New Jersey’s finances are stretched thin as the COVID-19 pandemic has essentially shut down the state’s economy. Precautions to keep the public safe and healthy have drastically reduced revenue from the sales, income, and corporate business taxes, throwing the state budget out of balance. New investments in everything from pre-K expansion, transit infrastructure, and tax credits for low-paid workers now face an uncertain future, as do the various state departments and agencies at the forefront of New Jersey’s COVID-19 response.

New Jersey is not alone, according to a new report by the Center on Budget and Policy Priorities (CBPP), as states across the nation are facing what could be the largest budget shortfalls ever recorded. Federal lawmakers have already provided states with some fiscal relief through the Coronavirus Aid, Relief, and Economic Security Act, or CARES Act, but states are limited in how they can use these funds. As it stands, significantly more aid will be necessary for states to address the ongoing public health emergency, provide relief to families and small businesses who need it, and avoid drastic cuts to public services that would disproportionately harm communities of color and only prolong the nation’s ultimate recovery.

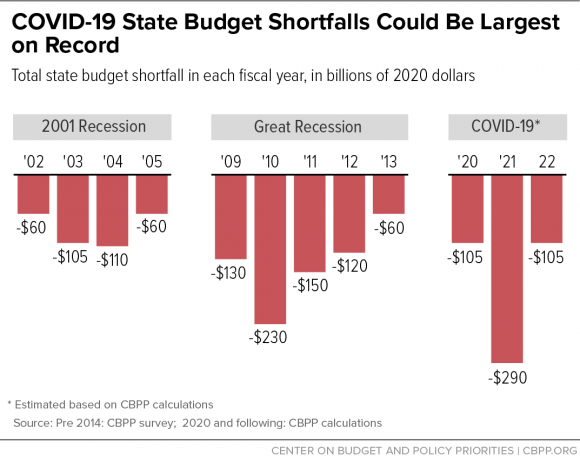

CBPP estimates that state budget shortfalls could total more than $500 billion, with most of the revenue loss concentrated in the upcoming fiscal year. These are conservative estimates as they do not include the substantial new costs that states are incurring to contain the COVID-19 virus, nor do they account for revenue shortfalls at the local, territorial, or tribal levels of government. Overall, these figures far exceed the federal aid given to states thus far, as well as what states already have saved up in their rainy day funds. What’s worse for New Jersey (and many other states) is that it will quickly exhaust its Rainy Day Fund, if it hasn’t already, as lawmakers left the state’s reserves empty for a full decade before finally making a modest deposit last year. To ensure a strong recovery from COVID-19, Congress should prioritize substantial and immediate fiscal relief in its next stimulus package.

What happens if the federal government does not provide states with significantly more aid?

One unattractive option is to make enormous cuts to state spending. This would mean laying off teachers and other public employees, as well as slashing spending on state programs and services that families rely on, especially during a crisis like the one we are living through. As we saw firsthand in the wake of the Great Recession, a cuts-heavy response to a downturn worsens the economy’s fall, slows the state’s recovery, and causes long-term harm to families and communities who are already struggling to make ends meet. It’s important New Jersey learns from this experience and does not make the same mistakes of the past.

So what else is there to do?

Another option is to borrow funds to support critical needs. Normally, New Jersey would not be allowed to borrow funds to cover operating expenses, but there is an exception in the state Constitution for “purposes of war, or to repel invasion, or to suppress insurrection or to meet an emergency caused by disaster or act of God.” In response to the COVID-19 pandemic, the Federal Reserve will buy up to $500 billion in bonds from state and local governments across the country to help shore up their finances. Governor Murphy has already expressed interest in borrowing up to $9 billion from the Fed, and NJPP has come out in support of that proposal, as President Brandon McKoy said the pandemic, “justifies, if not demands,” such action. Borrowing would help New Jersey avoid damaging cuts, which would help speed the state’s recovery from the recession.

But even if the state borrows to fill budget holes, more resources and funding will be needed to pay off these bonds in the short-term and stabilize the state’s finances in the long-term; after years and years of disinvestment and austerity, this should surprise no one. State lawmakers can accomplish this by ending tax breaks passed under the previous administration for the state’s wealthiest households and biggest corporations, as well as by reforming the income tax code to ensure that the top 5 percent of earners pay their fair share. Raising new, sustainable revenue will help New Jersey recover from the current economic downturn, prepare the state for the next one, and build an economy that works for the many, not just a chosen few.