To read a PDF version of this report, click here.

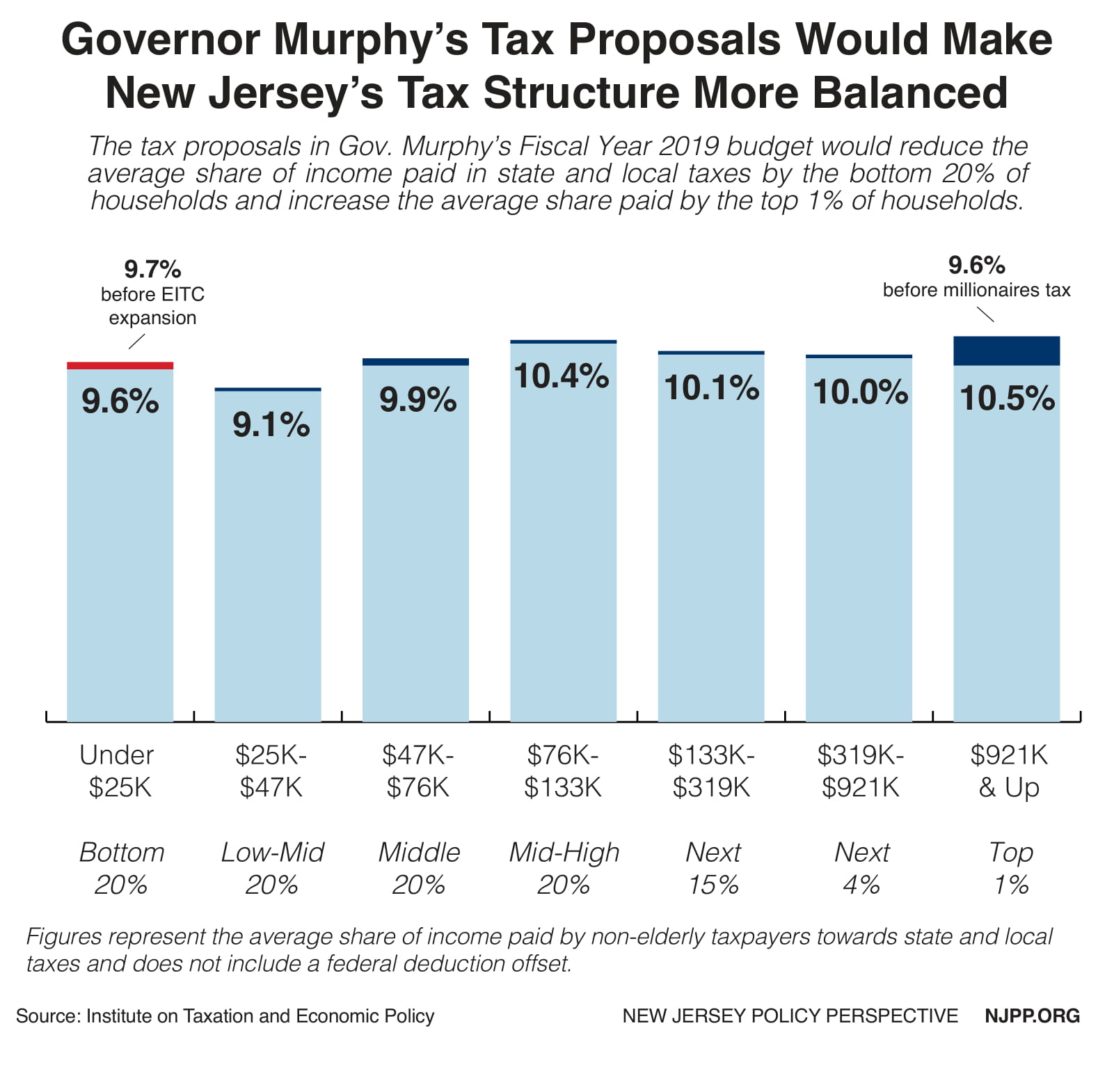

The tax changes proposed in Gov. Murphy’s first budget would bring more balance to New Jersey’s tax code by raising taxes on the wealthiest one percent while reducing them for the lowest-income New Jerseyans.[1] Updating the tax code would also raise nearly $2 billion in new revenue for targeted investments in early education, public transit, health care and other essential public services.

The effect of the Murphy plan is based on the following tax policy proposals:[2]

The effect of the Murphy plan is based on the following tax policy proposals:[2]

- An income tax increase on annual earnings of $1 million or more by implementing a tax rate of 10.75 percent

- The restoration of New Jersey’s sales tax to 7 percent

- The closing of tax loopholes used by multi-state corporations by implementing “combined reporting”

- An increase of the EITC from 35 percent to 40 percent phased-in over 3 years

- An increase in the state property tax deduction from $10,000 to $15,000 for over half a million homeowners

- A new child and dependent care tax credit for families with annual incomes of less than $60,000

These targeted tax changes would bring greater balance to the state’s tax code by giving working families in the bottom 20 percent a much-needed tax break and ensuring that the wealthiest New Jerseyans are paying their share. The overall effect would be a tax code that more accurately reflects one’s ability to pay.

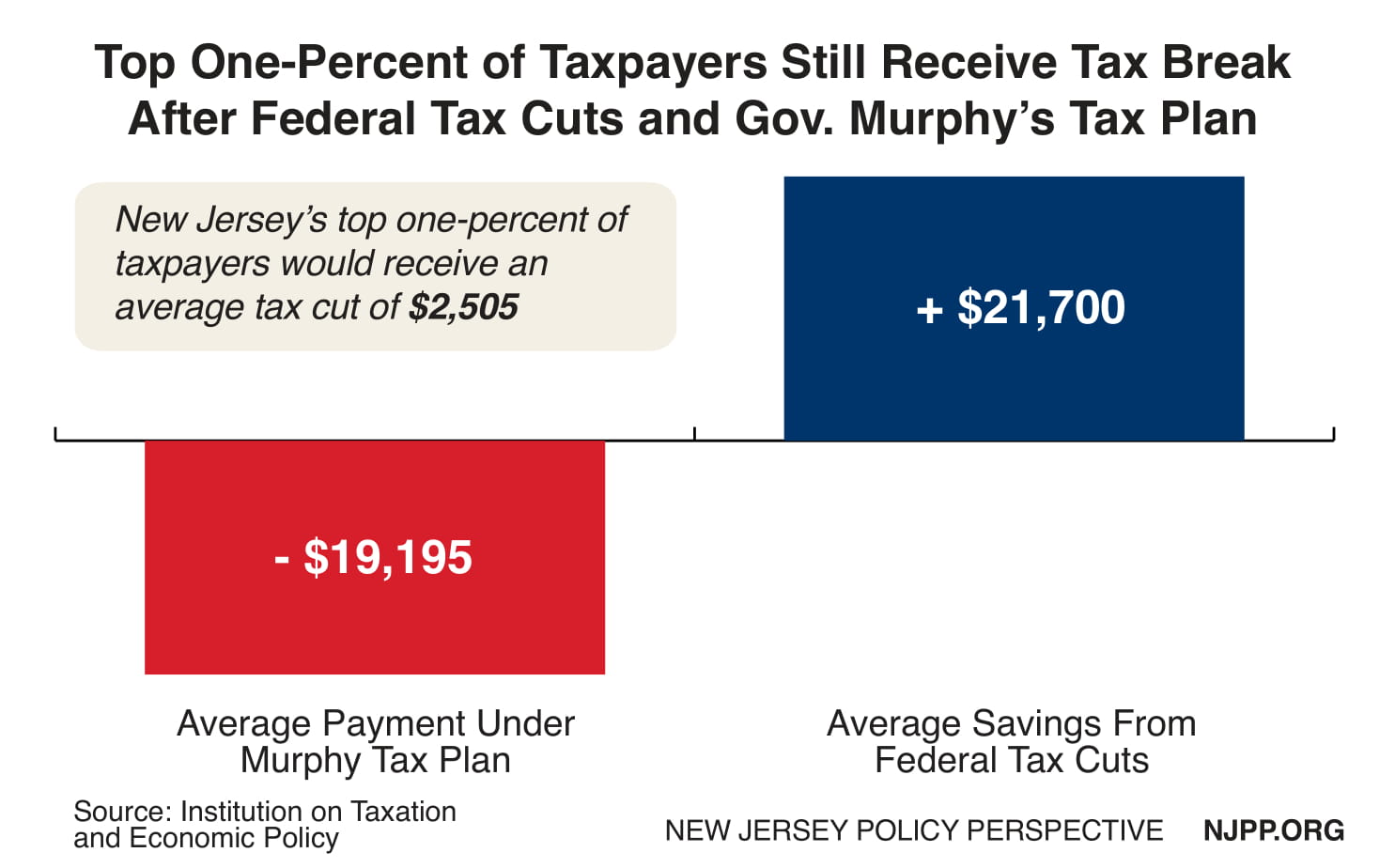

The proposed new marginal gross income tax rate on incomes over $1 million was popular with legislators during the Christie administration, as it was passed five times by both houses of the legislature and vetoed each time. Now, after recent changes to the federal tax code, some legislators fear that this is not the right time to raise state income taxes on those earning $1 million or more a year. These fears are unfounded: New Jersey’s top one-percent of taxpayers still receive a net tax cut when combining the effects of the recent federal tax overhaul and Gov. Murphy’s proposed tax changes.

According to a side-by-side analysis of the Tax Cuts and Jobs Act and Gov. Murphy’s plan, the top one percent of taxpayers – those earning over $924,000 a year and with an average annual income of about $2.5 million – would still come out ahead. That’s because their average tax break from the federal tax law is slightly larger than their average tax increase at the state level. Some of these wealthy households may experience a slight tax increase depending on their specific circumstances, but as a whole, the top one percent would not be burdened under Gov. Murphy’s tax plan. In fact, they would see little to no change to their overall tax bill, while New Jersey’s most important assets would see a much-needed boost in funding.

The lion’s share of income growth over the past decade has gone to New Jersey’s wealthiest taxpayers, yet the state and local tax code stillrequires low- and middle-income households to pay greater shares of their incomes in taxes than their wealthier neighbors. Gov. Murphy’s tax plan addresses the upside-down nature of the state’s tax code while raising the revenue needed to give all New Jerseyans a better opportunity to thrive – and, given the federal tax windfall to the wealthiest households who did nothing to earn it, lawmakers should feel confident in enacting a more equitable tax code here in the Garden State. The alternative would either be draconian cuts to public services or more reliance on taxes and fees that disproportionately fall on low- and middle-income families. Each of those options only leads to a more difficult and uncertain economic future for New Jersey families.

Endnotes

[1] Institute on Taxation and Economic Policy (ITEP) Microsimulation Tax Model, May 2018.

[2] These data do not include a “federal deduction offset” figure as appears in Who Pays and other ITEP reports because under the Tax Cuts and Jobs Act, the federal deduction for state and local taxes is limited to $10,000 and will predominantly affect only a relatively small group of high-income itemizers, most of whom will likely have enough tax payments to exceed the $10,000 cap. Because the availability of a deduction will be narrowed – and it will no longer vary significantly in proportion to state and local taxes paid – it does not function as a generalized offset of those taxes.