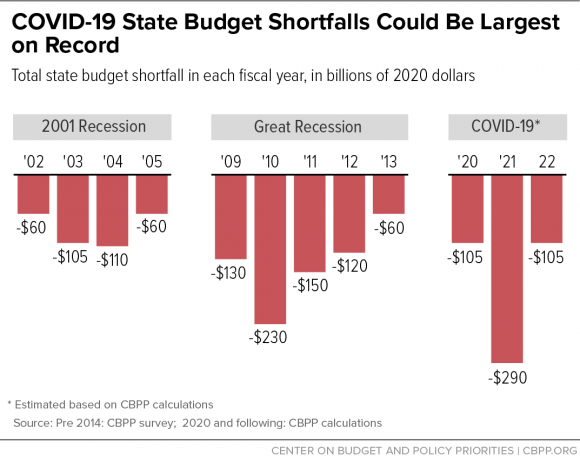

New Jersey is not alone, according to a new report by the Center on Budget and Policy Priorities (CBPP), as states across the nation are facing what could be the largest budget shortfalls ever recorded. Federal lawmakers have already provided states with some fiscal relief through the Coronavirus Aid, Relief, and Economic Security Act, or CARES Act, but states are limited in how they can use these funds. As it stands, significantly more aid will be necessary for states to address the ongoing public health emergency, provide relief to families and small businesses who need it, and avoid drastic cuts to public services that would disproportionately harm communities of color and only prolong the nation’s ultimate recovery.

CBPP estimates that state budget shortfalls could total more than $500 billion, with most of the revenue loss concentrated in the upcoming fiscal year. These are conservative estimates as they do not include the substantial new costs that states are incurring to contain the COVID-19 virus, nor do they account for revenue shortfalls at the local, territorial, or tribal levels of government. Overall, these figures far exceed the federal aid given to states thus far, as well as what states already have saved up in their rainy day funds. What’s worse for New Jersey (and many other states) is that it will quickly exhaust its Rainy Day Fund, if it hasn’t already, as lawmakers left the state’s reserves empty for a full decade before finally making a modest deposit last year. To ensure a strong recovery from COVID-19, Congress should prioritize substantial and immediate fiscal relief in its next stimulus package.

What happens if the federal government does not provide states with significantly more aid?

One unattractive option is to make enormous cuts to state spending. This would mean laying off teachers and other public employees, as well as slashing spending on state programs and services that families rely on, especially during a crisis like the one we are living through. As we saw firsthand in the wake of the Great Recession, a cuts-heavy response to a downturn worsens the economy’s fall, slows the state’s recovery, and causes long-term harm to families and communities who are already struggling to make ends meet. It’s important New Jersey learns from this experience and does not make the same mistakes of the past.

So what else is there to do?

Another option is to borrow funds to support critical needs. Normally, New Jersey would not be allowed to borrow funds to cover operating expenses, but there is an exception in the state Constitution for “purposes of war, or to repel invasion, or to suppress insurrection or to meet an emergency caused by disaster or act of God.” In response to the COVID-19 pandemic, the Federal Reserve will buy up to $500 billion in bonds from state and local governments across the country to help shore up their finances. Governor Murphy has already expressed interest in borrowing up to $9 billion from the Fed, and NJPP has come out in support of that proposal, as President Brandon McKoy said the pandemic, “justifies, if not demands,” such action. Borrowing would help New Jersey avoid damaging cuts, which would help speed the state’s recovery from the recession.

But even if the state borrows to fill budget holes, more resources and funding will be needed to pay off these bonds in the short-term and stabilize the state’s finances in the long-term; after years and years of disinvestment and austerity, this should surprise no one. State lawmakers can accomplish this by ending tax breaks passed under the previous administration for the state’s wealthiest households and biggest corporations, as well as by reforming the income tax code to ensure that the top 5 percent of earners pay their fair share. Raising new, sustainable revenue will help New Jersey recover from the current economic downturn, prepare the state for the next one, and build an economy that works for the many, not just a chosen few.

To read a PDF version of this policy brief, click here.

The COVID-19 pandemic hit New Jersey with a ferocious punch, leaving the state scrambling to contain the spread of the virus, save lives, and provide financial relief to the families and businesses who need it most. Depending on how quickly the state economy gets back on track and how much aid the federal government provides to offset New Jersey’s budget shortfall, many state programs and services are in serious danger of cuts or, worse, elimination. The economic fallout from COVID-19 is a stark reversal of the healthy state economy of the past two years that allowed New Jersey to expand investments in areas like pre-K education, free community college, transit infrastructure, the state’s reserves, and much more. Unfortunately, New Jersey’s recent deposits in its Rainy Day Fund will not be enough to weather this downturn; the state ran out of time, and now the departments tasked with running state government and responding to the COVID-19 crisis are facing an uncertain future, much like the rest of the economy.

Without proper funding, state government cannot fully serve the needs of the public, especially during a time of crisis when the demand for services is at an all-time high. Unfortunately, New Jersey lacks the reserves to help shore up these departments, as outlined in NJPP’s latest report. Making matters worse, tax revenue from income, sales, and corporate business taxes is collapsing at an unprecedented pace. Federal aid to help state budget shortfalls is essential to contain the damage, but it has yet to be considered in a serious way by Congress. If anything, the crisis has put a glaring spotlight on the damage done by a decade of government disinvestment. To ensure a strong and immediate recovery from the COVID-19 crisis, New Jersey cannot afford to repeat the mistakes of the past.

In response to the Great Recession, New Jersey lawmakers and Governor Christie made brutal cuts to state agencies and public programs, ultimately slowing the state’s recovery. Even before the COVID-19 pandemic hit, these cuts continued to hamper New Jersey’s ability to provide critical services that New Jersey families, communities, and the broader economy rely upon. Taken as a whole, staffing levels across all departments dropped by over 20 percent since the Great Recession in 2008. Today, funding for departments has yet to reach pre-recession levels and, for many, staffing is at a record-low for the past two decades.

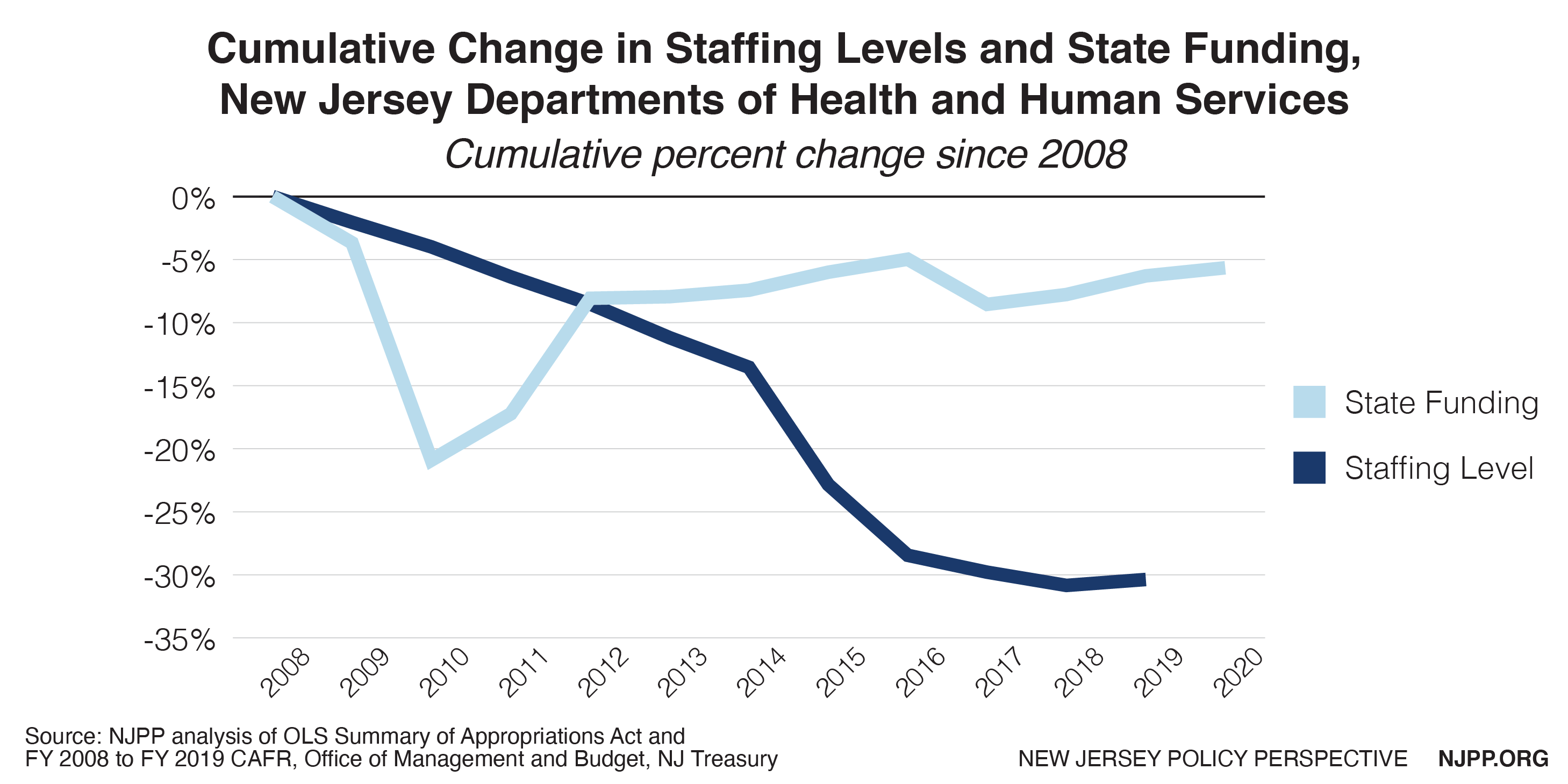

Departments of Health and Human Services

During normal times, and especially now in the middle of a global pandemic, the state departments of Health and Human Services ensure the safety and well-being of New Jersey’s most vulnerable populations, including the elderly, the disabled, those in addiction recovery, and children living in deep poverty. Taken together, the Department of Health (DOH) and the Department of Human Services (DHS) now function with less funding (6 percent) and about a third less staffing (30 percent) than they had at the onset of the Great Recession in 2008.

Without the necessary financial resources and workforce, it is near-impossible for the departments to promote public health. For example, the state is unable to ensure that community hospitals are in compliance with safety standards like adequate nursing staff levels, putting patients and their communities at risk. The lack of adequate resources and proper oversight has also plagued DOH’s medical examiner system, which The Star-Ledger described as a “national disgrace” in their 2017 Death and Dysfunction report. Despite a larger workload in recent years due to the overdose epidemic, the state medical examiner offices have 20 percent fewer employees than 10 years ago. Similarly, local health departments — the frontline of the state’s COVID-19 response — have been underfunded for decades, leaving them ill-equipped to handle the workload in response to the viral outbreak. Compared to other states, New Jersey fell to the bottom quarter for spending per person on local health departments at less than $30 per person. For reference, states like New York and Maryland invest at least $70 per person in local health departments.

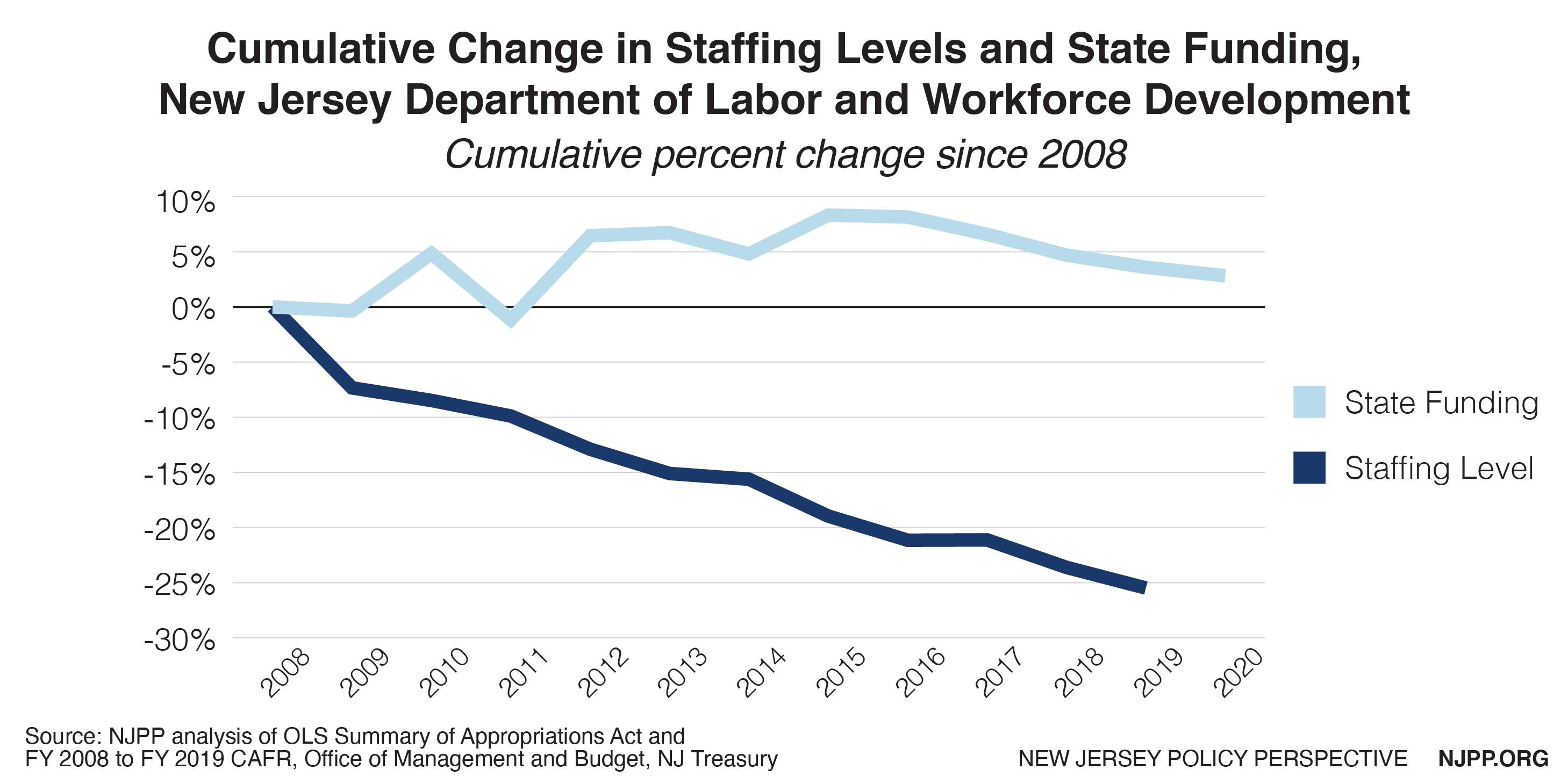

Department of Labor and Workforce Development

Once shelter in place became the new norm, much of New Jersey’s economy ground to a halt, with record numbers of residents losing their jobs and closing their businesses. Since the COVID-19 pandemic hit, more than 718,000 New Jersey workers — representing more than 15 percent of the state’s workforce — have filed for unemployment benefits to make ends meet.

However, many of these workers are unable to file their claims, as the department lacks the necessary staff and resources to handle all of the applications. Inadequate staffing and out-of-date software have paralyzed the department to the point where Governor Murphy has called on retired employees to return to work and help with the backlog. While the state Department of Labor and Workforce Development’s funding has remained stable since the Great Recession, it is operating with far fewer employees now than it did over a decade ago; since 2008, the department has experienced a 25 percent cut in staffing levels. This significant drop flew largely under the radar until now as residents go weeks without receiving their unemployment benefits.

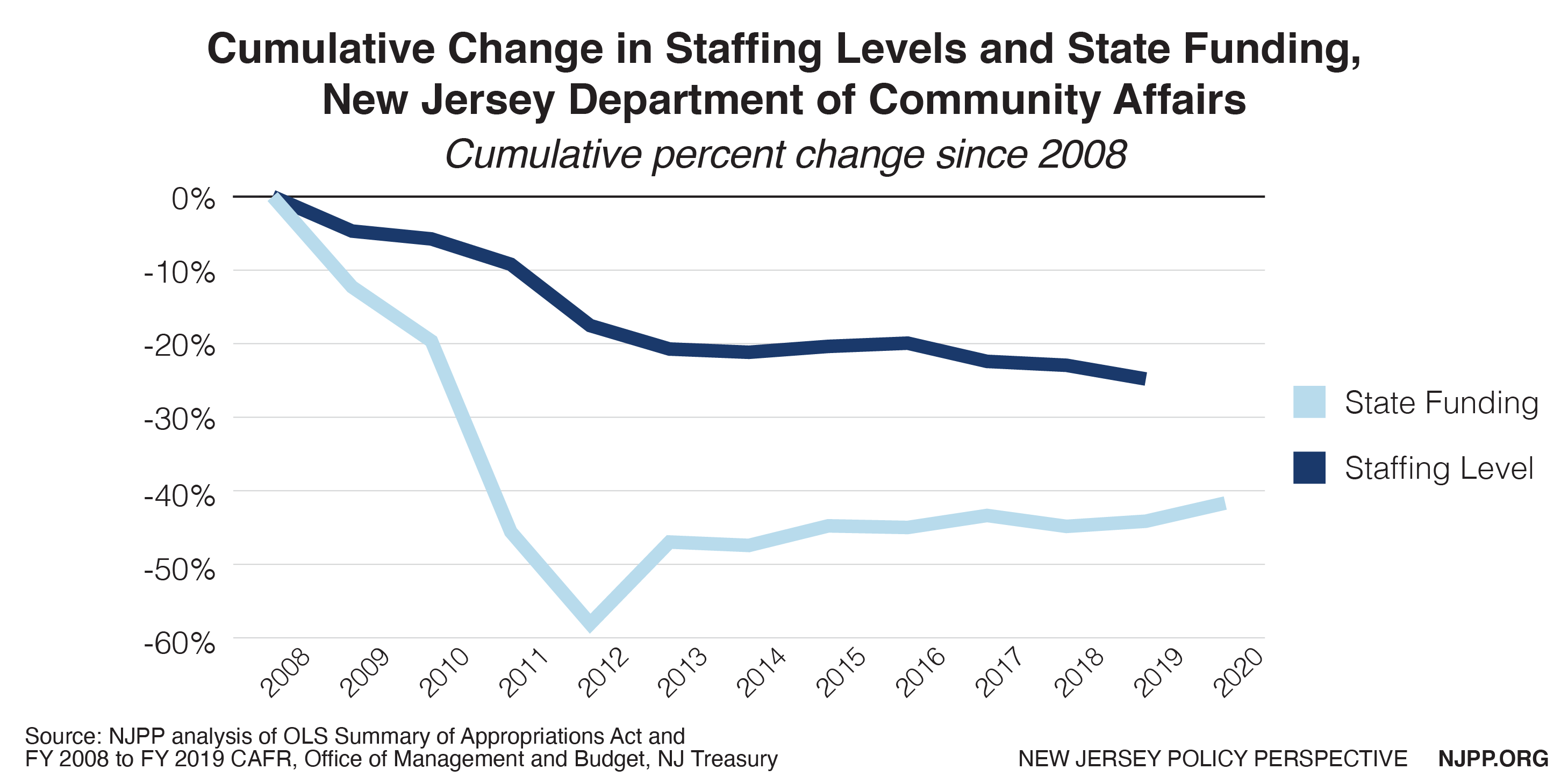

Department of Community Affairs

Far too many jobs in our economy do not pay enough or provide enough hours for families to meet their basic needs. As a result, thousands of New Jersey families struggle to afford necessities and rely on state assistance to help pay for their utilities and rent. The demand for these services was acute before the COVID-19 pandemic and even more so now as residents lose their jobs and struggle to pay their bills. But an inflation-adjusted 42 percent drop in funding since just before the Great Recession means less resources for the Department of Community Affairs to do its job and help those hit hardest by this crisis.

By providing low-income households much-needed energy assistance or affordable housing opportunities now, the state could play a vital role in helping the state economy recover more quickly — but only if it has adequate funding to do so. Even the Treasury Department has had to make do with almost half the funding it used to receive, undermining its ability to develop and enforce the tax laws that secure financial resources for all of these departments.

When in a Hole, Stop Digging it Deeper

When state government finds itself in a hole, as it does now in the COVID-19 crisis, cuts will only dig the hole deeper. Scaling back essential government services should not be an option, as the safety net programs administered by New Jersey’s departments and agencies will act as the foundation for the state’s ultimate recovery. To fund these investments and prevent cuts that would be devastating to families in every corner of the state, New Jersey must find new revenue as part of its response to COVID-19 and the resulting economic fallout. We suggest starting with targeted changes to the tax code, like making the income tax more progressive and extending the corporate business tax surcharge, to help fund New Jersey’s recovery.

Methodology

State funding figures are from the New Jersey Office of Legislative Services Summary of Appropriations Act and are inflation-adjusted to 2020 U.S. Dollars. Staffing level figures are for full-time employees, according to the New Jersey Department of the Treasury, Office of Management and Budget, Comprehensive Annual Financial Report (CAFR) for FY 2008 to FY 2019, and the Governor’s Budget Message for FY 2009 and FY 2021 . The staffing levels represent total staffing, including positions funded by the state and federal government. State funding and staffing level figures are combined for the Department of Health and Department of Human Services to account for offices and responsibilities that have been transferred from one department to the other over the time period reviewed in this analysis.

Departments of Health and Human Services

In FY 2008, combined state funding for the Department of Health and the Department of Human Services was $8.1 billion; in FY 2020, state funding was $7.6 billion. In FY 2008, total full-time staffing was 17,634; in FY 2019, total full-time staffing was 12,279. In FY 2008, 66 percent of full-time staff were funded by the state and 34 percent were funded by the federal government. In FY 2019, 32 percent of full-time staff were funded by the state and 68 percent were funded by the federal government.

Department of Labor

In FY 2008, state funding for the Department of Labor was $167 million; in FY 2020, state funding was $172 million. In FY 2008, total full-time staffing was 3,418; in FY 2019, total full-time staffing was 2,547. In FY 2008, 6 percent of full-time staff were funded by the state and 94 percent were funded by the federal government. In FY 2019, 6 percent of full-time staff were funded by the state and 94 percent were funded by the federal government.

Department of Community Affairs

In FY 2008, state funding for the Department of Community Affairs was $1.6 billion; in FY 2020, state funding was $923 million. In FY 2008, total full-time staffing was 1,129; in FY 2019, total full-time staffing was 849. In FY 2008, 15 percent of full-time staff were funded by the state and 85 percent were funded by the federal government. In FY 2019, 10 percent of full-time staff were funded by the state and 90 percent were funded by the federal government.

On Thursday, Governor Murphy announced that the state could borrow as much as $9 billion from the U.S. Federal Reserve to fill budget holes brought on by COVID-19. In response to this announcement, New Jersey Policy Perspective (NJPP) releases the following statement.

Brandon McKoy, President, NJPP:

“The ongoing health and economic emergency New Jersey faces from the COVID-19 pandemic justifies, if not demands, the borrowing proposed by Governor Murphy.

“New Jersey faces unprecedented challenges that endanger the economic security of families and small businesses, and stretch thin the financial resources our state relies on to help those in need. Without significantly more aid from the federal government, we are forced to choose between devastating cuts to public services that families need and borrowing billions of dollars to enable state government to meet its growing responsibilities to its residents.

“Borrowing, especially at the levels that would be required in this crisis, should always be viewed with skepticism, especially because New Jersey in the past has too often justified massive borrowing to support tax cuts that reduced the state’s ability to invest in the building blocks of economic growth. This situation is different. Borrowing now will speed our recovery out of this recession. This will require a disciplined approach that includes reforming the state tax code to make it fairer by calling upon the wealthiest to pay their fair share toward repaying, on schedule, what the state borrows.

“Policy decisions made in the next few weeks will set the path for New Jersey’s recovery. The worst thing the state could do when it’s in a hole like this is to keep digging. As we learned after the Great Recession, a response centered on cutting services and reducing investments in public needs will only slow New Jersey’s economic recovery, prolong the suffering of those harmed most by the pandemic, and worsen existing racial and economic inequality. Borrowing funds to plug budget holes, while far from ideal, is the best way for lawmakers to avoid harmful cuts in the short-term and maintain a strong social safety net for residents losing their jobs and businesses.”

To read a PDF version of the full report, click here.

Crafting a state budget is a tricky task in the best of times as lawmakers juggle competing needs while attempting to predict future economic conditions. This year, however, the COVID-19 pandemic has turned the fairly straightforward FY 2021 budget season into one that will force lawmakers to address sudden and dramatic changes in New Jersey’s finances and the state’s broader economy.

New Jersey is facing a dual threat from the COVID-19 pandemic: a public health crisis that requires mandatory business closures and social distancing, along with the economic fallout from these necessary measures. The state is taking in dramatically less revenue in income, sales, and corporate business taxes, stretching its finances thin. At the same time, lawmakers are hoping to ramp up spending to curb the spread of COVID-19 and provide relief for workers and families struggling to make ends meet. The Murphy administration has already frozen $920 million in planned expenditures in anticipation of a significant drop in revenue collections.[1] New Jersey’s Rainy Day Fund, which is meant to offset the impact of unexpected emergencies, is not sufficient to meet the state’s pressing needs in the coming days and months. Progressive sources of revenue will be needed to ensure the state has the resources to meet our rapidly growing public health and economic needs.

Under the first two years of the Murphy administration, New Jersey has moved away from trickle-down strategies and toward progressive tax structures that enable sufficient investment in public services and assets. Unfortunately, these policies have not been in place long enough to undo decades of underinvestment, nor has there been enough progress to blunt the impact of COVID-19 on the state’s economy. By implementing new, reliable sources of revenue, state lawmakers can avoid harmful cuts to vital services, protect New Jersey families harmed during this economic downturn, and build an economy that works for the many.

New Jersey’s Revenue Problem

New Jersey has a revenue problem. In fact, the state has failed to bring in enough revenue to cover annual expenses since at least 2002. Looking at the latest available data, New Jersey has the worst fiscal deficit in the nation at 91.1 percent.[2]

This lack of revenue has resulted in flat funding and cuts to department budgets, the raiding of trust funds and emergency savings to make ends meet, and forgoing investments into our Rainy Day Fund. For instance, over $300 million in dedicated funds meant for the Affordable Housing Trust Fund were diverted over the course of the last decade to cover chronic budget shortfalls, severely hampering the state’s ability to construct affordable homes and address its continuing housing and foreclosure crisis. Similarly, the New Jersey Department of Environmental Protection has a limited capacity to hold big polluters accountable and enforce clean air, water, and waste standards as its funding was cut 35 percent since the Great Recession.[3] All in all, these fiscal decisions have not only limited the ability of state government to do its job, but have also led to an unenviable record of 11 credit downgrades by the major credit rating agencies since 2010, making borrowing for capital improvement projects more expensive.[4]

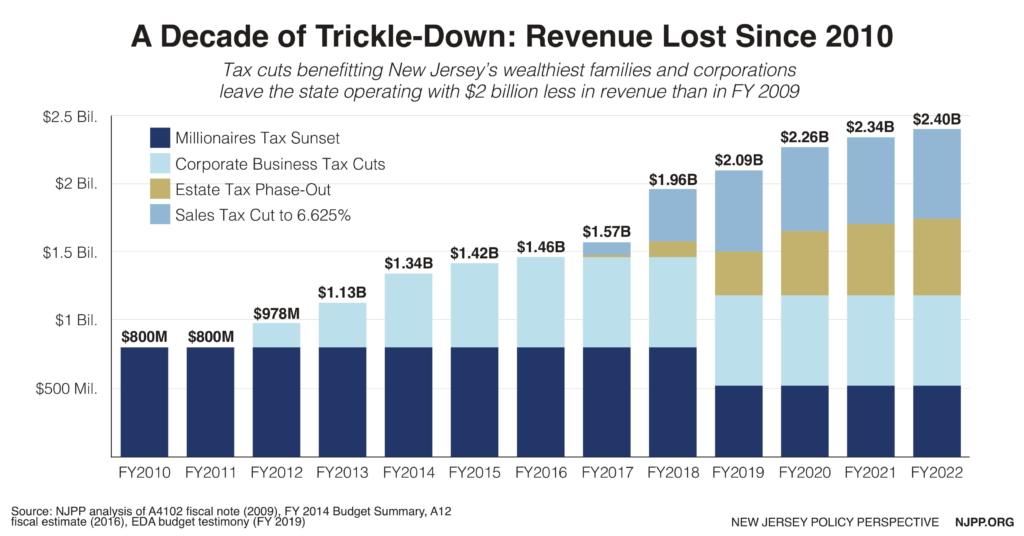

To make matters worse, the Garden State has turned its back on working families by relying on trickle-down economic policies, namely lopsided tax cuts for the ultra-wealthy and large corporations and deeply flawed economic development strategies that put a tremendous burden on the state budget for years to come. Under the Christie administration, New Jersey cut taxes and reduced revenue by a cumulative $15 billion while awarding over $8 billion in tax subsidies to already wealthy corporations.

The state’s failed experiment with trickle-down economics started in 2010 when the millionaires’ tax was allowed to sunset, giving wealthy families a cumulative $5 billion in tax breaks and undermining property tax relief programs that allow low-income seniors and adults with disabilities to remain in their homes. In 2018, the estate tax was fully repealed, which was only paid by the wealthiest 4 percent of households in the state. Since the repeal of this tax, wealthy heirs have collectively benefited to the tune of $923 million at the expense of middle-class families. What’s more, in 2017 the state began gradually reducing the sales tax from 7 percent to 6.625 percent. This small decrease in the sales tax has cost New Jersey $1.7 billion in lost revenue, making it even more difficult for the state to fund key priorities, build a healthy Rainy Day Fund, and meet its existing obligations.

These cuts also have deepened structural inequality in the very communities that have been historically deprived of meaningful investments. Already, 25 percent of New Jersey families don’t have enough savings to withstand an emergency without falling into poverty, despite the state’s ranking as one of the wealthiest in the nation.[5] It’s disproportionately worse for New Jersey’s Black households at 45 percent and Hispanic/Latinx households at 60 percent. For these families, a layoff or a visit to the emergency room can easily translate into a financial crisis.

What’s worse, everyday New Jersey families now pay a higher percent of their income in state and local taxes than the state’s wealthiest households do. Middle-income earners — those who make $74,800 to $132,000 annually — pay the highest effective tax rate. They also pay the highest percentage of their annual income in property taxes, at an average of 5.8 percent. Those in the top one percent pay a much smaller share of their income in property taxes at an average of 2.2 percent. The state tax code also disproportionately harms households of color, who are more likely to earn less (due in large part to the nation’s legacy of slavery and generations of discriminatory state and federal policies), and thus pay a larger share of their incomes in state and local taxes than white households.

Breaking Bad Habits: Governor Murphy’s First Two Budgets

The first two budgets enacted under Governor Murphy’s tenure were a good start to repairing years of flat funding, raids on dedicated funds, and disinvestment across the board. Collectively, they were the most progressive budgets New Jersey has seen in at least a decade due to a commitment to tax fairness that, in turn, reinvested in key assets that create strong communities and help grow the state’s economy.

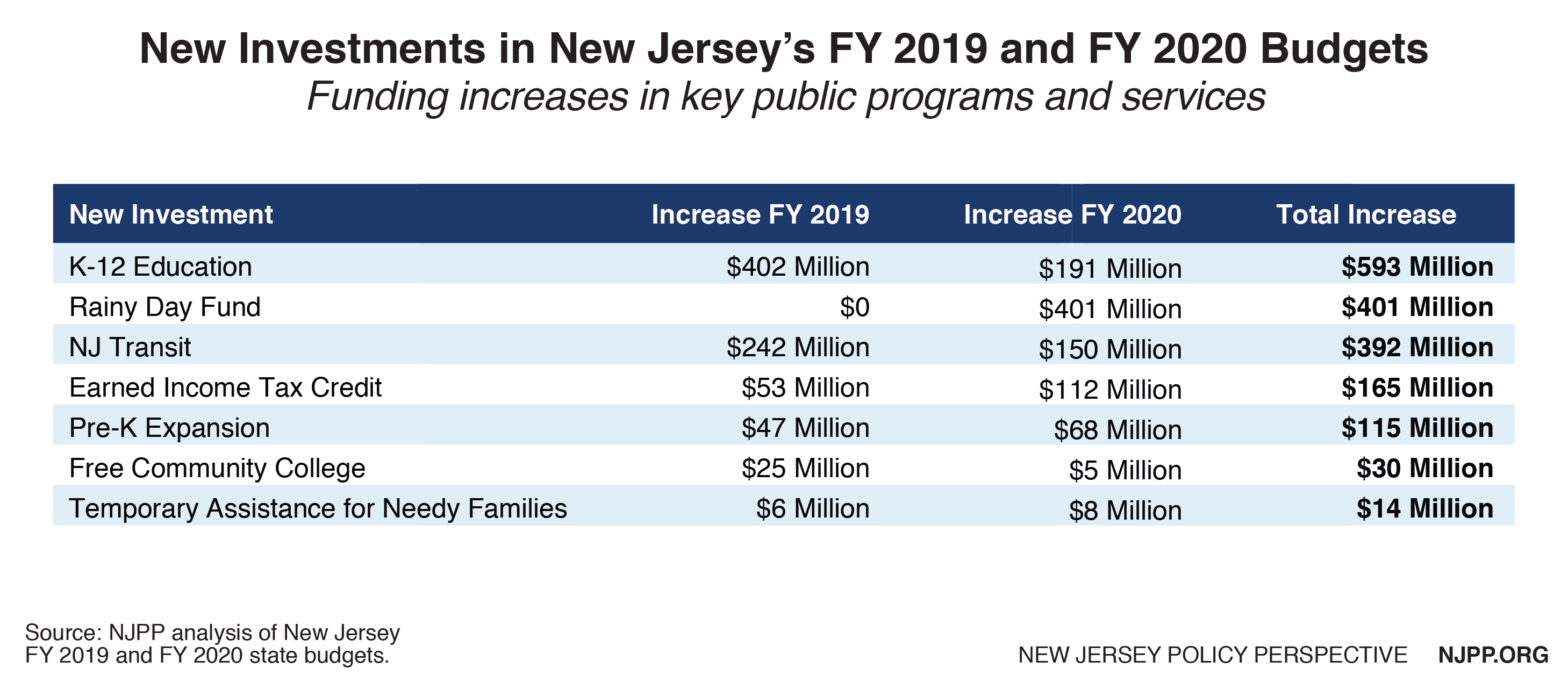

In the last two years, New Jersey made back-to-back record-breaking pension payments, protecting the retirement security of 800,000 public workers. Major investments were made in New Jersey’s most important assets like pre-Kindergarten expansion, K-12 education, and NJ Transit after years of neglect. The state prioritized working families and those struggling to get by with an expanded state Earned Income Tax Credit (EITC) and a new Child and Dependent Care Credit for low-paid working parents. Tuition-free community college was offered for the first time, giving 18,000 low-income students a path toward a more prosperous future. Funding for property tax relief programs improved and state-funded care workers, who are disproportionately women of color, were given an overdue raise. Finally, cash assistance for families living in extreme poverty, including 20,000 children, was raised twice, by a total of 32 percent, after 30 years without an increase.

The state’s last two budgets also prioritized good faith negotiation tactics and addressed an overreliance on budget raids. Through collective bargaining, the Murphy administration successfully secured about $800 million in real and lasting savings in the delivery of public employee health care in the FY 2020 budget — a 16 percent year-over-year decrease from the previous budget. This year’s budget also moved further away from the habitual raiding of the Clean Energy Fund and the Affordable Housing Trust, boosting their funds by $70 million and $59 million, respectively.

Finally, the state made its first, long overdue deposit of $401 million into the Rainy Day Fund, which had been empty since the height of the Great Recession. Though a relatively small investment — national budget experts recommend states save 16 percent of their annual spending in reserves — it is an important step in rebuilding an emergency savings account that the state can use during tough times without having to make detrimental cuts which commonly put low-income communities of color at the most risk. Unfortunately, it is likely to be used up quickly in response to the COVID-19 crisis.

All these investments were possible due to a steady job growth rate, a stable economy, and an administration that, over the last two years, prioritized new, renewable sources of revenue after a decade of tax breaks for wealthy families and large corporations. By restoring the 10.75 percent income tax rate on earnings over $5 million (a part of the millionaires tax that sunset under the Christie administration), applying the sales tax to purchases made on the Internet, closing corporate tax loopholes, and enacting a new (but temporary) surcharge on corporate profits, New Jersey has established a more fiscally sound foundation for the future — albeit one that is now at severe risk due to the harmful effects of the coronavirus pandemic.

Regardless of the current crisis, these last two years demonstrate how a budget can promote tax fairness and help New Jersey families gain economic security by making meaningful investments in their communities. Decades of neglect cannot be fixed in just a few years, however. Many departments that provide critical services and programs remain flat-funded and the raiding of dedicated funds to fill budget holes has continued. More will have to be done to help the state rebuild its assets and invest in long-term initiatives again.

Looking Ahead to FY 2021: Governor Murphy’s Budget Proposal

Prior to the COVID-19 pandemic, Governor Murphy’s FY 2021 budget proposal relied on healthy economic growth and adequate resources to fund new investments. That view has now shifted significantly to mitigating harm from a once-in-a-lifetime public health crisis while providing critical economic relief for workers, families, and small businesses.

As is, the $40.85 billion proposal commits to making substantial investments in affordable housing, education, and NJ Transit, as well as expanding programs designed to address racial, gender, and economic disparities. Like previous budgets under Governor Murphy, the FY 2021 proposal restates the importance of budgeting responsibly by scaling back on raids of dedicated funds, making the next scheduled pension payment in full, and growing a healthy surplus and Rainy Day Fund to better weather unexpected shortfalls without resorting to damaging cuts.

The Murphy administration and legislative leaders must now find a way to retain the overarching values of this proposal without shortchanging measures most needed during this pandemic. It is imperative that the state continue to adequately fund essential services to protect public health and provide relief to all affected workers and local businesses. The state’s modest Rainy Day Fund will be wiped out almost immediately, leaving it in no shape to handle immediate emergency needs. To sustain current needs, prop up the state economy, and reduce the harm to families and communities, Governor Murphy has requested at least $20 billion in aid from the federal government as part of a $100 billion multi-state package.[6] As of this writing, the federal government has provided $3.44 billion in support to New Jersey.[7] It seems that most, if not all, of the relief package is meant for COVID-19 specific interventions rather than helping New Jersey replace lost revenue due to the burgeoning economic recession. Regardless, if the state is to successfully tackle these challenges, the federal government will need to provide much, much more economic relief that is flexible for New Jersey to use as it needs. Only then can New Jersey policymakers begin to piece together a state budget that meets the needs of families and communities without making dramatic cuts during these extraordinary times.

In response to the COVID-19 crisis, New Jersey is going to have to think outside the box. The effects of this crisis on New Jersey’s economy will create major upheaval for the state budget due to a surge in demand for public services just as multiple sources of revenues needed to fund them begin to evaporate. Federal support for NJ Transit and COVID-19 response has been approved, but without knowing how long this public health crisis will last, New Jersey’s fiscal outlook is precarious at best. Policymakers have a choice: either prioritize and increase resources to protect the most vulnerable New Jersey families or continue giving massive tax breaks to the well-connected.

In these challenging times, it is more important than ever that New Jersey resist the impulse to cut vital programs and services. That would be a repetition of the mistakes made during the Great Recession, mistakes which slowed the state’s recovery and set it further back.[8] Raising revenue in a progressive manner is crucial to having the resources for a proper emergency response. Without additional revenue, the state won’t be able to fully assist workers, families, and businesses who are vulnerable to economic calamity during this crisis.

In order to provide critical relief, state lawmakers should prioritize and even expand existing programs that can support and protect frontline workers like first responders, health care providers, childcare staff, and those employed by businesses providing essential services like groceries and garbage pick-up. Workers who may not qualify for federal assistance because they lack income tax filing information must also be given priority. Programs that are best positioned to protect vulnerable households from losing their home or going hungry need to be protected. Extra funding will be needed to mitigate the spread of the virus among the incarcerated and the homeless population, too. All programs that make public colleges and universities more affordable must also be spared. College tuition aid and grants for community colleges play a critical role during an economic downturn, helping jobless workers expand their skills now for economic prosperity in the future.

The next state budget must prioritize tax policies that deliver very targeted benefits to families most in need. The scheduled increase of the state’s EITC to 40 percent must remain in place as should plans to expand the eligibility to young adults without children.[9] It would also be prudent to establish a state-level child tax credit, designed to help working parents meet the costs of raising children, during this time of economic instability. The lack of a robust social safety net is precisely why so many families are at increased risk by the economic fallout brought on by COVID-19.

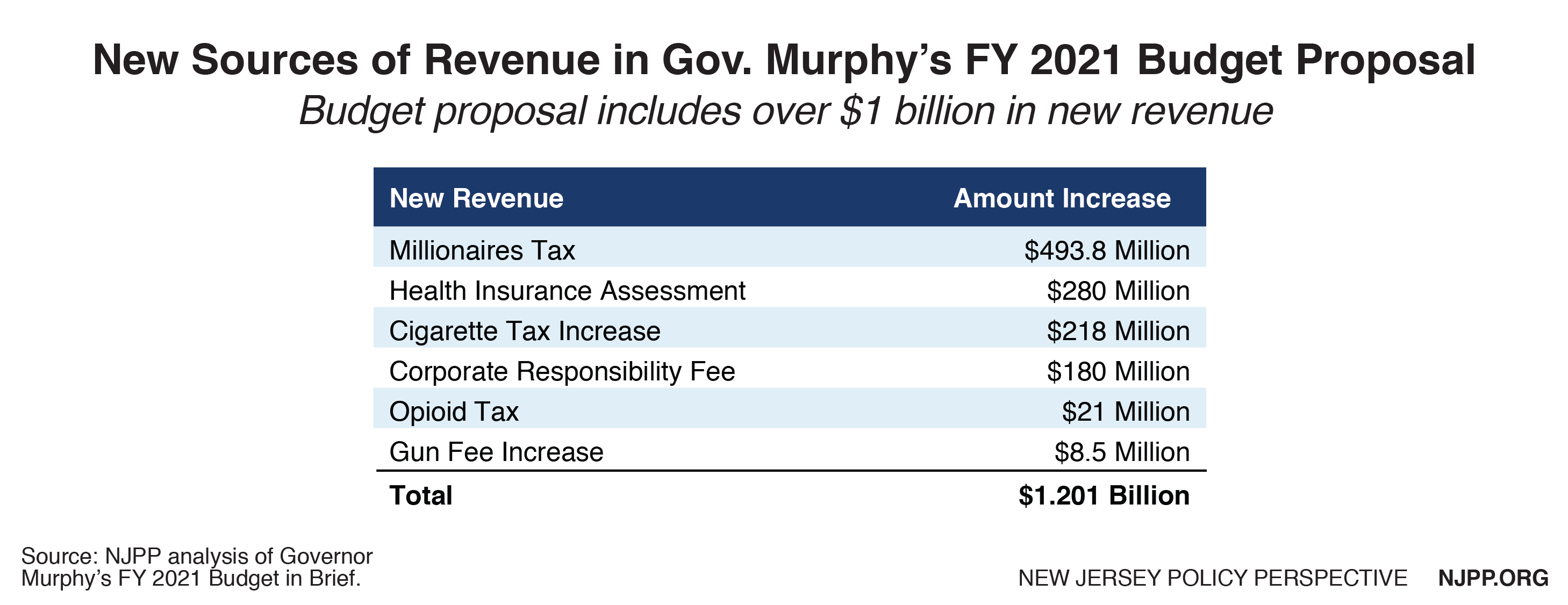

Lawmakers must table all efforts to cut taxes and instead focus on relief for those most in need by generating short- and long-term tax revenue from those who are in the best position to contribute: wealthy households and successful corporations. The Governor’s proposed budget, although crafted before the coronavirus pandemic, includes $1.2 billion in new sources of revenue through a true millionaires tax and a variety of fees and sin tax increases. To mitigate the harms posed by the current crisis, reverse revenue shortfalls, and enhance widespread prosperity and racial equity, the state must continue to prioritize responsible and progressive budgeting practices to overcome the current challenges. The proposed package of tax reforms is a good start, but it could and should go further.

For example, Governor Murphy has proposed applying the 10.75 percent income tax rate to earnings over $1 million — a 2-cent increase on every dollar earned over $1 million — to raise an additional $500 million in annual revenue. There is, however, a better way to make the income tax code more accurately reflect the lopsided income gains made by the top 15 percent of households over the past 40 years. Under the current tax code, individuals earning slightly over $75,000 are in the same bracket as those who earn just under $500,000. Creating new brackets between $250,000 and $2.5 million would make the tax code fairer and ensure budgets are not balanced on the backs of middle-class families. Further, New Jersey lawmakers should increase the marginal tax rate on annual incomes over $5 million. These changes would raise twice as much revenue as Governor Murphy’s proposal for property tax relief, school funding, and municipal aid.[10]

Governor Murphy’s proposed budget also contains a new health insurance assessment.[11] This was previously levied by the federal government but was repealed as part of the 2017 federal tax cuts. Governor Murphy’s budget estimates the new state-level policy would generate $280 million in its first year, the majority of which would support subsidies for New Jerseyans purchasing health insurance. This new revenue source is slated to generate up to $500 million annually after FY 2021.

The Governor also proposed a tiered fee for private employers that have more than 50 employees receiving state Medicaid benefits. The fee is designed to encourage large corporations to improve the quality of their health benefits and reduce their reliance on state resources. However, national budget experts warn this untested policy may only encourage employers to resort to a variety of tactics to avoid the fee, potentially leading to discriminatory hiring practices and lay-offs that would disproportionately impact people of color, single mothers, and young workers.[12] There are other more-direct and proven ways to ensure large corporations are paying their fair share in taxes. New Jersey could instead raise revenue through extending the 2.5 percent corporate business tax surcharge, closing tax avoidance loopholes, and reversing business tax cuts made in 2013.

There are multiple sources of revenue that must be put back on the table during these extraordinary times. Here are other policy recommendations to consider:

Revise taxation on inherited wealth to reverse the $500 million in tax breaks now going to wealthy heirs.

Repeal the 2016 sales tax cut and broaden the sales tax base by including services typically utilized by wealthy households, such as limousine services and chartered flights.

The purpose of fair taxation is to raise revenue in an equitable manner that can fund the critical public services and assets New Jersey families rely on with enough left over to save for a rainy day. A progressive tax code is also crucial to improving racial equity and undoing centuries of discrimination that have left communities of color behind,[13] making them particularly vulnerable during moments of crisis.[14] Unfortunately, New Jersey spent the last decade largely ignoring these important priorities. Had the state spent that time making annual investments in the Rainy Day Fund that match what it made last year, we would have nearly $4 billion to help tackle the COVID-19 crisis instead of the $401 million currently available. Going forward, implementing sound tax policies that help the state plan for future challenges will be paramount.

New Jersey’s economic future is at risk with the ongoing COVID-19 pandemic, the associated economic fallout from social distancing measures, and the uncertain amount of federal assistance New Jersey will ultimately receive. Workers, families, and businesses need real help and the state needs to prepare and act quickly. State lawmakers simply cannot afford to fall back on old habits by cutting government services and waiting out the storm. New Jersey needs new, reliable sources of revenue to build up a healthy surplus, avoid harmful cuts to vital services, and protect those most at risk during this economic downturn. Only then can we say with confidence that our state budget lives up to the values we all share and hold dear.

The COVID-19 pandemic is a major threat to New Jersey, presenting unique and pressing challenges to the state’s public health infrastructure and broader economy. As the number of positive cases climbs daily, state and local leaders have called for mandatory business closures and restrictions, as well as a voluntary curfew to contain the spread of the virus. These are necessary measures to avoid inundating the state’s health care system, but they come with an enormous cost to working families who will see their hours cut or jobs eliminated entirely.

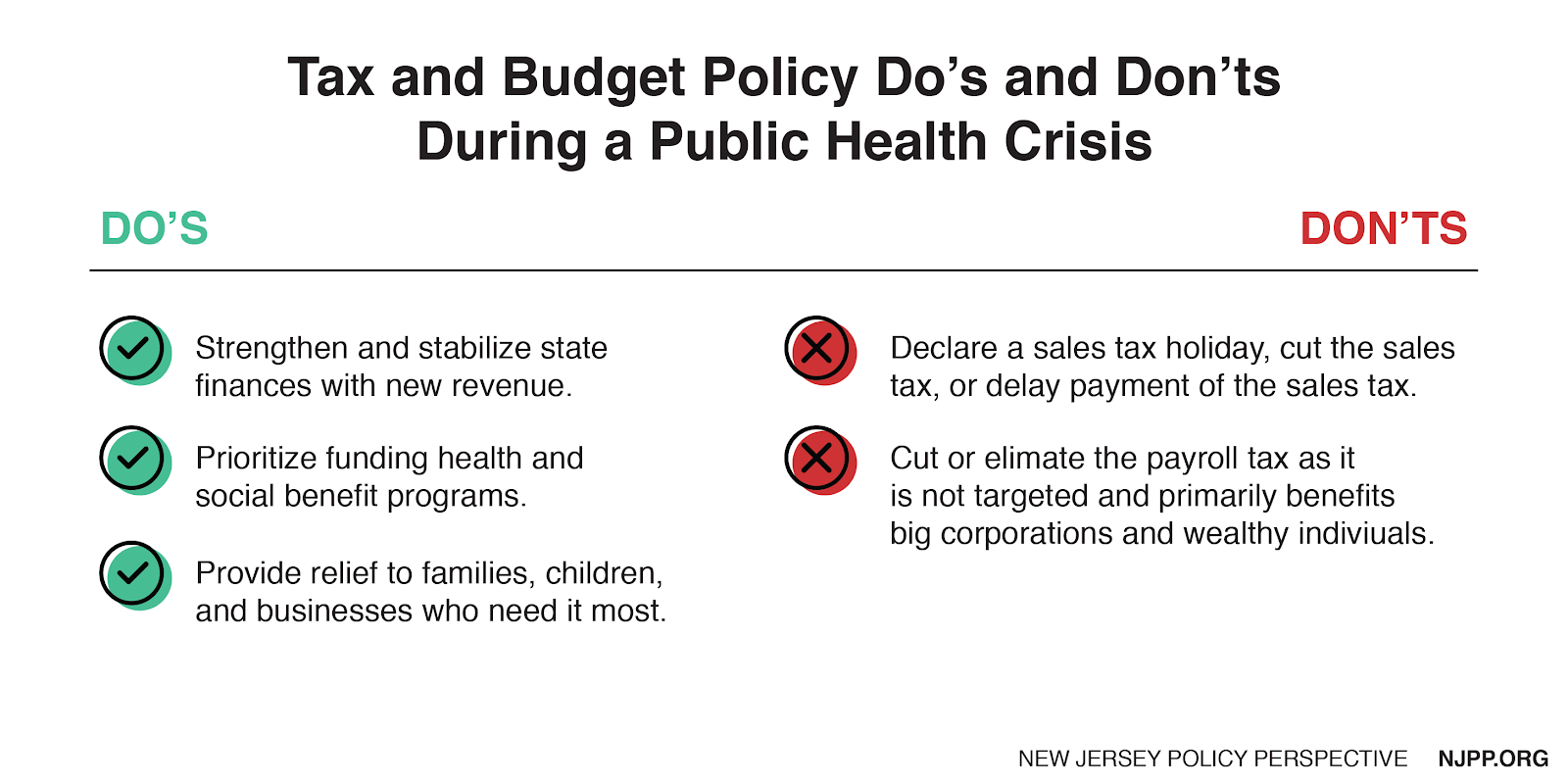

The economic fallout from COVID-19 will not be felt evenly. Those who earn the least are the most likely to suffer from a loss of income or loss of health coverage as a result of business closings and quarantines. New Jerseyans of color will particularly be harmed as they have fewer earnings on average and minimal amounts of wealth to fall back on in an emergency. And, because the state has not sufficiently invested in its Rainy Day Fund to help mitigate the challenges of the pending recession, the damage to people of color will be even greater. As such, the tax and budget policy decisions made by state lawmakers in the coming days and weeks will be critical in determining the size and scale of New Jersey’s recovery — and whether or not those harmed most by COVID-19 are centered in the state’s response. What follows is a list of tax and budget policies to pursue and avoid to help ensure New Jersey has the resources necessary to support and protect its residents in the coming months.

Do: Strengthen and Stabilize State Finances

New Jersey requires significant financial resources to adequately address the combined public health and economic crises from COVID-19. However, as the pandemic unfolds, unanticipated public health care costs will inevitably increase while state revenues, specifically from income and sales taxes, decline sharply. Implementing a more progressive tax code in this year’s budget will provide the state with the necessary revenue and flexibility to rapidly respond with targeted interventions. Restoring the millionaires tax and estate tax, strengthening the inheritance tax, and extending the corporate business tax surcharge would ensure wealthy individuals and corporations who have not been paying their fair share in taxes finally do so.

Workers who become unemployed, have their work hours reduced, or are laid off will be the first to experience economic insecurity under this health crisis. Therefore, lawmakers must expand access to all workers in the following state programs: earned sick days, temporary disability insurance, family leave insurance, and unemployment insurance. Access for these interventions can be improved by waiving eligibility requirements, removing waiting periods that prevent workers from accessing benefits right away, speeding up application and approval processes, and utilizing emergency funds to pay for these policy expansions. It is paramount that New Jersey leave no one behind in the COVID-19 recovery.

In addition, state lawmakers must ensure that existing social safety net programs remain well-funded so that more families have their needs met, even if the state experiences a revenue shortfall. More families will likely need public assistance during this crisis. Programs like emergency nutritional assistance, food pantries, Medicaid coverage, cash assistance (TANF), subsidized child care, shelters, and other critical services provide necessary and stabilizing support and they must be funded to deliver payments and benefits as fast as possible.

Finally, New Jersey must respond to this health crisis by eliminating barriers to health care. For instance, the state can waive costs for everyone seeking treatment for the COVID-19 virus. Funding should be provided to support better outreach regarding policies implemented in response to the pandemic so that all communities stay informed of critical developments. This means communicating in multiple languages and working directly with institutions like worker centers, school districts, community clinics, as well as state agencies who are providing services. Finally, the state should expand access to CHIP and NJ FamilyCare to ensure all New Jersey children have comprehensive health coverage and can get the care they need during these challenging times.

Do: Provide Relief Directly to Small Businesses Who Need It

One immediate concern created by this crisis is the increased likelihood of small businesses laying off employees and closing down as the economy heads into a recession. During an ordinary recession, a sizable stimulus could be expected to keep businesses afloat and put people back to work. With a health crisis also underway, workers and businesses could be shut down for weeks if not months, leaving them unable to earn or spend money.

While some policymakers have proposed payroll tax cuts or sales tax holidays to provide relief to small businesses, those interventions are severely flawed and would do much more harm than good (as explained below in Don’ts). Instead, policymakers should focus on interventions that work quickly and target the most at-risk businesses. As the crisis unfolds, states need to implement policies that will directly encourage businesses to keep their employees and continue paying them.

Rather than throwing hundreds of millions of dollars at major corporations, the state should be prioritizing main street businesses and smaller firms. While the state Economic Development Authority (EDA) is largely known for providing tax subsidies to already wealthy and well-connected corporations, it would be much better off prioritizing smaller businesses, especially during this crisis. By extending lines of credit to troubled businesses, offering low or no-interest loans, and focusing the benefits of tax credits on those businesses most at-risk of employee layoffs and closure, New Jersey can help them stay afloat and protect local economies.

Finally, as much as possible, policymakers should seek to tie employee protections to any business assistance programs. The primary goal of providing relief to businesses is for them to maintain payroll and avoid layoffs. As such, the New Jersey Department of Labor should work in conjunction with the EDA and other organizations to ensure businesses guarantee they will meet these requirements and pay their workers as a condition for receiving assistance from the state.

Don’t: Declare a Sales Tax Holiday or Cut the Sales Tax

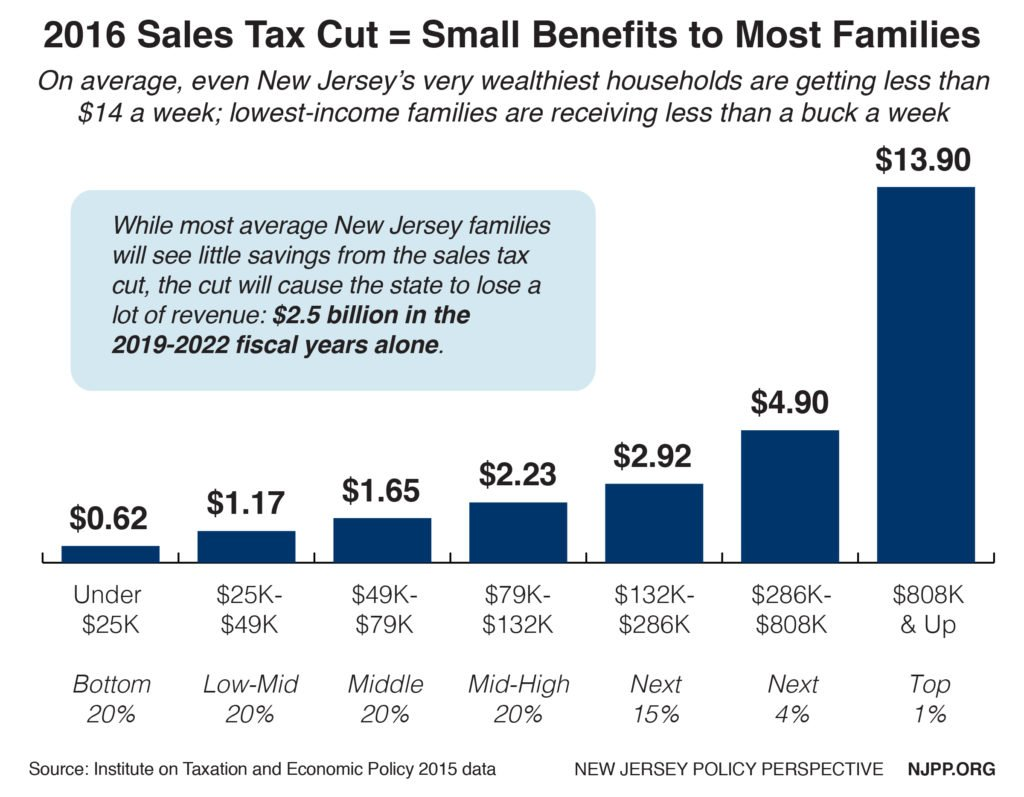

The sales tax is one of the biggest sources of revenue for the state of New Jersey, generating approximately $1 billion on a monthly basis. In 2016, New Jersey cut the sales tax from 7 percent to 6.625 percent, reducing revenue to the state by about $600 million a year and growing; by fiscal year 2022, the loss is expected to be $655 million annually.

The combined challenges of the coronavirus pandemic and pending recession will create a crisis of consumer demand in the short and long term. If people can’t get to work or don’t have disposable income to spend, suspending the sales tax won’t cause them to make purchases. In fact, they will end up doing more harm than good, starving the state of much needed revenue at a time when New Jersey needs to expend resources and expand public health services and assistance to workers, families, and businesses hit hardest by the fallout from this crisis.

Other sales tax holiday proposals are designed to delay the collection of sales tax for several months. This would not have the intended effects of stemming a recession or spurring consumer spending. It would do little more than withhold critical resources from the state at a time when it needs revenue and resources the most. Furthermore, New Jersey’s sales tax already exempts food and clothing, meaning there is little benefit to low-paid families and those in poverty who are already struggling to afford basic needs. This is easily understood by reviewing the regressive impact of New Jersey’s 2016 sales tax cut.

Consider, for example, a payroll tax cut of 2 percent of workers’ earnings:

A single parent getting by on $25,000 a year would receive just $500 over the course of a year, even as a couple with a combined $275,400 income (with each spouse earning half this amount) got $5,500. Even if the tax cut’s dollar value were capped, only higher earners would get the maximum benefit. That’s not sound economic policy, since affluent households generally spend a much smaller share of any added income than lower-income households do.

Chye-Ching Huang, Center on Budget and Policy Priorities

Further, cutting the payroll tax would not benefit people without earnings, even though they are most likely to spend any additional resources they receive on basic and immediate needs. This group includes those who are laid off from their jobs and no longer receiving a paycheck, as well as seniors and people with disabilities. Those supporting children or other dependents would also not receive any additional help from a payroll tax cut.

A payroll tax cut would benefit big businesses, however, as half of the payroll tax is paid by employers. Eliminating the employer side of these taxes would provide a windfall to corporations and other businesses that are not at greatest risk for failure. Better interventions would be extending lines of credit and no-interest loans to businesses in need of support.

Welcome to NJPP’s Budget Address FY 2021: Rapid Reaction, your source for commentary and data analysis on Governor Murphy’s address. The transcript below was taken from NJPP’s conference room, over a delicious Sicilian pizza, and has been lightly edited.

Lou (Louis Di Paolo, Communications Director): Budget season is back! Earlier today, Governor Murphy delivered his budget address for fiscal year (FY) 2021, where he detailed new investments in education, transportation, tax credits for working families, and so much more. The budget proposes the largest pension payment in state history, limits one-shot revenues and (some) raids of dedicated funds, and makes another big investment in the state’s Rainy Day Fund.

For New Jersey Policy Perspective (NJPP), this year’s budget season started a week early with the launch of For The Many NJ. This new coalition, made up of faith-based organizations, labor unions, and nonprofits advocating for education, the environment, transportation, affordable housing, and more, stood on the State House steps to call for a new approach to budgeting that puts the needs of ordinary people over those of corporate special interests.

Joining me in reflecting on what we heard today are Nicole Rodriguez and Sheila Reynertson! Sheila, can you give a brief overview of the coalition and its priorities this budget season?

Sheila (Sheila Reynertson, Senior Policy Analyst): Happy to do that, Lou. We are over 30 organizations working together to advance smart, responsible budgets that are sustainably funded. We are also prioritizing racial and economic equity as a critical component in realizing a New Jersey that works for the many instead of the few. We want to see New Jersey reverse ill-advised tax cuts like the tiny decrease of the state sales tax, close remaining corporate tax loopholes that allow profits to be parked overseas, and ensure the ultra-wealthy pay their fair share on inherited wealth.

Nicole (Nicole Rodriguez, Research Director): The coalition recognizes that budgets are about more than numbers. That’s because each line item represents real people – our neighbors, our families, our coworkers, as well as students and seniors in every corner of the state. Budgets have direct implications on all our livelihoods and we need to keep that in mind when discussing and advocating for sound budget practices and investments that will help all residents thrive.

Lou: Beautifully said, Nicole. Budgets really are moral documents and represent the state’s priorities. Keeping that in mind, let’s jump into the governor’s address. First, what did we like?

Nicole: The governor proposed a boost to working families across the state by way of the Earned Income Tax Credit (EITC), a refundable tax break for lower-income workers. The EITC is an important anti-poverty program that helps families struggling on low wages to make ends meet and provide basic necessities for their children. Think of it like a refund for low-paid workers.

Specifically, the FY 2021 budget proposal increases the state tax credit to 40 percent of the federal benefit and proposes lowering the age threshold for workers without children to 21, making about 60,000 more workers eligible.

Sheila: I was really impressed with another round of solid investments in education across the board. Students and teachers should be very excited about this budget.

Pre-Kindergarten expansion continues to be an important priority with $83 million in additional funding. That will help 30 more districts introduce early education. That’s on top of the expansion to 60 districts over the past two years. Direct formula aid for K-12 public schools is slated to receive an additional $336 million. In total, the Murphy administration has increased this funding by 11 percent. It was great to see continued support for the community college grants program, which started in 2019, and it was a pleasant surprise to learn this budget will bring this model to 4-year public college and universities.

Lou: I’d like to point out the $1.6 billion surplus and $300 million deposit into the Rainy Day Fund (RDF). These aren’t sexy investments, but they help rebuild the state’s fiscal foundation and prepare New Jersey for the next recession or superstorm. The governor remarked that this is the first time the state is making back-to-back deposits into the RDF in over 20 years. That really surprised me given that this is such a basic budgeting best practice.

Sheila: Yes, baby steps! The state’s Rainy Day Fund was emptied during the height of the Great Recession and then was allowed to grow cobwebs for years. While this is a relatively small investment, it is an important step in rebuilding an emergency savings account that will give New Jersey the ability to weather tough times without having to resort to making drastic and dangerous cuts to programs that, might I add, low-income communities depend upon the most.

Lou: You know what else was emptied during the last decade? Billions and billions of dollars in revenue. New Jersey enacted $15 billion in cumulative tax cuts that primarily benefited the state’s wealthiest families and biggest corporations.

How’s the governor’s proposal stack up in terms of recouping this lost revenue and ensuring the ultra-wealthy pay their fair share? Or, more broadly, how do we feel about the governor’s proposals to raise revenue?

Sheila: It’s baaack! Governor Murphy has proposed the millionaires tax for the third year in a row.

This time the Senate President has signaled his willingness to support it in exchange for a larger pension payment. We shall see how this all plays out in the next few months, but it’s a proposal that is long overdue. Since the Great Recession, there has been a 62 percent increase in the number of New Jersey residents with incomes over $500,000 in annual income. A third of them make over $1 million in annual revenue. These high earners have further enriched themselves and their families through the many new loopholes and tax cuts in the 2017 federal tax law. It’s time for the income tax code to reflect this reality – permanently. It would generate much needed, sustainable revenue for direct property tax relief and address worsened income and wealth inequality in the Garden State.

Lou: I can’t wait for New Jersey to pass the millionaires tax. Then I’ll finally be able to change my twitter name back to normal.

Nicole: Let’s be clear here: The millionaires tax is not the end all be all of tax fairness. New Jersey can and should do more to ensure the ultra-wealthy and corporations pay their fair share. The Senate President made a valid case this weekend for extending the corporate business tax surcharge for companies with over $1 million in annual profits. Many of these corporations pay little-to-no federal taxes and received a huge windfall thanks to the Trump administration’s 2017 tax cuts.

The state can also do a better job of taxing inherited wealth, whether it be through bringing back the estate tax or reforming the inheritance tax for wealthy heirs.

Lou: All great points. New Jersey can definitely do more to advance equity through the tax code. Sheila, were there any new programs or services in the budget that could help reduce disparities?

Sheila: Yes! In his speech today, Governor Murphy highlighted three initiatives that would have a direct impact on racial disparities. He lifted up the Amistad Commission, which will help revitalize African-American history curriculum in public schools, highlighted ongoing efforts to eliminate the racial disparities in New Jersey’s dismal maternal mortality rates, and announced new programs to break the school-to-prison pipeline which disproportionately harms Black and Latino communities.

Lou: I’m curious to hear more about eliminating racial disparities in maternal mortality rates. New Jersey truly is a tale of two states when measuring the experiences of people of color with white people. We have the best public schools in the nation but the worst racial segregation; the best maternal health care but one of the worst maternal health rates for Black mothers; one of the biggest gaps between the wealth of white families compared to Black families. I could go on.

Sheila: We would be here pretty late if you did. This pizza is already getting cold, and I’m sure all of our cats miss us.

Lou: That is very true! Let’s move this thing along: What was missing in the governor’s address?